ByRobert W. Wood,

Senior Contributor.

California has long been the land of high taxes. It’s top 13.3% income tax does not distinguish between ordinary income and capital gain. The top 13.3% tax can grow to 14.4% in some cases. There are audit and administration concerns too. California’s Franchise Board is notoriously tough, many say tougher than the IRS. So far, California has not had a wealth tax, although it has been proposed a few times. The latest proposal is targeted, and it may stand a better chance of passing than the wealth tax proposals of the past.

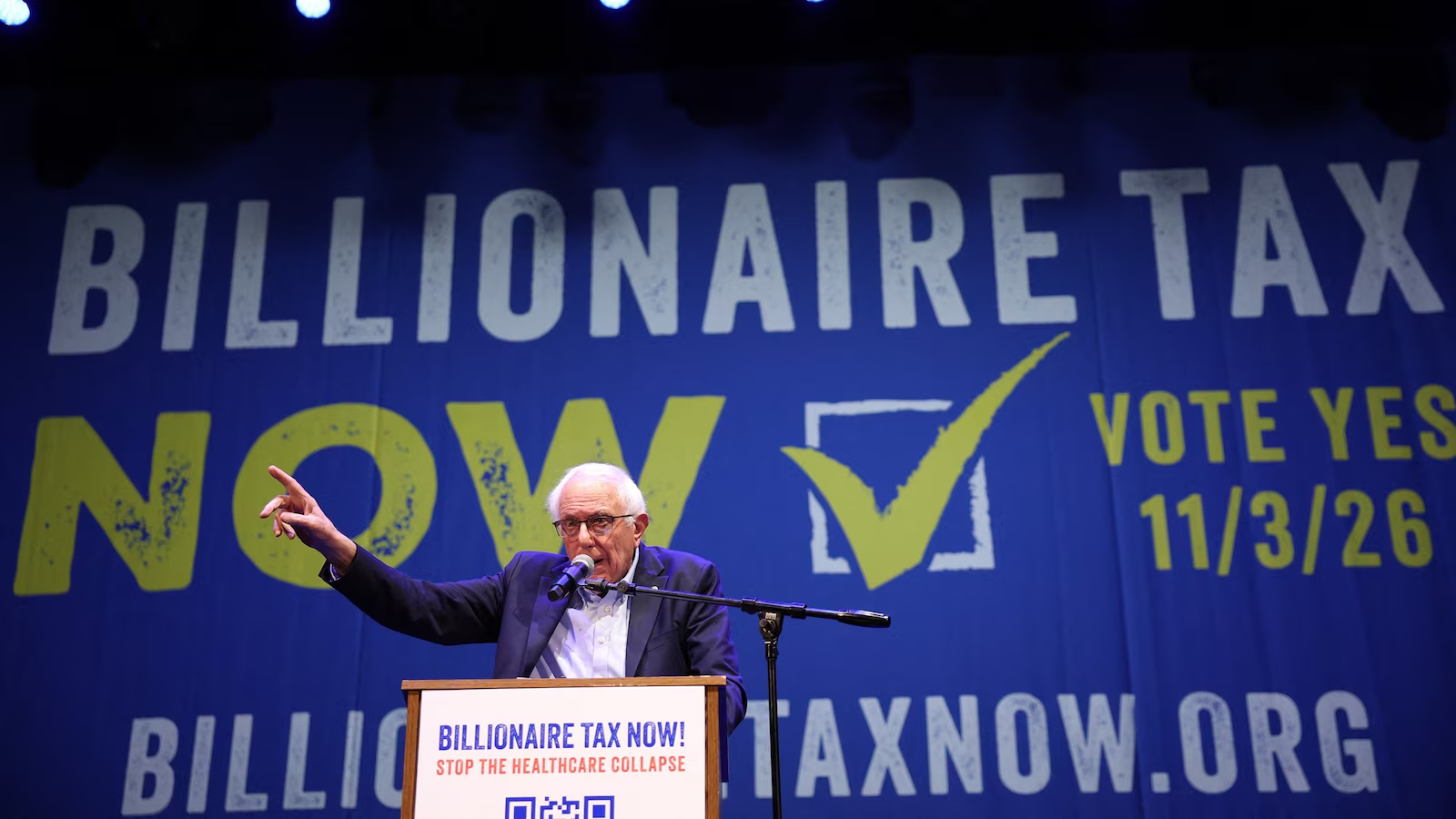

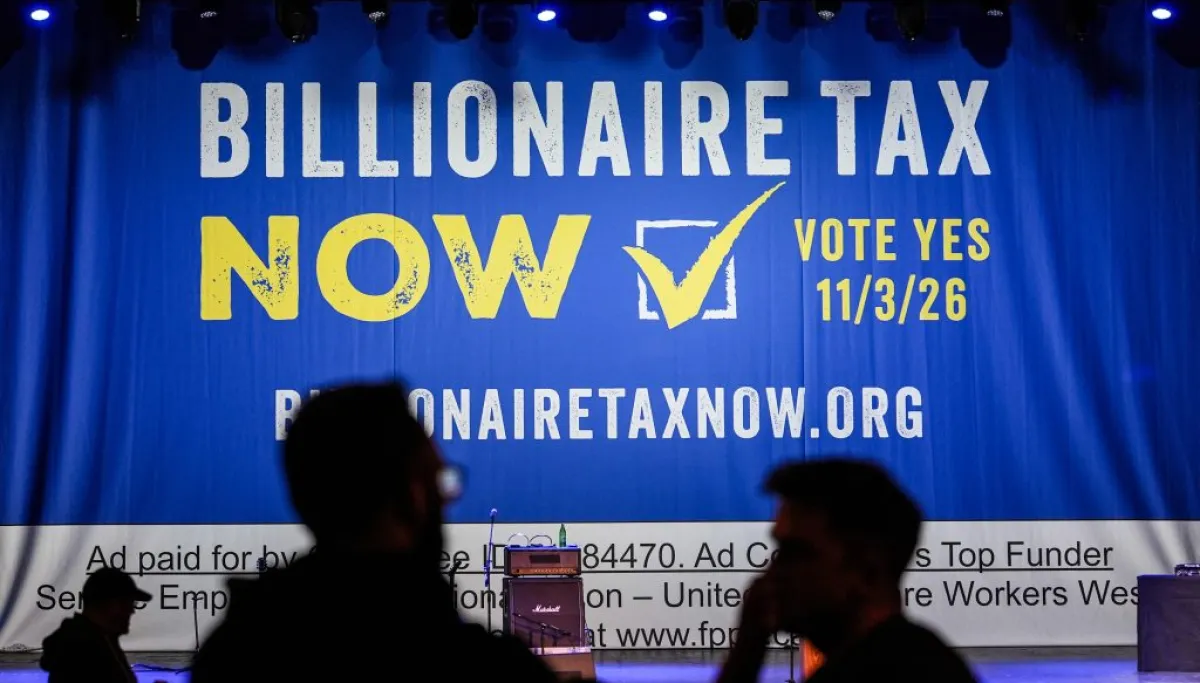

A proposed ballot measure known for the 2026 Billionaire Tax Act would impose a one-time 5% tax on billionaires living in the Golden State, said to be about 200 people. Supporters say that this measure could raise about $100 billion to help fill funding gaps in health care and education. Proponents say that the tax is needed to offset massive cuts in federal spending on Medicaid and food aid recently signed into law by President Trump. As proposed, the tax would apply to the net worth of California billionaires in the 2026 tax year.

Notably, real estate holdings would be exempt. However, most other assets — from private company shares to investment portfolios — would be subject to the 5% levy. The tax could be paid over five years. A small group of billionaires who might have to pay a mere 5% seem unlikely to generate much sympathy from most California taxpayers, or sympathy nationally for that matter. But as with the prior wealth tax proposals, some of the objections are likely to focus on floodgates concerns.