Soaring energy costs have grabbed headlines around the world the past two months, but prices across the solar supply chain are marching to their own beat, writes Hanwei Wu of OPIS. Oversupply in Asia continues to distort markets, with either sharp price falls or tepid price gains.

May 25, 2026

From the magazine

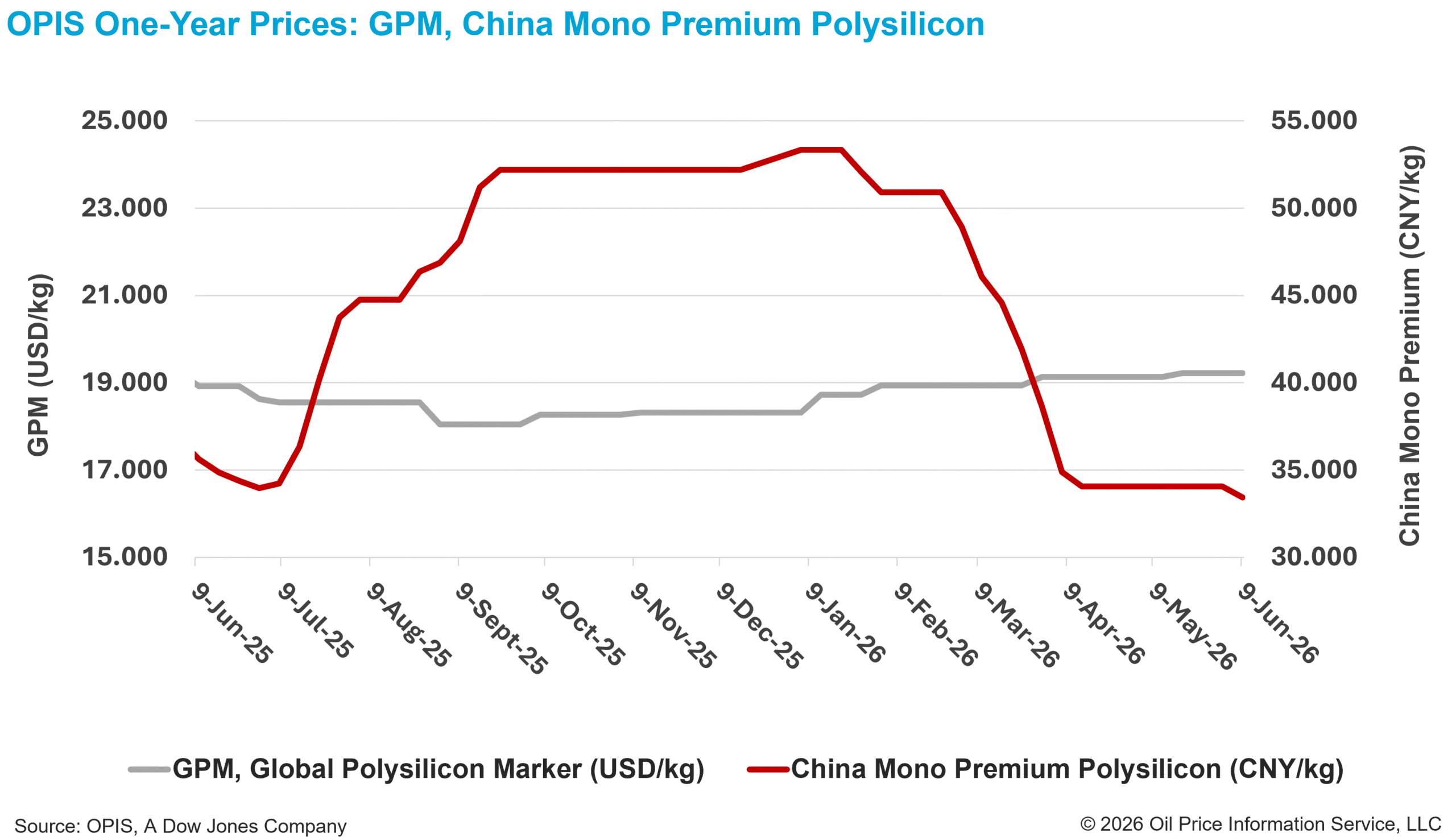

The Global Polysilicon Marker (GPM) has hardly moved since the latest outbreak of war in the Middle East. The OPIS benchmark for polysilicon produced outside China was assessed at $19.138/kg, or $0.040/W, as of April 14, only up 1% from Feb. 24, the week the war in Iran started. Over the same period, the China Mono Premium – OPIS’ assessment for mono-grade polysilicon used in n-type ingot production – fell by 33% to CNY 34.071 ($4.99)/kg, or CNY 0.072/W; FOB China TOPCon M10 cell fell by 11% to $0.05/W; FOB China TOPCon module rose by near 2% to $0.118/W.

Such price movements pale in comparison to the wild swings seen in oil markets, particularly in Asia. Prices of jet fuel and diesel, the transport fuels most affected by the Iran war, have more than doubled from $92.72/barrel (bl) to $210.73/bl and $92.68/bl to $185.75/bl, respectively, on a free-on-board Singapore basis over the same period, according to OPIS data.