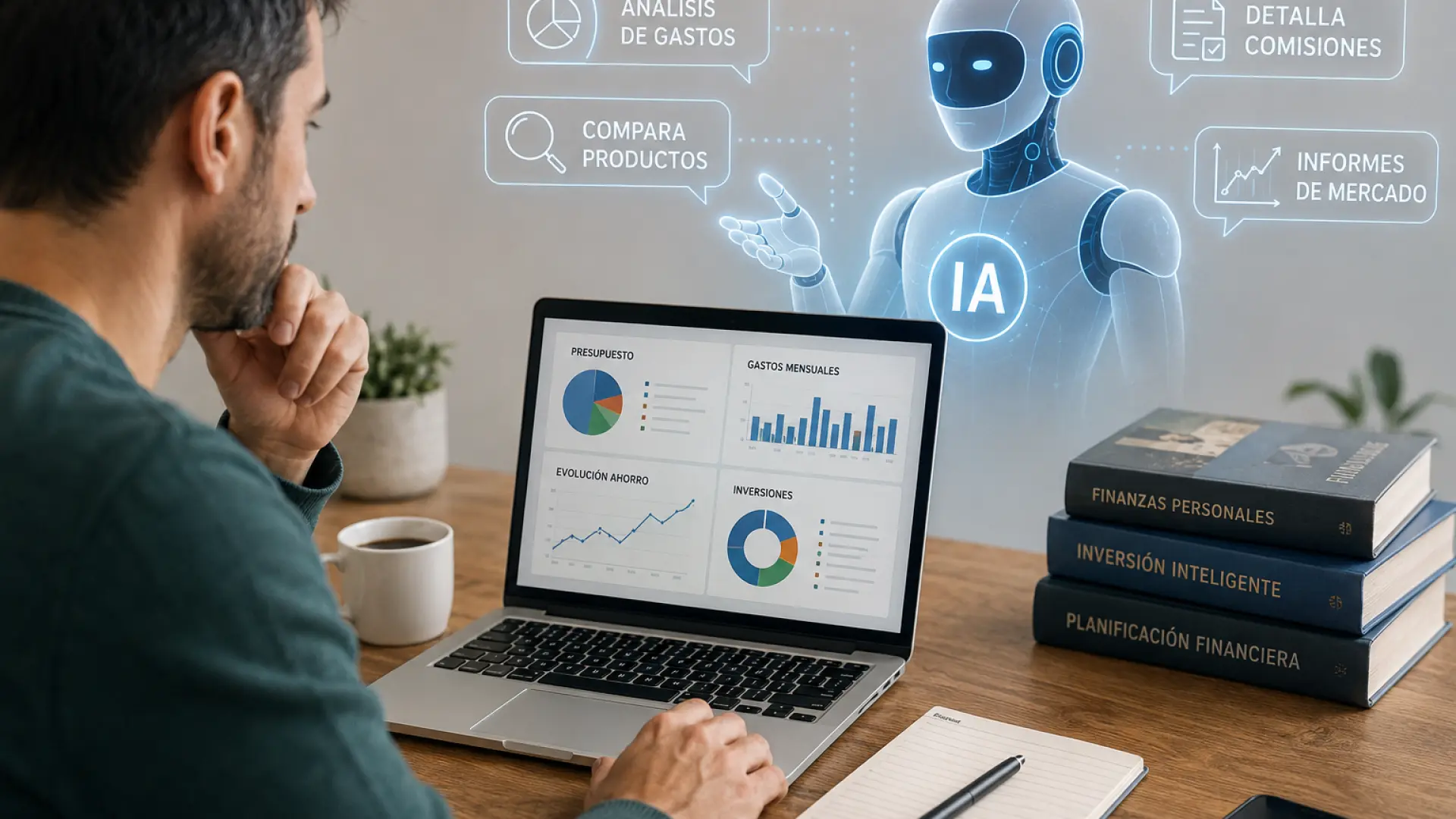

SynopsisA retirement economist expresses concern over AI's use in financial advice, noting its limitations despite providing basic guidance. The article emphasizes understanding investments, diversifying across various assets, avoiding speculative ventures, and paying low fees. It cautions that time doesn't always mitigate market risk, highlighting the inherent link between risk and return.AgenciesWhen someone told me recently that her favorite use of AI is for financial advice, I was horrified. I am a retirement economist, and my first reaction was self pity: Now I know how doctors feel when people use AI for medical questions.Then I went home and gave it a try. It was not terrible — it gave a clear and engaging explanation of the conventional wisdom on saving and investing. It was the equivalent of a mediocre financial planner, but without the personal touch. That’s probably better than nothing, and it’s bound to become more common as more brokerages offer AI advisers to less wealthy customers.But it comes with some major weaknesses. And with most Americans unable to answer basic questions about financial markets — only about half believe it is safer to own many stocks instead of a few — I thought it might be appropriate to offer a kind of primer. Finance 101 still explains almost everything, but maybe some of the language could be clearer.BloombergOne issue I noticed with the chatbot I used was that it often gave the wrong reasoning behind its advice. Most of the time, that’s not a problem, since most people don’t care — they just want to be told what to do. But the faulty reasoning shows the limits of an AI adviser in the event of an unusual personal or financial event, which is inevitable. There is no shortage of advice about retirement investing, and the number and types of assets are constantly expanding. Yet there is somehow also less transparency and understanding. So here is a kind of guide to understanding how to save and invest in this new market, especially for people who use AI as their financial adviser.Know what you are invested in. Is it a stock fund, full of public companies that track the market? A municipal bond fund? Commodities (not my favorite)? It’s important not to blindly trust a fund if you don’t know what exactly is in it — and then once you do, to ensure that all the assets have a market price. You don’t need to track that price daily, or even name every security you own, but you should know what kind of assets you have. Just as you should know where your food comes from, you should know what’s in your portfolio.Diversify. The future is uncertain: AI could transform the economy and bring unprecedented growth, or it could just be meh. Governments are borrowing more than they’ll ever pay back even as populations are shrinking. There is no