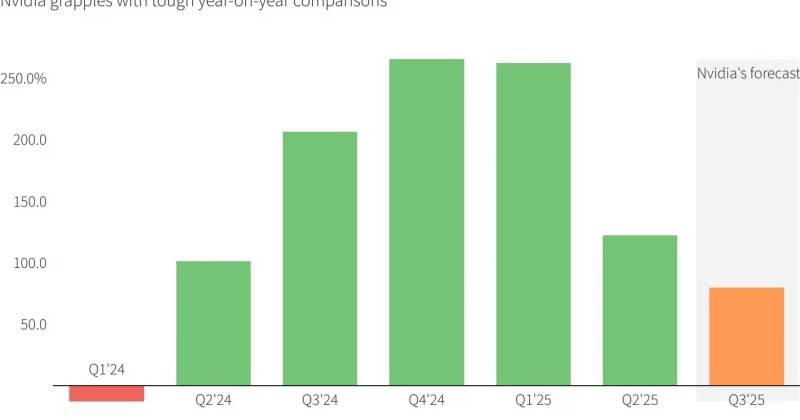

Long the leading light of the industry, Nvidia has had a bad couple of months. Bloomberg has the ugly details, but the upshot is that the company’s stock price has fallen 15% since its peak in May, even as projected revenue continues to grow. Compared with expected earnings, the company is now cheaper than the S&P average; investors are paying less per dollar of Nvidia’s projected profit than they do for the typical large American company.

Money is still flooding into AI infrastructure stocks, but it’s mostly going into memory companies. Over the same period, Micron — one of the world’s largest makers of DRAM, the standard type of memory chip found in computers and servers — has nearly tripled in value, establishing memory as the new bottleneck for data centers and the hot new AI trade. The basic reason is simple: the GPU shortage that looked so alarming last year has eased off a bit. At the same time, data centers need all the memory money can buy.

For anyone who appreciates Nvidia’s technological accomplishments, this can feel a bit deflating. There’s a lot of genuinely impressive technology behind Nvidia’s rise, both in developing CUDA, its widely adopted programming platform that made Nvidia GPUs the default engine for AI research, and in pushing the pace of GPU development to a speed few thought possible. Nvidia’s success is the kind of thing you can write whole books about, and the GPUs themselves are among the most complex devices ever produced, right at the bleeding edge of human capability.