Insurance practices in an age of climate volatility raise troubling questions about home ownership and housing affordability – the bedrock of the American middle class

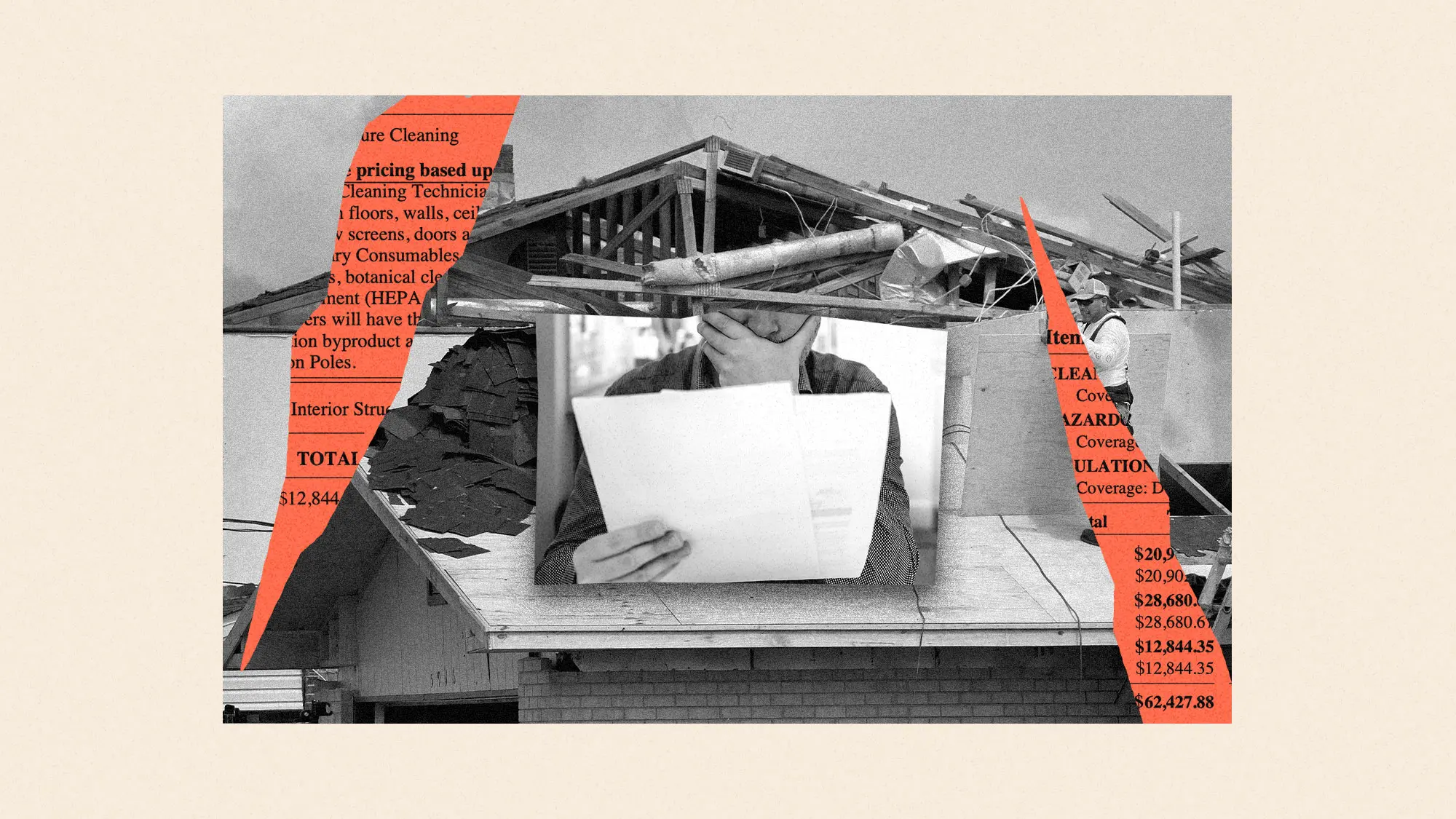

For a few frenetic days last January, after losing their midcentury ranch home to the wildfires that ravaged Los Angeles, Jessica and Matt Conkle thought they could see a glimmer of hope.

Their insurance company, State Farm, had sent emergency response teams to Altadena, where they lived, and they filed a claim right away. It wasn’t long before they received a check that covered four months of living expenses.

Then the process bogged down. Like many homeowners, they imagined that since they had suffered a total loss they could collect on the full value of their coverage. Instead, they had to negotiate over the value of each of their lost possessions with a claims adjuster, only to have to start again with a second adjuster and then a third – a process they believe was expressly designed to deter them from moving forward.

Months went by with no discernible progress. They felt they were being shortchanged on item after item, and when they attempted to challenge the valuations State Farm was offering, they struggled to get anyone to respond.