Show Caption

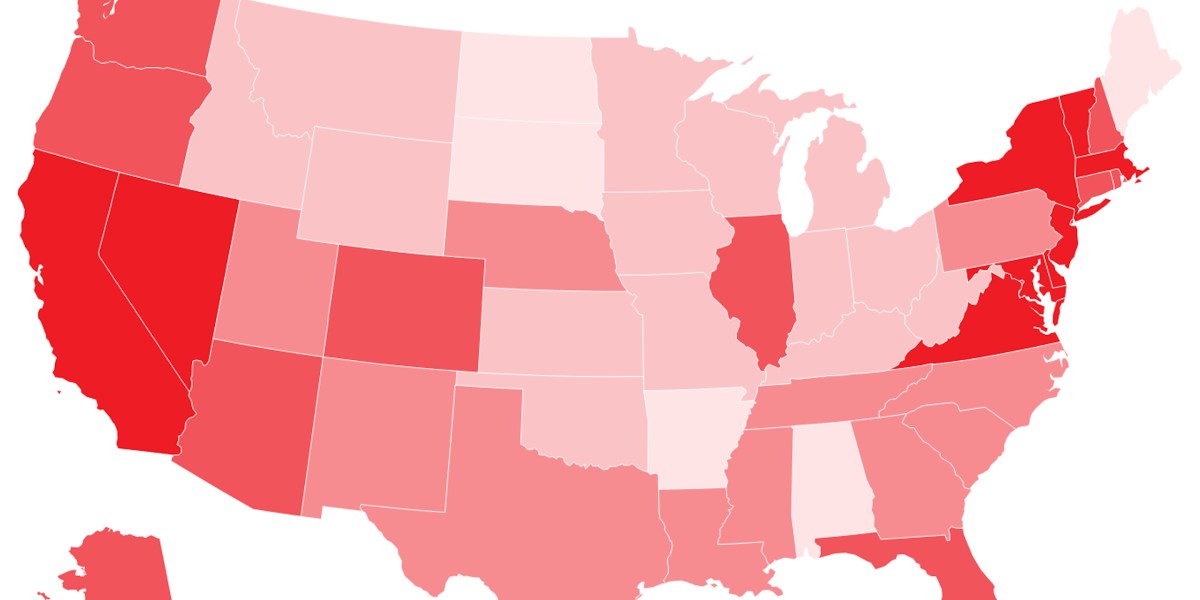

Buying a home feels unaffordable to millions of Americans, but so is owning a home, especially among seniors, data show.Fifty-four percent of the nation’s 35 million mortgage-free homeowners are age 65 or older, a group that represents just over a third of all U.S. homeowners, according to housing research firm ResiClub. Among that population, roughly 64% own their homes outright, it said.Yet, a record 12.5 million senior households, or more than a third of the age 65+ population, may be feeling "house poor," or spending a disproportionately large percentage of their monthly income on housing costs, data show. In 2024, they spent more than 30% of their income on housing, with half of them spending more than 50%, according to U.S. Census data.The government's general rule of thumb is to spend no more than 30% of gross income on housing, including rent or mortgage payments, property taxes, insurance, and utilities, to avoid being cost burdened. Since 2019, older adult households also made up roughly half of all newly cost-burdened households, according to the Harvard Joint Center for Housing Studies."That’s a sign that housing affordability challenges don't disappear at retirement age, and can be extra problematic for older adults on fixed incomes," wrote Christine Healy, head of brand at CareScout, in a report."Even seniors who did everything right aren't safe," she added. "For homeowners who paid off their mortgages entirely, median housing costs have still climbed 35% since 2019 – about 1.5 times faster than their incomes grew."What's causing the housing squeeze for seniors?About every expense related to housing has skyrocketed since the pandemic, faster than the 28.67% overall pace of inflation, making it harder for seniors − even those without a mortgage − to keep up, experts said.For instance, rent since the pandemic has increased by 36.2% nationally, according to property listings company Zillow's March report, while median property taxes rose about 30% between 2019 and 2024, nonprofit Tax Policy Center said. Home insurance premiums surged by 40.4% between 2019 and 2024, said rate comparison site LendingTree. Electricty prices soared 40% between 2020 and 2025, according to the Bureau of Labor Statistics."These staggering increases have proved insurmountable for many Americans, but no group has been more impacted than seniors, especially those on fixed incomes," Healy said. "Property taxes, utilities and insurance are now eating away at their savings – and unlike younger Americans, many seniors can't simply take on a second job or trade up to a higher salary to compensate."Suffering differs geographicallySeniors are being hit harder in some places more than others, according to an analysis by long-term care solutions company CareScout that looked at the share of seniors who spend 30% of their income on housing, real estate taxes, home insurance, electric bills, assisted living costs, and more across the United States.Seniors are most likely to be cost-burdened in California and least so in West Virginia, which was helped by having the nation's lowest property taxes ($881) and the smallest share of households facing high insurance costs (10.2% pay $2,000+), CareScout said.How can seniors cope?Preparing early is always the best way to avoid a housing squeeze, said Steve Azoury, chartered financial consultant and owner of Azoury Financial. He suggested:Look at what your sources of income are to pay expenses and how long they'll last, even with some annual inflation.If applicable, consider a scenario in which one spouse dies and how taxes, home insurance and other expenses will be paid.Check for local property tax breaks and other benefits for seniors. More than nine million eligible seniors are missing out on $58 billion in benefits, according to the National Council of Aging. NCOA's benefits check tool can show you what you may be missing. For surviving spouses, there are also nonprofit organizations like Wings for Widows that help them navigate their new financial situation.Consider downsizing sooner and invest some of the money to be used for income later. Married couples filing jointly who have lived in the home as a primary residence for a while can exclude up to $500,000 of capital gains from the sale. If a spouse dies, that exclusion drops in half two years after death.Buy whole life insurance while you're young so if a spouse passes away, the surviving spouse receives an immediate tax-free, lumpsum payment "that's not subject to stock market movements and comes in handy when needed," he said. Some of the money can be used to pay expenses and the rest invested to generate income.Consider renting out a room in your house to earn extra income, if you're comfortable.If you love and want to keep the house you own, consider a reverse mortgage if you can't afford monthly home equity loan payments. Reverse mortgages earned a bad reputation earlier for predatory lending practices, high upfront fees, and a lack of consumer protections, but they're more regulated now.Reverse mortgages are insured by the Federal Housing Administration as a standardized, government-insured loan option with defined guidelines and borrower protections. "You can get money to use for income that's paid each month," Azoury said. "You still own the house and pay the taxes, utilities, insurance and upkeep but now, you have a little extra money. You have the option to stay in your house until you die or you can sell it and pay off what you owe."(Updated Christine Healy's title to reflect that she represents CareScout because CareScout purchased Seniorly.)Medora Lee is a money, markets, and personal finance reporter at USA TODAY. You can reach her at mjlee@usatoday.com and subscribe to our free Daily Money newsletter for personal finance tips and business news every Monday through Friday.