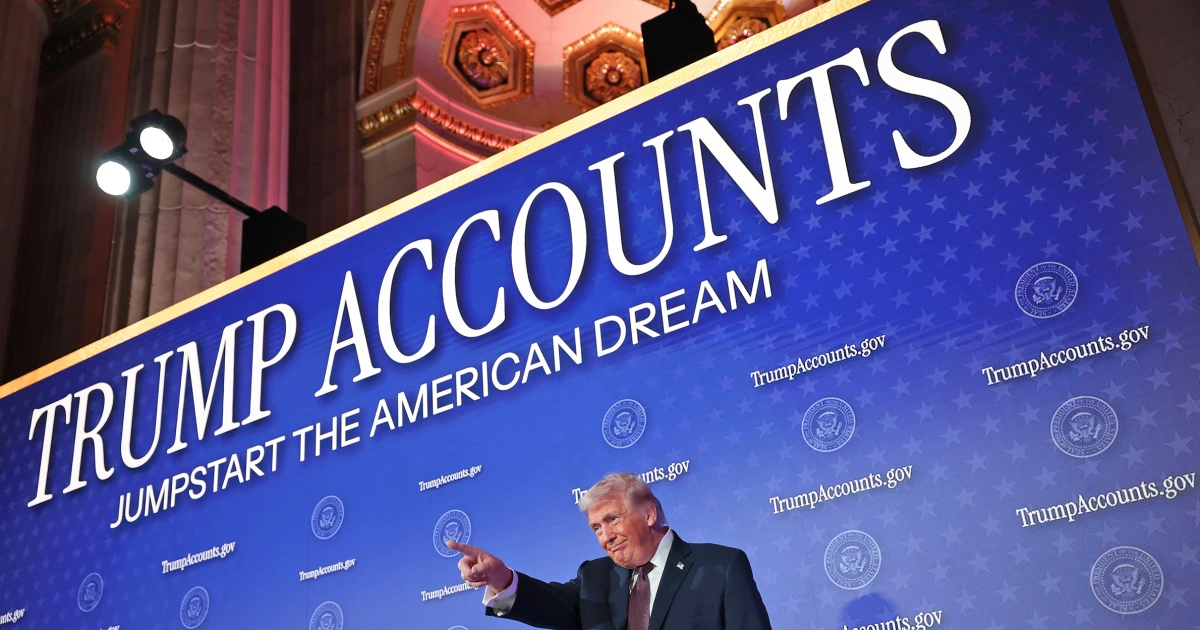

If you’ve opened the Trump Accounts app, the pitch for investing is hard to resist.

Enter a $250-a-year contribution, and the app shows the user would have $19,000 by age 18 or a whopping $878,000 by age 55. Bump it up to the $5,000 annual max, and the numbers jump to $271,000 and $13 million, respectively.

That eye-popping figure comes straight from the government’s own projection on TrumpAccounts.gov, but it rests on an assumption of the S&P 500’s historical annual return of more than 10%, sustained without interruption for 55 years. While that 10% has historically been the case, Morningstar provided CNBC with data showing U.S. stock market returns could be lower over the next decade, closer to an average return of 6.3% per year.

That being said, financial planners want parents to see the full picture before they start dreaming of what feels close to a trust fund, or at the very least, a nice nest egg, for their kids.

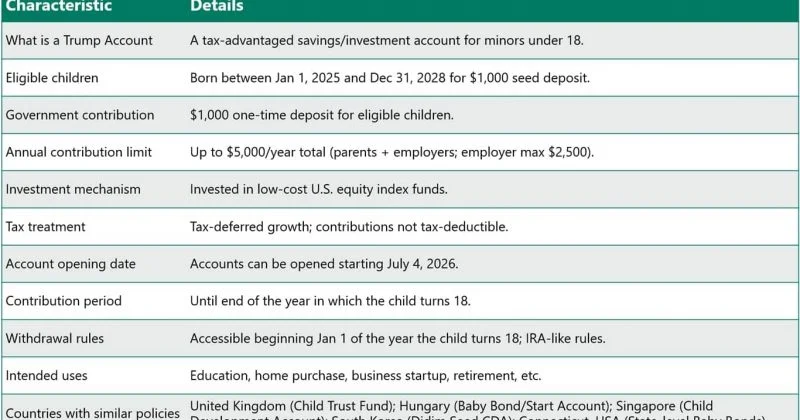

Trump Accounts, the tax-advantaged investment accounts for children created under President Donald Trump’s tax law that officially launched July 4, have drawn attention for a headline promise: that a child could retire a millionaire off contributions their family barely notices. The accounts function like a traditional IRA, but during the “growth period” that runs from birth through the year before a child turns 18, special rules apply.