Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

With revenue surging and profits accumulating, it’s not hard to understand why there’s been so much investor excitement around the memory company. Indeed, Micron is one of only a handful of companies capable of providing the advanced memory needed to run high-octane AI workloads.

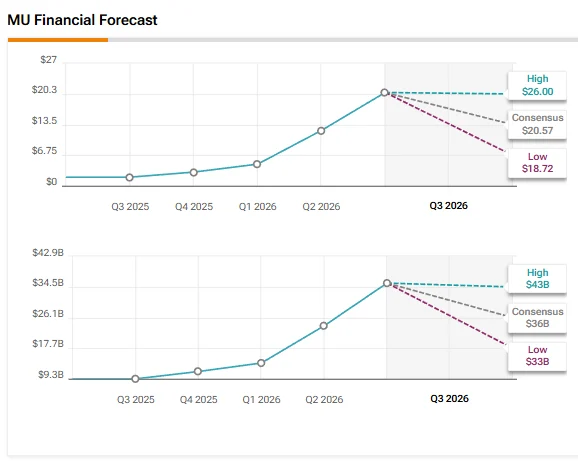

That dynamic has propelled demand into the stratosphere, while the growing appetite for memory products has also given Micron incredible pricing power. The company is guiding for $33.5 billion in sales (which would represent sequential growth of ~$10 billion), along with a gross margin of ~81%, in the current quarter.

Still, for all the positive movement, there is a lingering fear that Micron is playing on borrowed time. The memory industry is historically cyclical, the thinking goes, meaning that it’s only a matter of time before things start to go south.

That’s not a concern that top investor Keithen Drury shares.