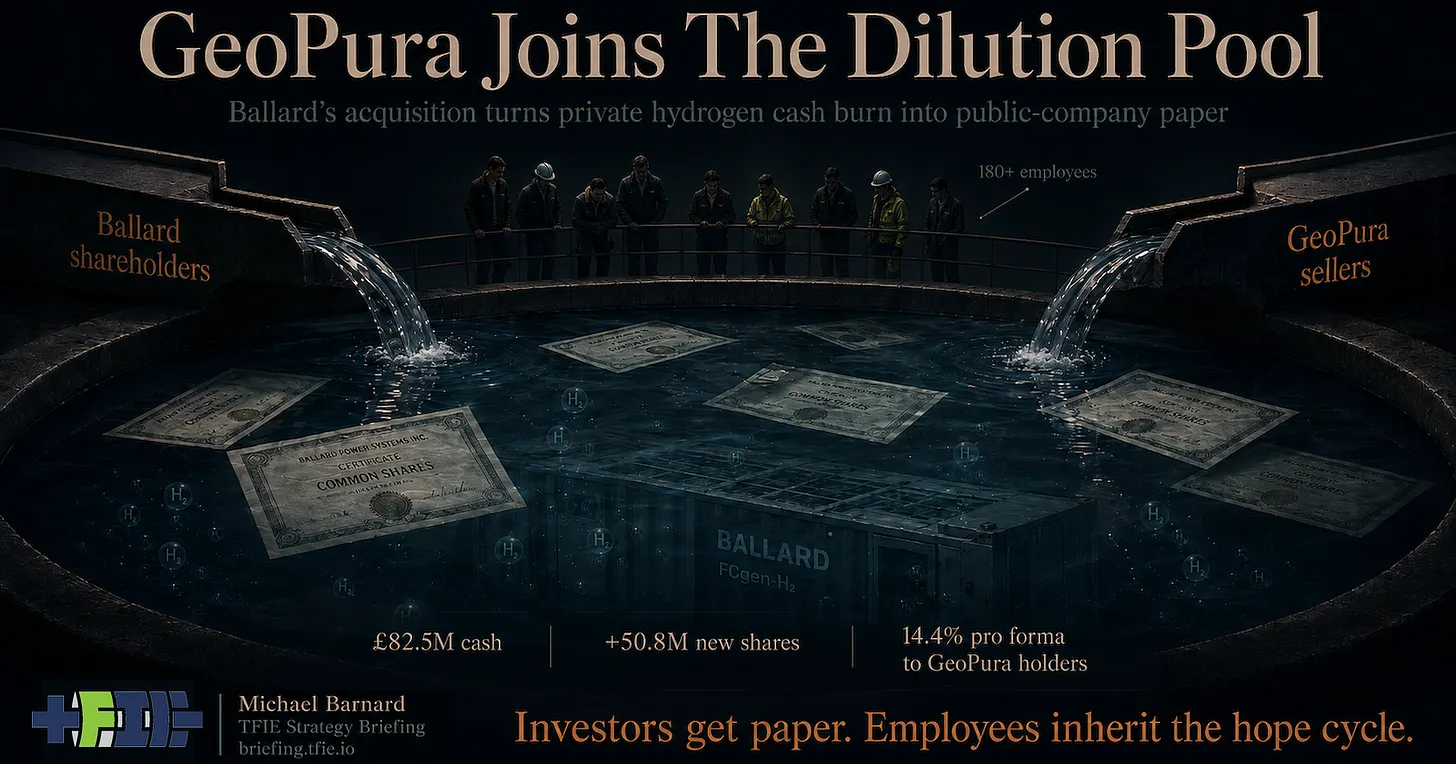

GeoPura’s sellers receive only £82.5 million in cash and mostly Ballard shares, while employees inherit the execution risk of the next hydrogen dilution cycle.

Support CleanTechnica's work through a Substack subscription or on Stripe.

Perpetual loss-making hydrogen fuel cell firm Ballard Power is paying £275 million for GeoPura, but only £82.5 million is cash. Most of the price is 50.8 million newly issued and dilutive Ballard shares, leaving GeoPura’s investors with about 14.4% of the combined company and subjecting much of their consideration to post-closing lock-ups. That looks less like a strong strategic buyer acquiring a profitable growth platform than a capital-hungry private hydrogen company accepting the least-bad exit available.

Ballard’s acquisition announcement presents the deal as a transformation into an integrated hydrogen ecosystem provider. The company will move beyond fuel-cell power modules into hydrogen production, storage, distribution, refuelling, logistics and deployed power services. That makes the investor presentation broader and more tangible, but it does not change the denominator: most of the purchase price is dilutive Ballard paper with its history of terrible stock performance. The share price is already down substantially from the announcement of the deal.