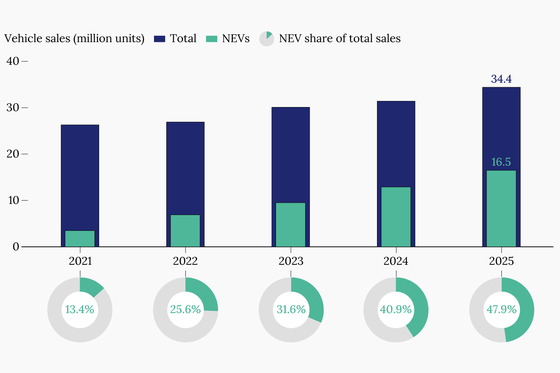

1. In recent years, Chinese automakers, especially those focused on electric vehicles (EVs), have accelerated new model launches to gain a larger market share in the competitive Chinese auto market. The number of new vehicle models reached a record high of 167 in 2025, up from 157 in 2024, and is expected to climb to 173 in 2026, according to CMB International. This surge is primarily attributed to the industry’s rapid shift toward electrification, improvements in component compatibility (e.g. batteries), and the widespread integration of digital and AI technologies, which have streamlined design and testing processes [para. 1][para. 2][para. 3].2. The faster pace has resulted in domestic EV-makers reducing their research and development (R&D) cycles to under two years, a significant drop from the conventional vehicle era, where development typically took at least four years. Growing customer demand for autonomous driving also pushes automakers to keep up with swiftly evolving smart car technologies, such as frequent upgrades of chips by Nvidia and Qualcomm. As a result, domestic brands have achieved a record 69.5% share of China’s passenger car sales in 2025, driven largely by new-energy vehicles (NEVs) [para. 4][para. 5][para. 6].3. However, this rapid development pace has created several challenges. Shorter cycles risk alienating existing customers and eroding brand trust if their purchased models become obsolete quickly. Financially, the swift pace makes it hard for many EV-makers—who already struggle with profitability—to recoup R&D investments, contributing to a decline in industry-wide profit margins. There are also safety and quality concerns, as shorter development periods can lead to more reliability issues compared to traditional vehicles [para. 7][para. 8].4. To stay competitive, many Chinese carmakers are streamlining R&D processes. For example, Zhejiang Geely Holding Group aims to reduce its R&D cycle by 30% over five years. While traditional vehicles emphasized the innovation of unique components, standardized electronic architectures now allow automakers to reuse core systems across models, saving time. Time-saving tactics also include using temporary dies for prototype assembly. Global automakers like Porsche and Toyota are adapting by adopting faster development cycles in China, learning from local competitors [para. 9][para. 12][para. 13][para. 15].5. However, frequent model upgrades can backfire, as seen in August 2024 when Geely’s EV subsidiary Zeekr faced customer backlash after upgrading its 001 model twice in less than a year without a price increase, damaging consumer trust and causing a sales slump. The industry’s average profit margins fell to 4.1% in 2025, the lowest in over a decade, despite a 10% increase in sales to a record 34.4 million vehicles. High components costs and potential product homogeneity risk further eroding profits, leading manufacturers to rely on discounts to boost sales [para. 17][para. 19][para. 20][para. 22].6. Quality assurance is another major concern. According to J.D. Power, NEVs in China experience significantly more reliability issues than conventional vehicles, partly due to the shortened R&D cycles and insufficient durability testing. This has pushed regulators to intervene. Starting January 2027, new rules will require NEVs to complete at least 15,000 kilometers of reliability testing, aiming to balance innovation with safety. Automakers are also taking steps, with Geely now informing customers of upgrades in advance and offering promotions on older models, strategies that have helped restore consumer trust [para. 23][para. 24][para. 25][para. 27][para. 28].7. Looking ahead, automakers are expected to adopt more diverse upgrade strategies, possibly reserving frequent updates for high-end models where higher profit margins can offset R&D costs. This shift reflects a broader industry recognition of the need to balance rapid innovation with financial health, customer loyalty, and product safety [para. 29][para. 30].AI generated, for reference only

In Depth: Chinese Automakers’ Need for Speed Comes With a Price

Launching new models at a record pace has helped domestic carmakers dominate the world’s largest auto market, but the strategy is threatening their financial health, eroding customer loyalty and raising quality concerns

594 words~3 min read