In this article

The S&P 500

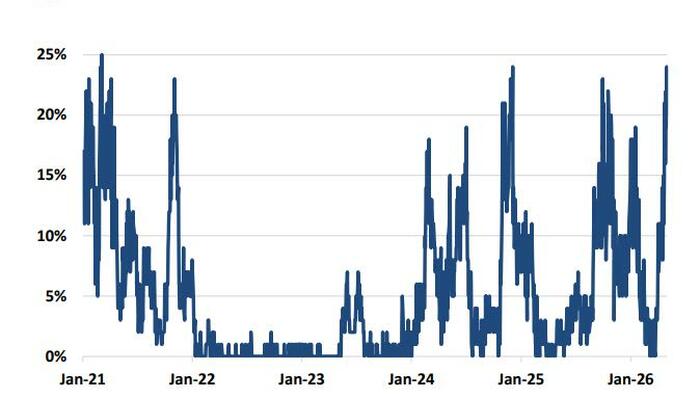

The arithmetic is straightforward. Protection costs less when volatility is compressed. With the VIX

sitting in the high teens, well below the stress levels that accompanied the March selloff, the implied volatility priced into put options has pulled back sharply. Buying a one-month 2-2.5% out-of-the-money put (about 30 “delta”, sometimes written as 30^) today costs a fraction of what it cost when the market was in free fall. If you’re the type of investor that likes to hedge when you can, rather than when you have to, now’s your chance.

And there’s good reason to think hedging still makes sense, consider the conditions that drove the rally: tariff progress, earnings resilience and hopes the bottleneck in the Strait of Hormuz might resolve. That and momentum are not the same as resolved fundamentals. The Federal Reserve remains effectively sidelined as higher oil prices have pushed inflation higher. Consequently, Treasury yields are elevated relative to year-to-date lows and gold, despite retreating from its January peak, continues to signal that institutional safe-haven demand has not evaporated.