The Bank of England opted to keep its benchmark interest rate parked at 3.75% on April 30, choosing patience over action in a monetary policy environment that looks increasingly like a game of wait-and-see. The Monetary Policy Committee voted 8-1 to hold, with Governor Andrew Bailey framing the decision not as inaction but as a deliberate choice shaped by what prior rate hikes have already done to the economy.

The lone dissenter was Chief Economist Huw Pill, who pushed for a 25 basis point increase that would have brought the Bank Rate to 4%. That split tells you something about the internal tension at Threadneedle Street: most members think prior tightening is still working its way through the system, but at least one senior voice thinks it isn’t working fast enough.

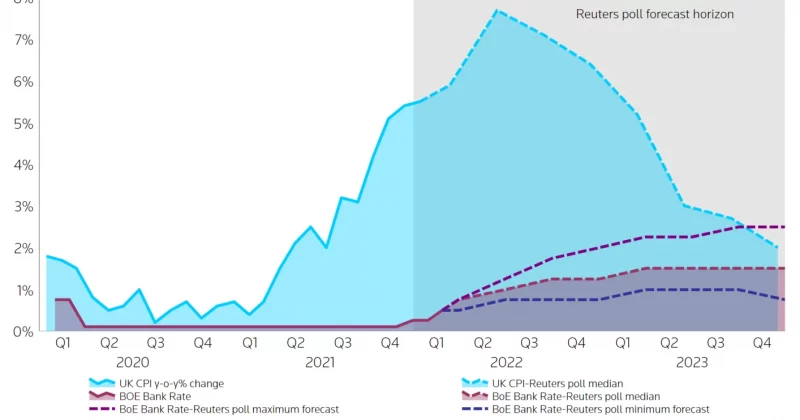

The inflation problem hasn’t gone away

The UK’s inflation rate currently sits at 2.8%, meaningfully above the Bank’s 2% target. March figures were even worse, clocking in at 3.3% before the slight pullback.

The outlook isn’t exactly comforting either, with projections suggesting inflation could climb further throughout 2026. A significant driver of that upward pressure is energy costs linked to the ongoing conflict in Iran, which has disrupted supply chains and pushed up prices for fuel and utilities.