way to predict the future or time markets, so the best thing to do is buy lots of different stocks, ideally from different countries.Don’t invest in anything weird unless you’re prepared to lose it. “Diversify” does not mean buy everything. Invest in assets that make some sense, for example a fund of companies that are expected to have future profits. This kind of investing is positive sum — that is, when the economy grows, those investments do well. More exotic assets, such as crypto or in betting markets, are zero-sum — for every bet, someone wins and someone loses, and odds are you will be loser. It can be fun to invest in these assets, but it’s more entertainment than investment.Pay low fees. The good news is you can follow the three rules above without having to pay much. In fact, the less you are paying, the more likely you are to be diversified in straightforward assets. Stay away from anything that promises high returns and low risk, because the only way investment firms can achieve that is by either charging a big fee that undermines that high return, or exposing you to a hidden risk that emerges at the worst possible moment.Time is probably your friend, but not always. When I was using the AI as my adviser, it told me that “time is your protection from volatility” and that “stocks are volatile in the short run, but reliable in the long run.” This is wrong. More time in markets means more risk, which is one reason long-term insurance policies cost more. True, markets often bounce back from a drop, but they can also have decades of bad returns (see, e.g., Japan). It can be a good idea to invest more in the stock market when you are young, but that’s because most of your wealth then is in your future earnings — not because time makes investing less risky.Managing personal finances is much harder than most people think. There is a lot of advice out there that is perfectly fine most of the time, even from AI, but there are always situations — losing your job when the market is down, for example — that call for more tailored advice. The main thing to remember — regardless of your financial situation or your age or your investing horizon or your hopes for retirement — is that there is no extra return without extra risk. Anyone who tells you different, whether they’re human or AI, is trying to sell you something.Read More News onRead More News on

Can AI financial advice help you retire more comfortably?

A retirement economist expresses concern over AI's use in financial advice, noting its limitations despite providing basic guidance. The article emphasizes understanding investments, diversifying across various assets, avoiding speculative ventures, and paying low fees. It cautions that time doesn't always mitigate market risk, highlighting the inherent link between risk and return.

906 words~4 min read