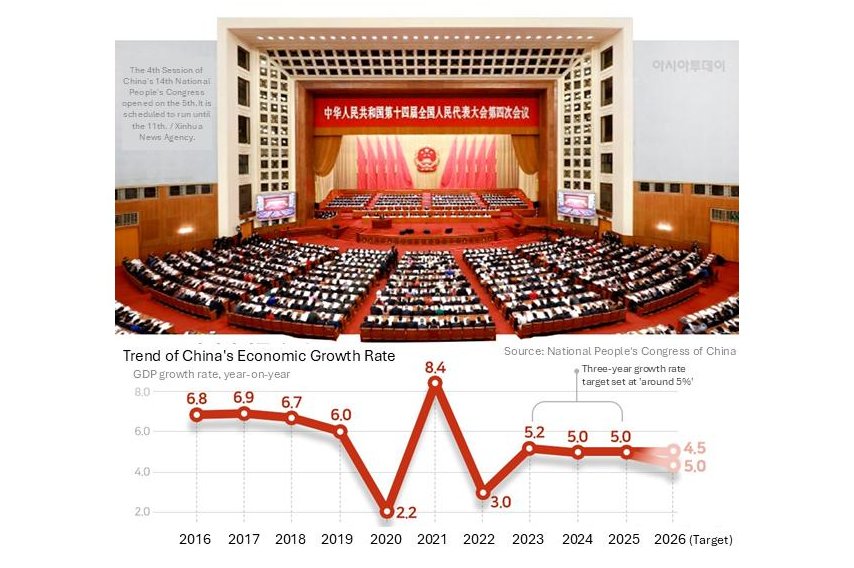

China’s decision to set a reduced GDP growth target of 4.5–5.0 per cent for 2026 marks another step in a long-running structural transition. Chinese policymakers have presented it not as a sign of economic weakness but as a deliberate pivot away from growth at all costs towards high-quality growth, with emphasis on productivity, technological upgrading and comprehensive development.

Trading partners face a China that is simultaneously slowing overall and becoming more competitive in selected industries. Investment has flowed into advanced manufacturing, clean energy and digital technologies. In sectors such as electric vehicles (EVs), batteries and solar power, Chinese firms occupy leading positions in global markets. China also hosts the world’s largest stock of industrial robots and has accelerated deployment of AI applications in manufacturing, healthcare and logistics.

Yet total fixed asset investment fell 3.8 per cent in 2025, dragged down by a 17.2 per cent collapse in property investment. Even excluding property, fixed asset investment was down 0.5 per cent.

Three structural headwinds — a spent reform dividend, a reversing demographic dividend and a weakening globalisation dividend amid trade frictions — are well documented. Compounding these, the property sector remains depressed. Most forecasts place a sustained recovery no earlier than 2027.