Deposits: Banking dynamics

| Photo Credit:

Andrii Yalanskyi

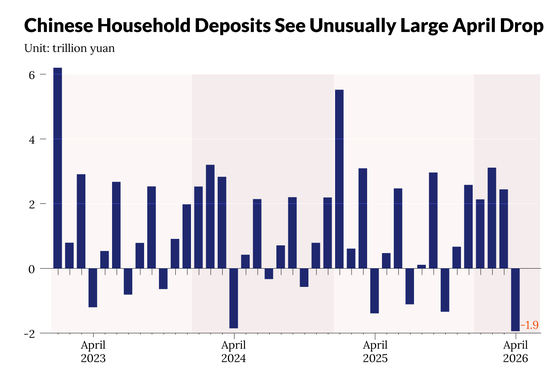

Where are all the deposits going? On April 15, Reserve Bank of India officials met commercial lenders urging them to bring in more ‘stable deposits. It is often argued that lack of deposit mobilisation, caused by a ‘shift in household savings into equities’, lies at the deposit conundrum impacting the Indian banking system (Bloomberg, April 15, 2026).However, what if the root cause of deposit sluggishness lies within the bank itself? What if it is not savers queuing up for mutual fund, but rather investment in bank shares that is ultimately leading to this deposit-capital conundrum?We argue that the deposit growth slowdown is a by-product of two important facets of Indian banking: increased equity held by banks, as reflected in the growing market capitalisation of bank stocks and the increase in regulatory capital requirements.Broad trendsFirst, from early 2022, deposit growth started lagging the credit growth. The scissor effect between deposit and credit growth is not a new phenomenon. Also, a CD ratio of above 75 per cent is not a new occurrence. There are times (like during January 2018 to October 2019) when credit growth far outpaced deposit growth and CD ratio was above 75 per cent.Second, credit growth fell sharply in July 2024 to 13.7 per cent year-on-year from 19.5 per cent in July 2023. This coincides with the period of regulator driven slowdown in unsecured personal loans, reduced bank lending to NBFCs, and a high base effect from the previous year.Why is the deposit sluggishness a conundrum? While a common discourse on deposit sluggishness is that households are increasingly moving to capital markets and hence withdrawing from deposits, but this is half the story. Because any money invested in stock market must also show up in bank’s liabilities — ultimately it must be booked in a bank account. There may be compositional changes in term, saving and current deposits — in aggregate, deposits of capital market activity must find a place in bank’s liability.The root cause of deposit crunch plausibly lies somewhere else, not just the portfolio allocation by households.First, capital accumulation by banks have significantly increased. Changes in system level liquidity, as presented by annual M3 variation, is shown in Table 1. Asset side liquidity creation is mapped by the liabilities in the form of currency with the public, bank deposits (including both demand and time deposits), other deposits with RBI (mainly the CRR reserve), and the banking sector’s net monetary liabilities.Changing liabilitiesThe changes in the banking sector’s net monetary liabilities since 2022 has been massive. Its contribution in the change increased from 11 per cent during 2021 and 2022 to 27.8 per cent in 2023, 23.4 per cent in 2024 and whopping 38.3 per cent in 2025.Capital and reserve, or equity, of banks is the largest component of banking sector’s net monetary liabilities: Indian banks have accumulated large capital during this period. Thus, increase in deposits is substituted by increase in banks’ equity. The increase in banks’ equity is not just an allocation of household savings into stock market; it is specifically the move of savings to bank stocks.The impact is amplified of course, by growing financialisation and digitalisation. Thus, additional equity by banks necessarily entails movement from deposit-like liquid claims toward equity, and in equilibrium market clearing requires that deposits will fall by the same amount: ‘new bank equity must come from somewhere’ (Gorton and Winton, 2017).Second, banks are keeping far higher capital buffer than prescribed by regulation and higher equity is substituting deposits for liquidity creation. This is corroborated by high capital adequacy ratio of banks. The top 10 banks, constituting over 73 per cent assets of Indian banks, recorded the CRAR in the range of 17-19 per cent, markedly far above than statutory minimum.Regulatory capital requirements have increased significantly since the Global Financial Crisis (GFC). In the post Covid scenario, the immediate trigger was RBI’s tightening of risk weights on unsecured consumer credit and bank exposures to NBFCs, alongside banks’ conscious efforts to maintain healthier Credit-Deposit (CD) ratios. These measures moderated aggressive lending in high-growth but riskier segments, but also impeded liquidity.Thus, with financialisation and digitalisation, people are putting more money in stock markets. A large sum of money is also moving for the bank stocks and effectively eating away deposits. At the same time, over valuation of stock prices is making banks more capital rich than ever. What can be policy measures to address this?First, banks can be given flexibility on the way they hold the regulatory capital. One way forward would be to treat portions of regulatory capital as releasable and countercyclical (ECB, Macroprudential Bulletin 32, November 2025), which would allow buffers to be used during stress periods.Second, with growing financialisation, banks must move away from deposit-dependence and tap financial markets to access funds for credit expansion.Das is ICICI Bank Chair Professor, Indian Institute of Management Ahmedabad (IIMA); RoyTrivedi is Associate Professor, National Institute of Bank Management (NIBM). Views expressed are personalPublished on May 30, 2026