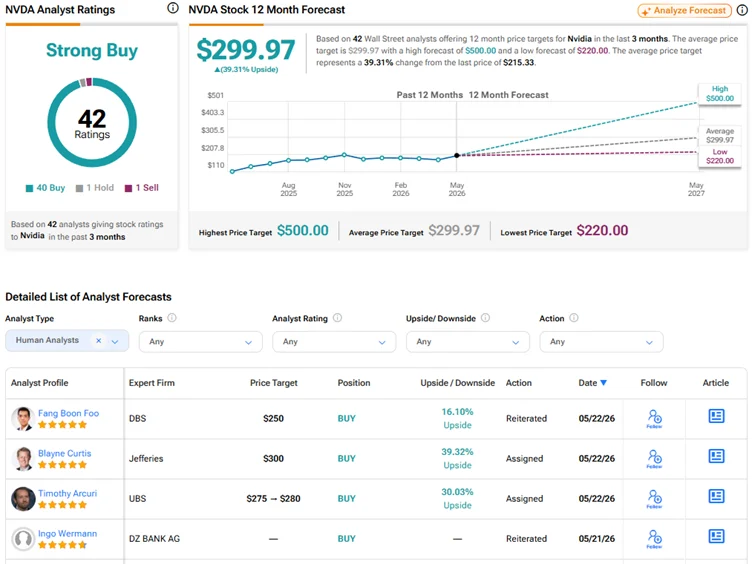

Baird just slapped a $500 price target on Nvidia, up from $275, while maintaining its Outperform rating. That is not a modest revision. That is the kind of move that makes other analysts quietly re-examine their spreadsheets.

The new target places Baird firmly at the top of Wall Street’s range for the chipmaker. Current analyst estimates span from $140 to $350, with a median clustered around the mid-$250s. Baird’s number isn’t just above the consensus. It’s in a different zip code.

What’s driving the conviction

Nvidia’s most recent quarterly results provided the fuel for Baird’s aggressive stance. Revenue hit $57B, representing 62% year-over-year growth, powered almost entirely by data center AI GPU demand.

In English: companies are spending staggering amounts of money on the chips that make AI models work, and Nvidia makes nearly all of those chips. The company isn’t just riding the AI wave. It built the surfboard, the wave machine, and most of the beach.