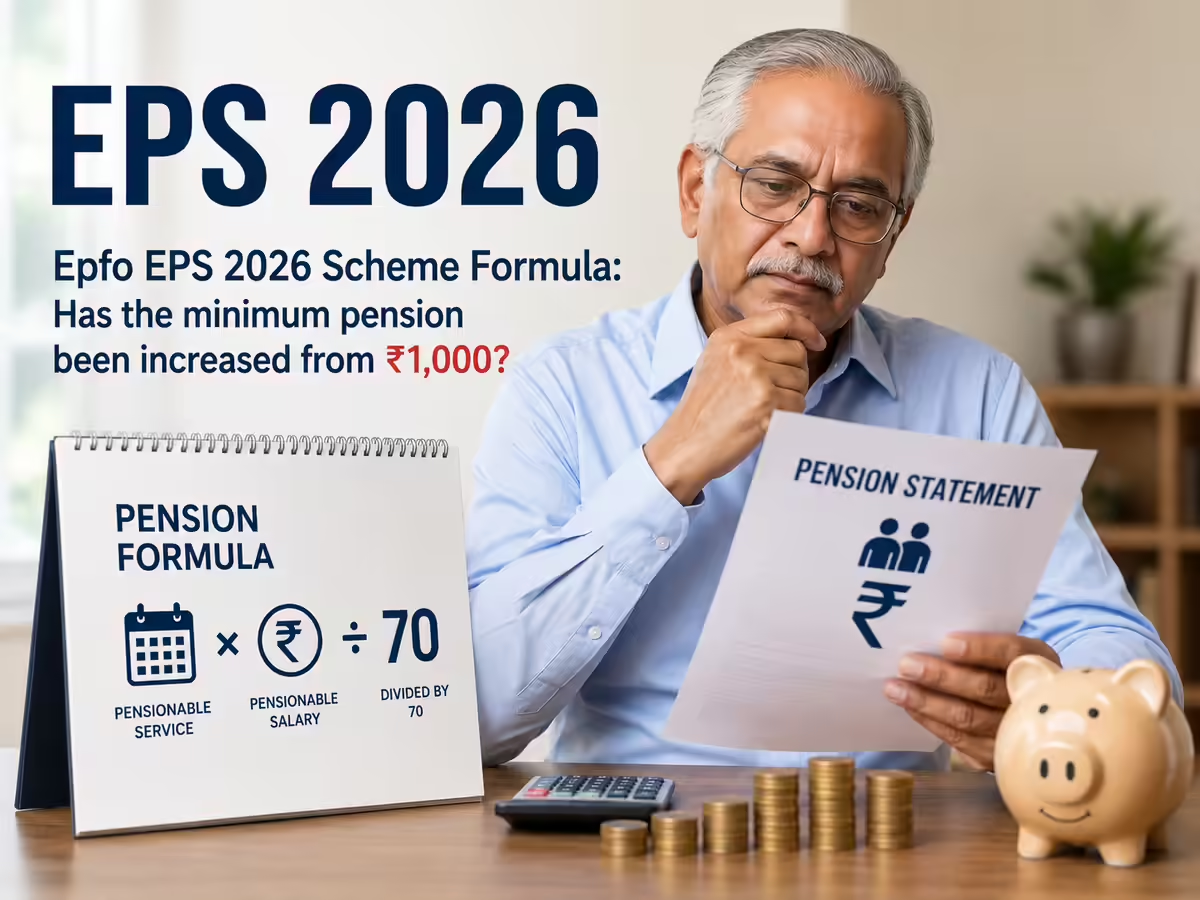

The Employees' Pension Scheme (EPS), 2026, has incorporated numerous significant changes aimed at improving the pension system for EPF members. The new EPS scheme has been notified under the Code on Social Security, 2020.The new EPS scheme has maintained many provisions of the previous EPS scheme while introducing stringent withdrawal benefit requirements, faster claim settlement deadlines, statutory recognition for the higher pension option, and better alignment with the EPF system, 2026.What is the EPS and who is eligible to draw a pension under it?The EPS stands for the Employees' Pension Scheme, a social security programme managed by the Employees' Provident Fund Organisation (EPFO). The EPS guarantees a lifelong monthly pension to eligible organised-sector employees in India.Who is covered under the EPS-95 scheme?Employees' Pension Scheme (EPS), 1995, covers employees working in factories and establishments that are covered under the EPF scheme. It also includes members of the erstwhile Family Pension Scheme, 1971, as well as employees who became members between April 1, 1993, and November 15, 1995. EPS membership generally continues until the member attains the age of 58 years.Here is a look at the key changes introduced under the EPS 2026 scheme as analysed by Grant Thornton Bharat.Key changes introduced under EPS Scheme, 2026Revised withdrawal benefit provisionsOne of the key changes under the EPS 2026 scheme relates to withdrawal benefits. While EPS 1995 permitted eligible members to claim withdrawal benefits upon exit from employment, the EPS 2026 scheme restricts such withdrawals until the completion of a 36-month waiting period from the last contribution due date or the attainment of superannuation age, whichever is earlier, thereby promoting long-term pension retention.Continuity of existing membershipThe transition to EPS 2026 does not require fresh enrolment for existing members. Para 8 of EPS 2026 specifically provides for the continuation of all eligible members already covered under the earlier scheme, ensuring a seamless transition without the disruption of pension benefits.Statutory recognition of higher pension optionPara 4(2) of EPS 2026 expressly incorporates the higher pension option within the scheme itself, providing greater statutory clarity for eligible members who have exercised the prescribed option.Introduction of defined claim settlement timelinesPara 17 of EPS 2026 mandates that pension claims be settled within 20 days. Delays in settlement may result in accountability measures and interest implications, thereby enhancing administrative efficiency and claimant protection.Alignment of damages frameworkUnder EPS 2026, the damages framework has been aligned with the provisions of the EPF Scheme, 2026, promoting consistency across the social security framework.Pensionable salary based on extended wage averagingEPS 2026 retains the existing pensionable salary determination mechanism and provides that pensionable salary shall be calculated based on the average monthly wages drawn during the last 60 months of eligible service immediately preceding exit from the Scheme.

EPS Scheme 2026: Higher pension, 20-day claim settlement, new withdrawal rules; top changes explained - The Economic Times

The Employees' Pension Scheme, 2026, introduces significant changes for EPF members. Withdrawal benefits now require a 36-month waiting period after exit. Existing members will seamlessly continue their coverage under the new scheme.

451 words~2 min read