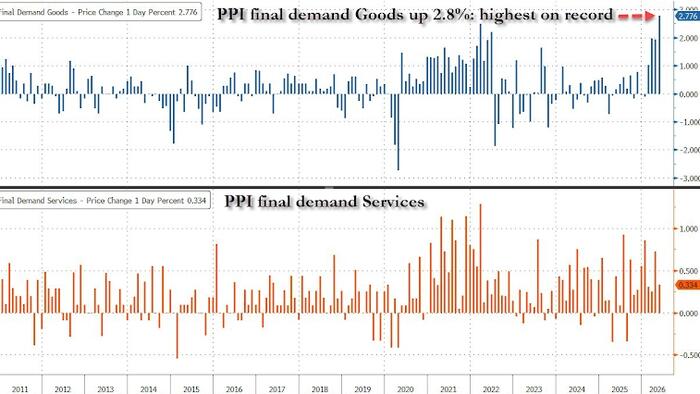

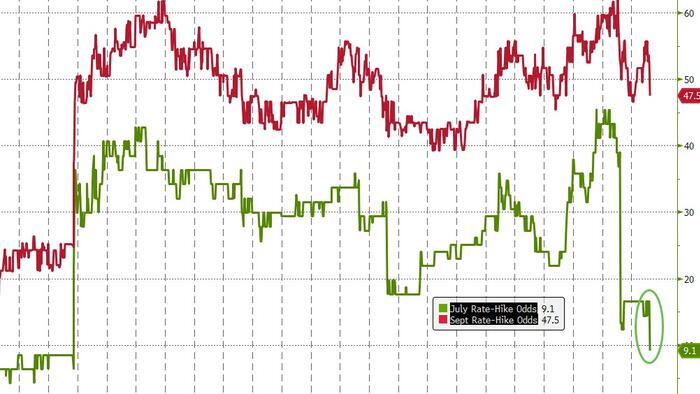

Following yesterday's much cooler than expected, Goldman's Rich Privorotsky notes that today’s PPI print matters more for the core PCE read-through (Fed's favorite inflation indicator), particularly healthcare and financial services.While May's headline PPI print was hot, core was cooler than expected, and June's data release today was expected to show no change in headline producer prices.In fact, like with CPI, headline Producer prices actually saw deflation (-0.3% MoM), equaling the biggest monthly decline since April 2020. The annual pace of producer price gains slowed to 5.5% (well below the 6.2% expected) and May's big jump was revised notably lower also...While Services remain with modest inflation, Goods are in significant deflation now...Core PPI (ex Food and Energy) printed +0.2% MoM, cooler than the +0.3% MoM expected, and May's rise was revised notably lower leaving Core prices up 4.7% YoY (vs +54.1% YoY exp)...Energy was the biggest driver of the headline deflation, but Food and Transportation also saw MoM price declines......and it appears, like with CPI, that Energy's impact on inflation has peaked with prices...Services did pick up from May's deflation...Additionally, according to the data, Memory prices also dipped...Following this print's confirmation of easing inflation angst, July is effectively off the table (technically 9% chance still priced), while September remains live (45%)...Unless core inflation reaccelerates, Goldman's Privorotsky says rate pricing should remain close to current levels.

July Rate-Hike Off The Table After Producer Price Inflation Drops Most Since COVID

...headline Producer Prices actually saw deflation (-0.3% MoM) as Energy's impact on inflation has peaked with prices...

224 words~1 min read