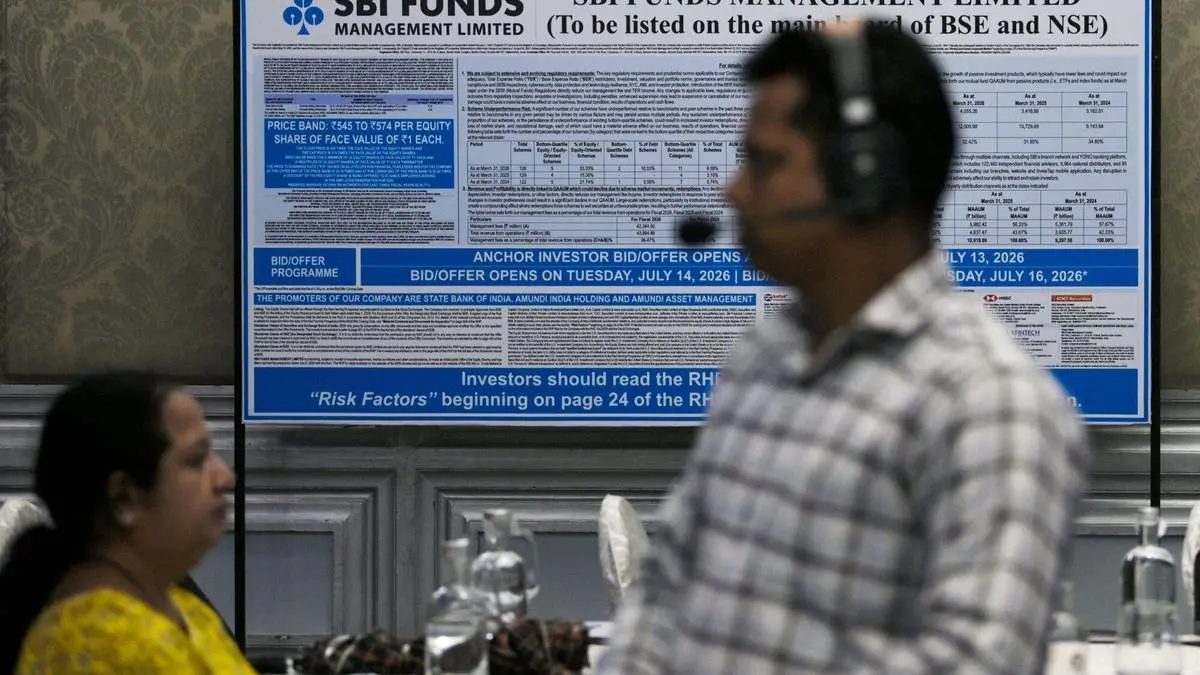

Incorporated in 1992, SBI Funds Management (SBIFM) is the oldest and the largest asset manager in India in terms of Quarterly Average Assets Under Management (QAAUM) and market share. It is a joint venture between State Bank of India (India’s largest bank) and Paris-headquartered Amundi Asset Management (largest European asset manager). The company serves a large unique investor base of 1.8 crore.The company is the seventh AMC to tap the IPO market. As per SBI’s latest July 11 update, promoter shareholders SBI and Amundi plan to raise about ₹9,813 crore by selling up to 17.095 crore shares at the upper end of the ₹545–574 price band. The IPO is entirely an offer for sale, so the company will receive no proceeds. In a pre-IPO placement, SBI has already raised ₹1,655 crore by selling about 2.88 crore shares to 30 investors at ₹574 apiece. The IPO opens on July 14 and closes on July 16. After the issue, the promoters will hold 88.2 per cent, with SBI alone retaining 55.6 per cent. The implied m-cap is about ₹1.17 lakh crore, which should place it after ICICI Pru AMC and HDFC AMC. At the upper end of the price band, SBI Funds is valued at FY26 P/E multiple of around 38x. This is not expensive and is below like-sized peers such as ICICI Pru AMC (47x), HDFC AMC (39x) and Nippon India (48x) on a trailing twelve-month earnings, per Bloomberg.Given the still low penetration (India AUM as per cent of GDP is 18.5 per cent vs 126 per cent for US), the mutual fund industry in India expected to grow at a robust pace, helped by rising financialisation of savings. Thus, the runway for growth is long for SBI Funds. As a manufacturer of investments products, it operates a highly scalable, cash-generative business model (we explain later in the article).Investors can subscribe to the IPO from a five-year or longer perspective. Massive scale, strong position in the AMC business as the leader, healthy operational performance and a seasoned fund management team are positives for the company.Note that businesses such as AMCs are dependent on market movements. If prolonged bear markets make investors wary with parking surpluses in mutual funds or investors choose to exit during heavy volatility, there may be challenges and AMC stocks may correct. Since management fees are based on AUM, cyclical declines in markets can impact revenue and profits. Hence a long-term perspective is required. Any overall reduction of mutual fund management fees by regulator SEBI in the future may also affect earnings.BusinessSBI Funds Management managed a total of 128 schemes as of March 31, 2026, including one Specialised Investment Fund (SIF) strategy. In the MF side, there were 49 debt schemes, 37 ETFs and index funds, 35 equity and equity-oriented schemes, four domestic Fund of Funds (FoF), two liquid and overnight Schemes etc.In Alternative Investment Funds (AIFs) space, the company manages SBIFM Special Situations Fund-1, SBI Optimal Equity Fund, SBI Emergent India Fund. In the Portfolio Management Services (PMS), it offers discretionary and non-discretionary management tailored to different client bases. It manages portfolios for global investors who are seeking exposure to Indian equity markets through offshore India-focussed funds and PMS structures.The company has 1,500+ employees, with 71 in the fund management and investment team. Attrition rate in this bucket is stable at 10-11 per cent for the last three years, and no senior fund manager has left in the last few years.SBI Funds’ offerings are sold to investors through a pan-India distribution network comprising of 1.32 lakh institutional and individual MF distributors. This includes independent financial advisers, national distributors and 95 banks (including