Geoff Robins /AFP via Getty Images

For most Americans, the math on buying a home has become hard to make work. Mortgage rates remain well above the pandemic-era lows that briefly made ownership feel attainable for a wide swath of buyers. Home prices absorbed those rate increases without retreating, rising across most of the country even as borrowing costs climbed sharply. The result is a market where the typical buyer now spends roughly 40% of income on monthly housing costs, well above the 30% threshold that financial advisors have long treated as the outer boundary of responsible spending.

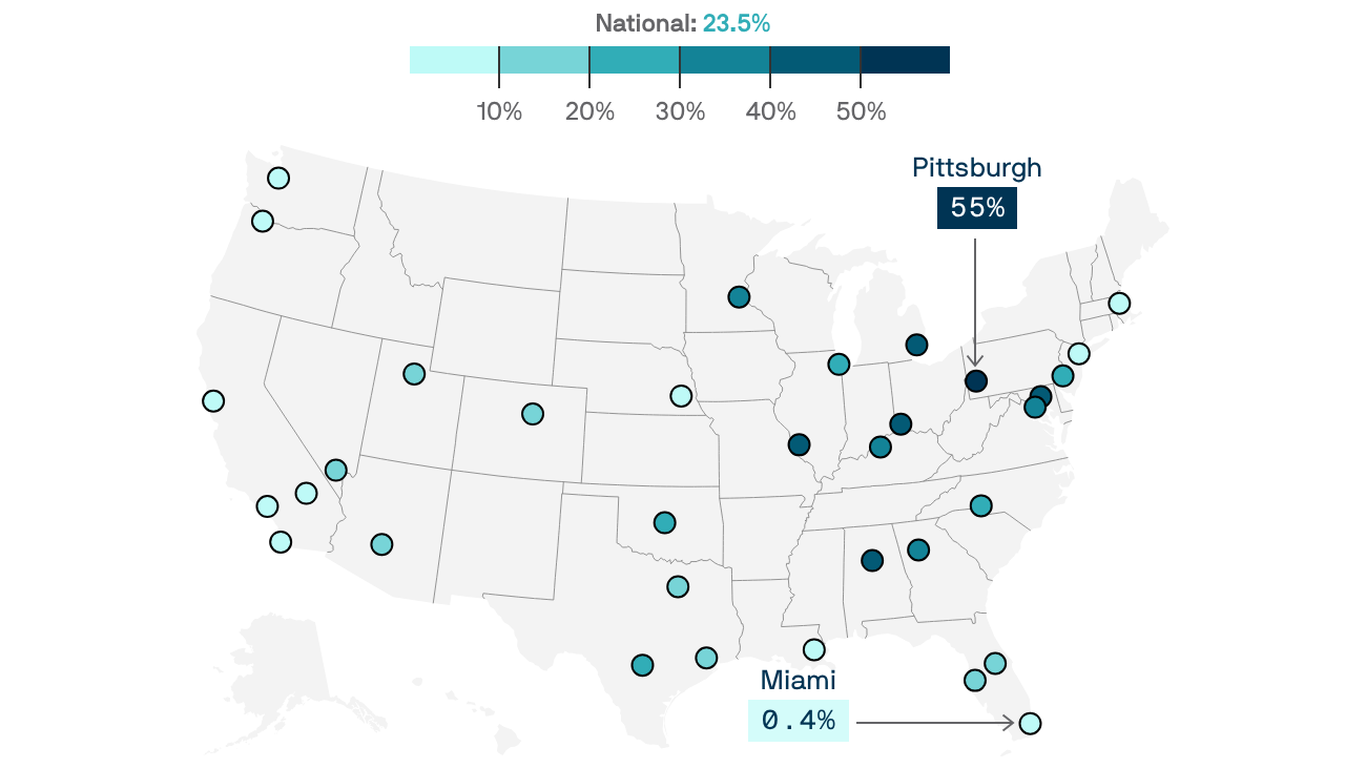

That gap between incomes and prices is not uniform. A handful of U.S. cities have largely avoided the worst of that squeeze. These are places where wages are strong enough relative to local prices that a median-income household can still find a wide selection of homes within budget. What connects them is a common history: decades of industrial decline suppressed home values in each of these cities, leaving behind markets that national price surges have not yet overtaken. The narrowing is already underway in several of them, as buyers priced out of more expensive metros have begun moving in and pushing values upward.