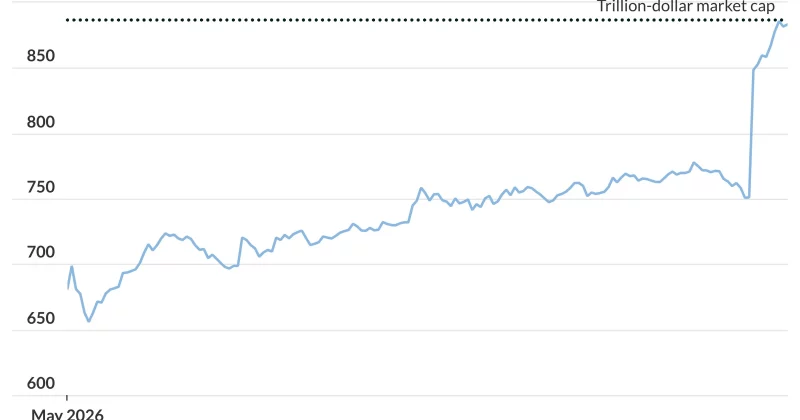

Micron Technology has quietly become one of the most consequential stocks in the entire S&P 500 this year. The memory chipmaker’s shares have surged more than 70% year-to-date, pushing its market capitalization past the $1 trillion mark and its stock price to all-time highs near $900.

The numbers don’t add up, until they do

Micron’s forward price-to-earnings ratio sits somewhere between 5.5x and 11x, depending on which estimates you use. The S&P 500’s average forward P/E hovers around 20x. In English: the market is pricing Micron’s future earnings at roughly a quarter to half of what it charges for the typical large-cap stock.

The explanation lies in Micron’s sector. Memory chips are famously cyclical. Boom years of constrained supply and fat margins tend to be followed by gluts that crush pricing. Investors who’ve lived through previous cycles instinctively discount future earnings more aggressively than they would for, say, a SaaS company with predictable recurring revenue.

Why this cycle might be different (or not)