SBI), proprietary branch network as well as direct digital channels (InvesTap and website). It maintains presence in 98.2 per cent of India’s pincodes.ModelAs an asset manager, the core economic engine is management fees. This is calculated as a percentage of the ₹29.46-lakh crore assets (as on March 2026) it manages across offerings. Mutual funds (MFs) - ₹12.5 lakh crore and PMS & Advisory - ₹16.89 lakh crore, mostly derived from EPFO, are the main product lines. AIFs at ₹0.07 lakh crore is minute but has good potential. AIFs command relatively higher yields compared to other traditional asset classes. EPFO money operates on compressed fee structures (not great operating revenue yields). Revenue from PMS clients and advisory services stood at a mere ₹154 crore or 3.5 per cent of revenue from operations. Instead, it acts as a stable, scale-driven anchor, while retail MFs deliver the actual high-margin yields. Thus, at a company level, FY26 operating revenue yield for SBI Funds was 35 basis points (bps) versus 44 bps for HDFC AMC and 52 bps for ICICI Pru AMC, who are like-sized peers. Equity, equity-oriented and equity-hybrid schemes (active) account for three-fourth of total management fee income from SBI MFs. Overall in FY26, their management fees drove 96.5 per cent of the company’s operating revenue (₹4,389 crore).Revenue yield depends heavily on the asset mix; actively-managed equity funds command higher fee margins than debt or rapidly-growing passive ETFs. At an asset class level, about 43 per cent of MF assets come from active equities and their hybrids, 14 per cent from active debt and their hybrids, 32 per cent from ETFs and index funds and the rest from liquid, overnight, arbitrage, SIFs and FoFs.What impact does MF SIP play? SIP inflows provide highly predictable, recurring cash flows. This drastically reduces the AMC’s reliance on volatile lump-sum investments, and secures stable management fee income. It holds a market leadership position (11.4 per cent share by inflows) with 1.62-crore live SIP accounts. Nearly 98 per cent have been active for over 37 months, showing high investor stickiness and long-term revenue visibility.Utilising an asset-light framework, SBI Funds’ primary expenses are relatively fixed in the short to medium term. Key costs include employee benefits (9 per cent of total income in FY26). Other expenses includes IT costs, brand royalty, CSR, marketing, etc. In this pie, there is royalty (1.6 per cent of FY26 PAT) paid to parent SBI for brand licencing. This number optically appears higher than trademark licencing fee of 1 per cent per annum of ICICI Pru AMC’s standalone PAT paid to ICICI Bank, as per that AMC’s RHP.SBI Funds also pays trail commissions to over 1.3 lakh distributors, though these are embedded within regular plan expense ratios.Profit is generated by deducting these operational costs from fee revenue. Cost as percentage of assets of SBI Funds at 8 bps is the lowest among listed AMCs (10-25 bps). Thus, the business thrives on strong operating leverage. As AUM scales, fee revenue outpaces the fixed cost base. This structural advantage enabled the company to deliver a robust 43 per cent Return on Equity (RoE) and a ₹3,067-crore FY26 net profit. This RoE sits right between HDFC AMC (32.9 per cent) and ICICI Pru AMC (85.8 per cent).FinancialsNext, let us find out how the business model and scale has translated into growth.Assets under management (AUM) growth is the top-line driver. The company’s ₹29.46-lakh crore AUM in FY26 grew at a CAGR of 14.2 per cent between FY24 and FY26. More importantly, the core MF assets grew at a 17 per cent CAGR over the same period. The highest-yielding segment (equity products) outpaced overall growth with an impressive 22 per cent CAGR.Because