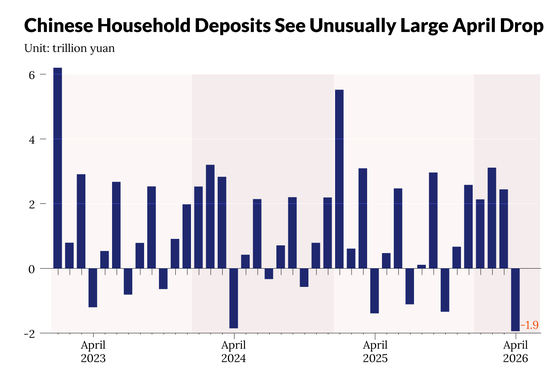

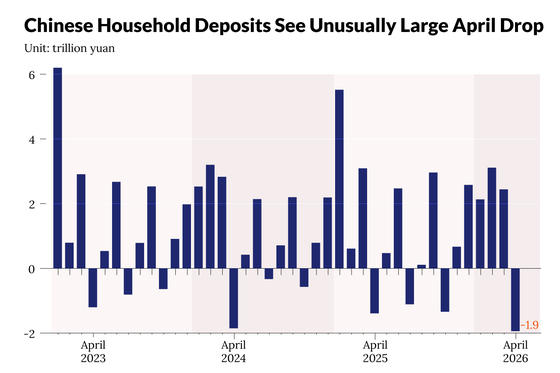

1. The period of easily accessible, high-interest deposits in China is coming to an end, evidenced by a sharp decline in interest rates offered on certificates of deposit. For example, deposit products that offered rates as high as 5.3% in 2021 now struggle to offer even 2%, marking a significant shift for Chinese savers as their deposits mature and need to be reinvested in a much lower-rate environment. [para. 1][para. 2][para. 3]2. The maturation of a large wave of long-term household savings deposits is a major event for China’s financial system. According to Zou Lan of the People’s Bank of China, many three- and five-year deposits are being repriced this year. Market estimates based on bank disclosures suggest that time deposits maturing in 2024 with original terms longer than one year amount to between 30 trillion yuan ($4.3 trillion) and more than 70 trillion yuan. This repricing will not only affect household wealth but could also have significant implications for bank funding costs and the broader allocation of liquidity in the financial system. [para. 4][para. 5][para. 6]3. Chinese banks experienced a boom in household deposits starting after 2020, as pandemic concerns led to more precautionary saving and aversion to volatile capital markets. During this time, time deposits and certificates of deposit frequently offered rates above 3%, and sometimes up to 5%. However, deposit rates have since dropped, quotas for long-term products have tightened, and some products have been withdrawn. Term structures even became inverted, with longer-term products offering lower rates than short-term ones. About 61% of maturing household time deposits are set to mature in the first quarter, per CICC estimates. [para. 7][para. 8][para. 9]4. For banks, the rollover of these maturing deposits at much lower current rates offers significant relief in funding costs. By late October, new three-year and five-year deposits had average rates of around 1.7% and 1.5%, nearly halved from 2022–2023 levels. Lowering interest paid out on deposits may save banks about 150 basis points in funding costs by early 2026, but it increases the risk that households will seek alternative, higher-yielding investments. [para. 10][para. 11]5. Despite this, analysts do not expect a large-scale withdrawal of funds from the banking system. Chinese household risk appetite remains subdued as they continue repairing their finances. Still, even a small reallocation of the huge maturing deposit base, estimated to be concentrated at state-owned "Big Six" banks, could be significant. Regional and rural banks, with older and more conservative customer bases, are expected to retain most deposits, while larger urban-centered banks may face more retention pressure. [para. 12][para. 13][para. 14][para. 15][para. 16]6. Among alternatives, wealth management products (WMPs) have become an attractive option. Surveys indicate maturing deposit holders prefer WMPs, followed by cash, insurance, bond, and equity funds. Bank WMP balances reached a record 33.3 trillion yuan in 2023, up 11% year-on-year, with yields averaging 1.98%. Cash management WMPs offer ~1.4%, and fixed-income WMPs about 2.2%, both above the 1.25% available from three-year deposits at major state-owned banks. [para. 17][para. 18][para. 19][para. 20]7. Insurance is also a growing avenue for redeploying savings. Savings-type insurance products, often promising a guaranteed rate around 1.75% plus dividends, are appealing to depositors avoiding risk. Bancassurance (insurance sold via banks) may attract 1.1 trillion yuan in new funds this year. However, buyers must consider policy fees, commissions, and lock-up periods. Break-even takes six to eight years, or three to five in peak campaigns, with limited liquidity until then. [para. 21][para. 22][para. 23][para. 24][para. 25]8. A significant shift toward riskier assets, such as equities or bonds, appears unlikely. Chinese households remain cautious, and a meaningful increase in stock investment would require sustained market gains. Bond yields are uncompetitive after years of compression, and gold remains a niche hedge. The most probable outcome is a slow rebalancing, as households gradually seek modestly higher returns in safe, alternative products while repriced deposits settle at lower rates. [para. 26][para. 27][para. 28]AI generated, for reference only

Cover Story: China’s Deposit Repricing Tests Banks and Savers as Trillions Come Due

As long-term deposits mature this year, lower rates are reshaping bank funding costs and household asset allocation

655 words~3 min read