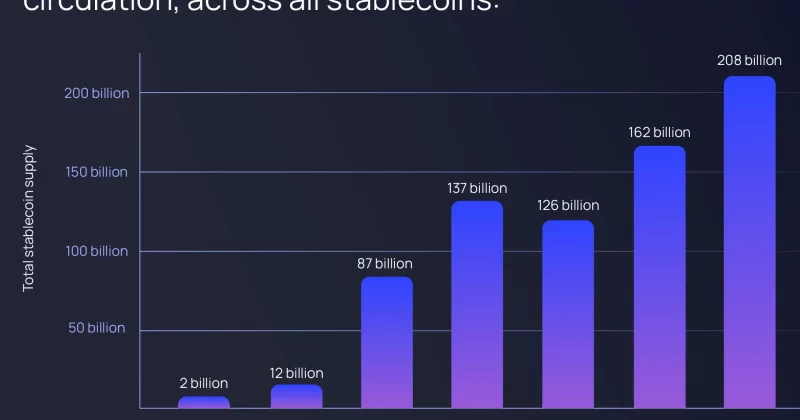

The stablecoin market is worth well over $100B. Non-dollar stablecoins account for roughly 0.2% of it.

The dollar’s quiet monopoly

USD-denominated stablecoins account for over 95% of total stablecoin market capitalization, according to analysis from the Bank for International Settlements and the European Central Bank. Tether’s USDT and Circle’s USDC are the two gravitational forces holding the ecosystem together, with fiat-backed stablecoins broadly constituting about 87% of all circulating supply.

Non-dollar alternatives barely register. Euro-pegged stablecoins, the most prominent alternative category, are concentrated in just two dominant tokens. Even with Europe’s MiCA regulatory framework supposedly giving euro stablecoins a clearer legal runway, they haven’t managed to move the needle.

The core issue is a chicken-and-egg problem that non-dollar stablecoins can’t seem to escape. Without deep liquidity, traders won’t use them. Without traders using them, liquidity never develops. And without liquidity, DeFi protocols have no reason to integrate them as base pairs or collateral assets.