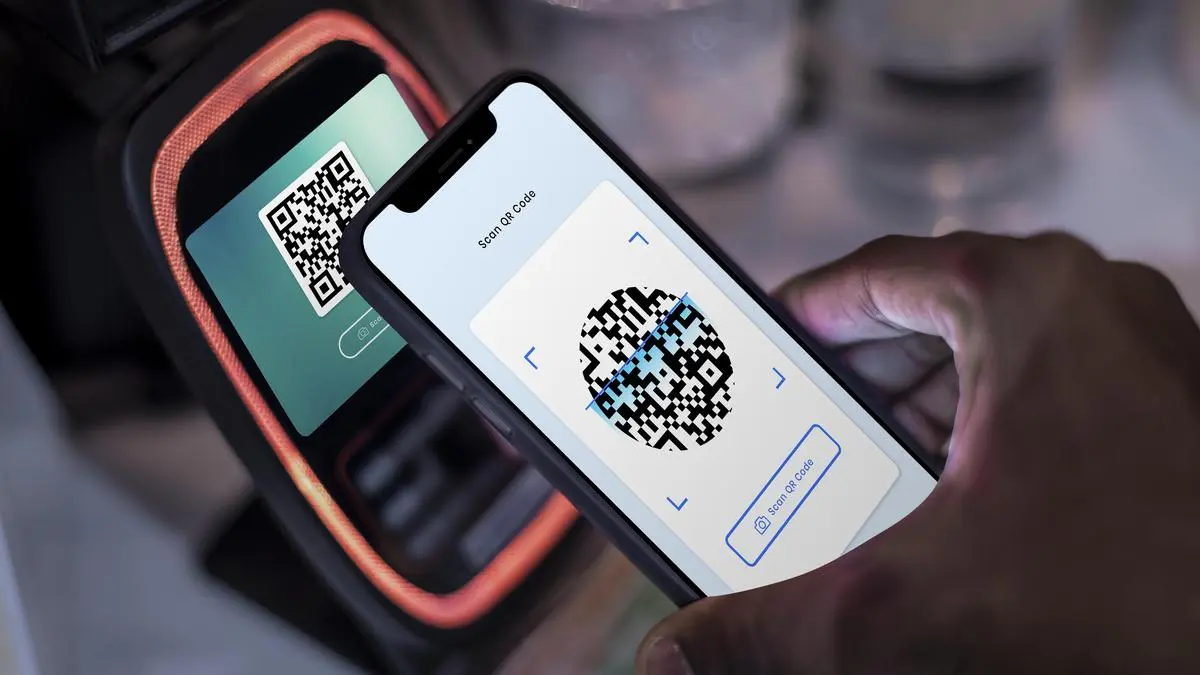

For Indian travellers, paying abroad is beginning to look very different from what it did a few years ago. Instead of carrying large amounts of cash, worrying about forex cards, or paying high credit card conversion charges, many travellers today are increasingly using UPI at shops, restaurants, airports, and retail outlets overseas. But while UPI abroad offers convenience, experts say many travellers still do not fully understand how international UPI payments actually work, what charges apply, where payments may fail, and what fraud risks users should watch out for. And unlike domestic UPI transactions, cross-border payments often involve multiple banks, forex conversions, telecom networks, and merchant restrictions operating simultaneously behind the scenes. In which countries does UPI work internationally? UPI’s global acceptance is still evolving and does not work uniformly across all countries. “UAE, Singapore, Bhutan, Nepal are some of the countries with active corridors and established merchant ecosystems,” says Ranadurjay Talukdar, Partner and Payments Sector Leader at EY India. In these markets, Indian travellers can increasingly use UPI at restaurants, retail stores, tourist locations, and local merchant outlets. However, adoption remains uneven across Western countries and Europe, where UPI acceptance is still relatively limited and often restricted to select merchants or payment partnerships. This means travellers cannot yet assume UPI will work everywhere internationally the way it does in India. Experts therefore advise travellers to always carry backup payment options such as international debit cards, forex cards, credit cards and emergency cash because merchant acceptance can still vary widely between countries and even between stores in the same city. What are the transaction limits for UPI payments abroad? Many travellers are unaware that international UPI payments also come with transaction limits. “As per recent updates, UPI Global transactions at merchant outlets abroad can have a limit of up to ₹2 lakh per transaction/day in supported international markets, including Europe, where UPI acceptance is enabled through partnerships,” says Rohit Mahajan, Founder and CEO, plutos ONE. This is intended for merchant payments (shopping, dining, retail purchases abroad), not all UPI use cases. However, the actual usable limit often depends on several layers operating simultaneously. Even if the UPI network permits a ₹2 lakh transaction, the issuing bank may impose a lower cap, the UPI app may apply risk-based restrictions, and foreign merchants themselves may set their own payment ceilings. some merchants abroad may allow only smaller transaction values despite higher network limits because of local compliance rules, terminal restrictions, or currency conversion controls, explains Mahajan. For example, a luxury store abroad may technically support UPI but permit only transactions below a certain amount. This is why experts recommend confirming payment acceptance and limits before completing large purchases overseas. Is using UPI abroad cheaper than credit cards and forex cards? One of the biggest reasons travellers are experimenting with UPI abroad is cost.ET Online

Can you use UPI abroad? Here’s what Indian travellers must know about charges, limits and security risks - The Economic Times

Indian travellers are increasingly using UPI abroad for convenient payments, but understanding its limitations and risks is crucial. While cheaper than cards in select countries like UAE and Singapore, UPI acceptance is uneven, and backup payment options are essential. Users must be aware of transaction limits, potential failures, and fraud risks.

1,267 words~6 min read