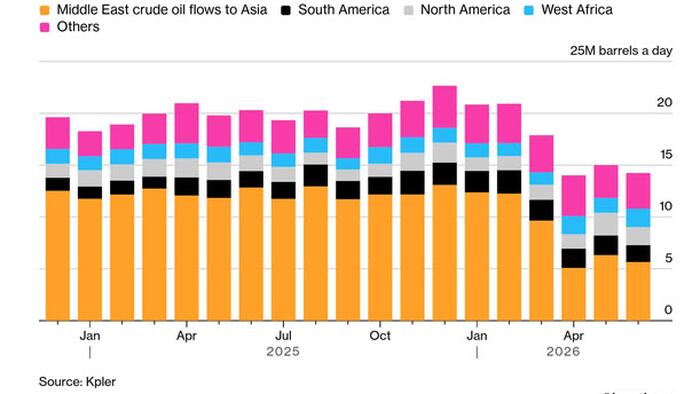

Asian refiners have been among the hardest hit by the severe disruption of crude shipments through the Strait of Hormuz. Refiners in China, India, South Korea, Japan and Singapore, among others in the region, are heavily reliant on crude imports from the Mideast. Since the latest war in the Mideast began on Feb. 28, Asian refiners have scrambled to find alternate crudes, leaning heavily on Latin American, West African and US barrels. But many regional refiners also have slashed run rates, cutting throughputs by 3.9 million-4.2 million barrels per day combined over March and April. That has not only lowered Asia-Pacific's overall demand but also slowed the race to secure replacement grades in the short term. Of the 15 million b/d of crude and condensate that used to typically pass through Hormuz (excluding Iranian barrels), roughly 13.5 million b/d went to Asian markets in 2025, representing close to 60% of the region's crude imports last year. Inventory releases from Japan and South Korea have helped partially plug the regional supply gap. But with elevated Brent futures prices and crude spot price differentials making the cost of replacement crudes "so high," according to three Northeast Asian refiners, regional imports have plunged. Asia-Pacific's total seaborne crude imports fell from 21.1 million b/d in February to 17.9 million b/d in March and to 13.8 million b/d in April, according to data intelligence firm Kpler. The decline started slowing in late April and May, as replacement crudes snapped up in the early days of the conflict began arriving. Through May 13, total monthly Asian seaborne crude imports had climbed back to 14.4 million b/d, according to Kpler data.

Long-Haul Crudes Help Asia Fill Mideast Supply Void

Crudes from Latin America, West Africa and the US help Asian refiners in their scramble to fill the Hormuz-sized supply gap.

274 words~1 min read