Effects on inflation and employment have not been as bad as feared – but could still materialise with full force in 2026

W

hen Donald Trump took office last January, most economists feared what would happen if he raised tariffs. The expectation was that, as the new duties drove up prices of consumer goods and inputs – affecting households and companies, respectively – surging inflation and falling real incomes would follow. This would be a supply shock, so the US Federal Reserve could not do much to counteract it.

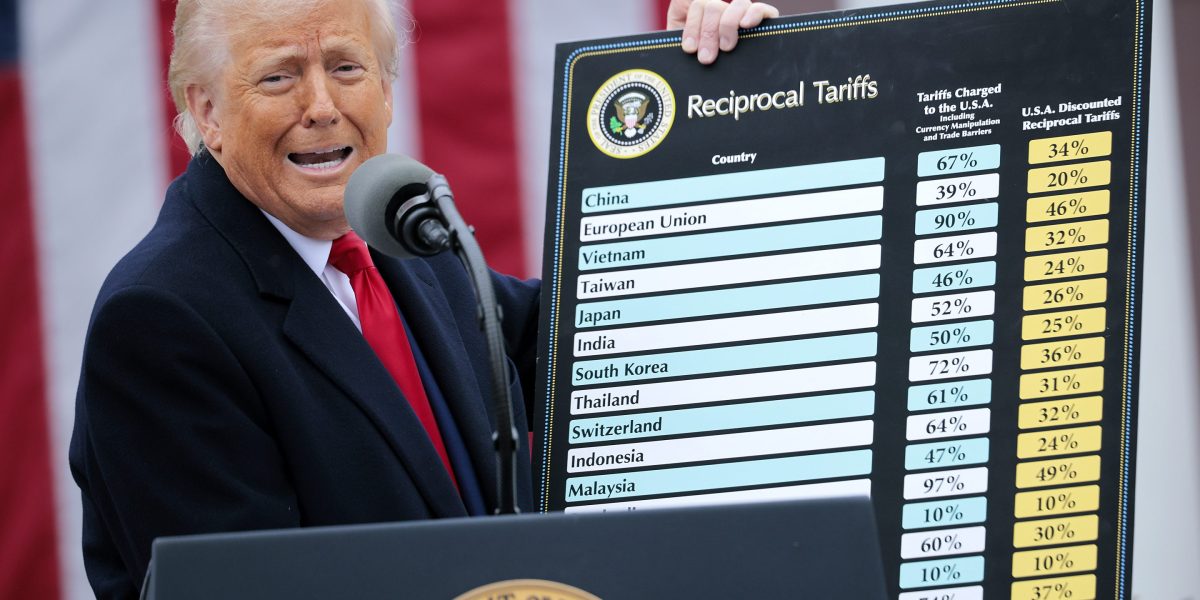

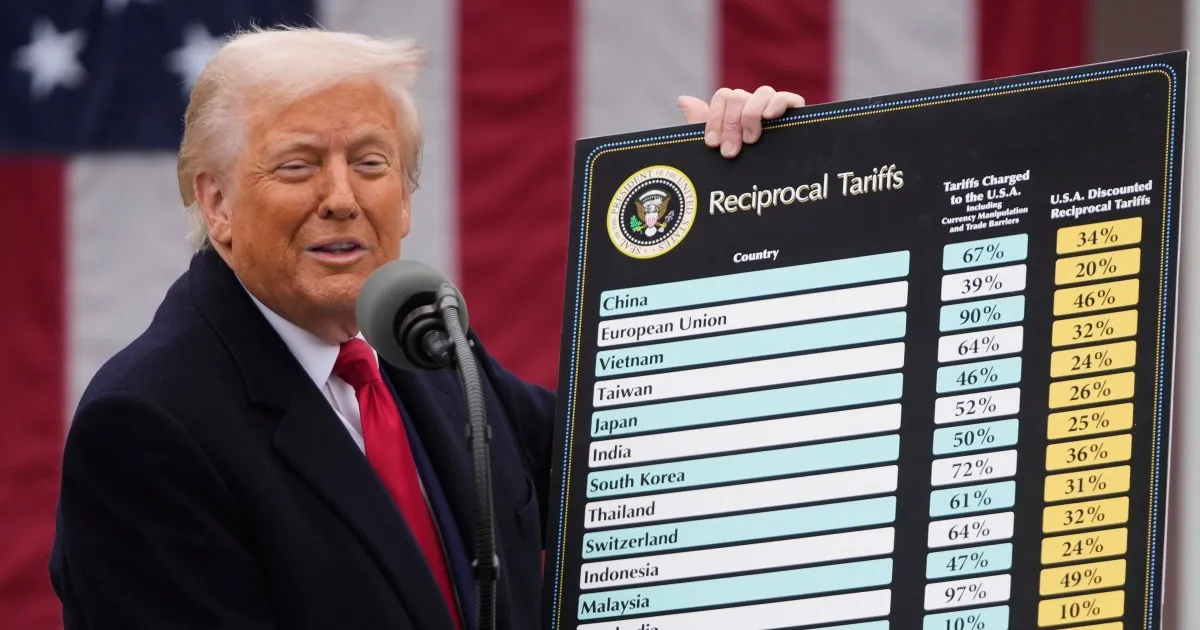

Trump did raise tariffs to shocking levels, violating international agreements and blowing up the Republican party’s oft-professed commitment to free trade. In terms of severity and disruptiveness, Trump’s 2025 tariffs went far beyond the already harmful tariffs of his first term, and even beyond the infamous Smoot-Hawley Act of 1930. According to the Yale Budget Lab, the average effective tariff on US imports rose from 2% to 18%, the highest level since the 1930s, this year. Add to that the uncertainty caused by frequent and inexplicable policy changes, and large adverse effects on inflation, employment and real incomes appeared all but inevitable.

But things did not turn out as anticipated. It is possible that consumer price inflation (CPI) did not rise at all: the most recently reported rate, for the 12 months ending in November, is 2.7% – the same level as in the closing months of 2024. (Of course, the price level is higher, contrary to Trump’s claims.) The unemployment rate rose only a little, from 4.1% at the end of 2024 to 4.6% in November. Economic growth probably slowed toward the end of the year, but the situation remains unclear, because a US government shutdown delayed data collection.