of the business’s fixed-cost nature, net profit (PAT) grew at a decent 22 per cent CAGR over the FY24-26 period, while total revenue increased at 20.5 per cent CAGR. This operating leverage allowed the PAT margin to expand from 60.50 per cent in FY24 to 61.65 per cent in FY26. In comparison, as per RHP, PAT margins for HDFC AMC (61.8 per cent) and ICICI Pru AMC (55 per cent) were in the same range.The asset-light model adopted by AMCs is highly cash-generative. In FY26, SBI Funds generated ₹2,487 crore in operating cash flows, which translates to a cash conversion rate of 81.1 per cent. This figure has improved from 69.4 per cent in FY24 and 78.3 per cent in FY25.The AMC business requires minimal capital expenditure and has no borrowings.PlansSince the IPO is entirely an Offer for Sale (OFS), SBI Funds is not raising fresh capital to fund operations. However, the company has outlined several “growth engines” and strategic initiatives designed to power its next phase of growth.To accelerate retail customer addition, the company is intensifying its focus on Beyond Top 30 (B-30) cities. This includes deploying dedicated MF specialists in high-potential, underserved geographies, running grassroots investor education campaigns and aggressively expanding the “Jan Nivesh SIP” initiative (low-ticket SIP starting at ₹250) through targeted campaigns to capture first-time MF investors.The company plans to significantly upgrade its digital engagement and distributor capabilities to increase wallet share and the number of products per customer. They are deploying predictive analytics specifically to identify investors who are at risk of discontinuing their SIPs, allowing for personalised interventions to improve long-term persistency rates.The rollout of AI-powered chatbots, goal-tracking dashboards and integrated financial planning tools aims to offer targeted product recommendations (such as retirement or education solutions) based on specific investor risk profiles. Further deepening the integration with SBI’s massive YONO digital banking app is on the cards to drive onboarding. It expects universal KYC to potentially double SBI MF’s SIP book.While active MFs are its bread and butter, SBI Funds is expanding its product suite to capture shifting institutional and HNI demand. It aims to broaden the passive portfolio with new thematic, sectoral and “smart beta” equity index funds, alongside fixed-income ETFs (like target maturity and G-Secs) and international/commodity ETFs. It is also expanding aggressively into Category II and Category III AIFs.Leveraging its dual parentage with Europe’s Amundi, the company is building a structural bridge for international capital. They also plan to expand co-managed fund offerings by tapping into Amundi’s global distribution network.RisksApart from market movements and regulatory fee reductions, investors should monitor scheme concentration and fund performance. While not different from peers, SBI Funds’ top 5/10 schemes account for a large chunk of assets. Consequently, underperformance or heavy redemptions from a few large schemes could have a disproportionate impact on revenue and profit.The growing popularity of passive funds is another risk to revenue yields. Passive products already represent nearly one-third of SBI Funds’ MF assets but earn lower fees than actively-managed products. Operational errors, cyber incidents, regulatory observations or the departure of key fund management personnel could hurt investor confidence and lead to outflows.Published on July 11, 2026

Why You Can Subscribe to SBI Funds Management IPO

Explore why investing in SBI Funds Management's IPO is promising, highlighting its market leadership, growth potential, and strong profitability.

1,743 words~8 min read