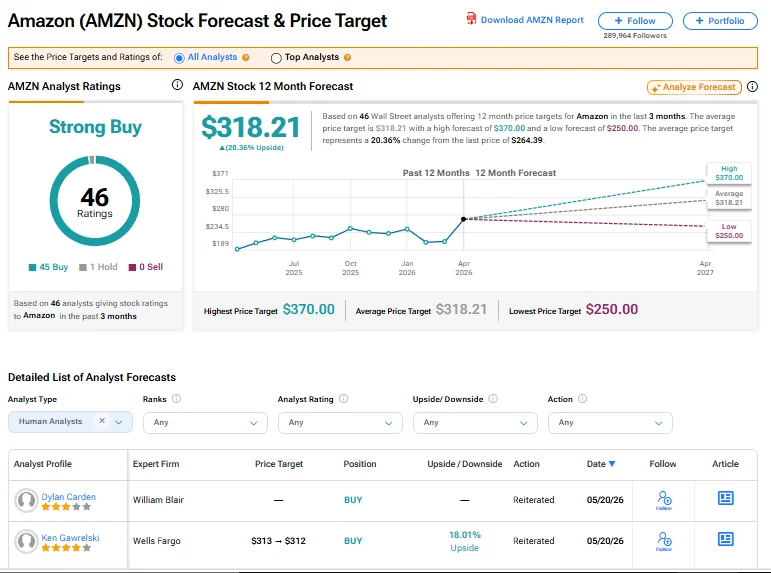

The firm said it expects Amazon to report second-quarter results during the week of July 27, with broad-based strength led by accelerating growth in Amazon Web Services (AWS).AWS Growth And Earnings ExpectationsBNP Paribas analyst Nick Jones expects investors to focus on four key areas: AWS growth and capital spending trends amid data center component inflation, the impact of Prime Day on retail sales, advertising growth and operating income margins as the company continues investing heavily in AI infrastructure.The brokerage expects AWS revenue growth of 33% to 35% in the second quarter, above the consensus estimate of about 31%. It also projects operating income of about $25 billion, compared with the Street consensus of $23.6 billion.Third-Quarter Outlook And AI SpendingFor the third quarter, BNP Paribas believes investors are looking for Amazon to guide toward the high end of its outlook, with revenue of about $207 billion and operating income of $26 billion. Those figures are above current consensus estimates of $204 billion and $25 billion, respectively.The firm added that investors are also likely to expect higher full-year 2026 capital expenditure guidance as rising data center component costs increase AI infrastructure spending.Retail Trends And Financial EstimatesBNP Paribas said data indicate Amazon’s Online Stores and Third-Party Seller Services businesses remain broadly in line with Wall Street expectations, implying about 14% year-over-year revenue growth. The firm left its financial estimates unchanged ahead of the earnings release.Valuation And Analyst ViewDespite ongoing concerns about the return on investment from data center spending, BNP Paribas said it expects continued AWS acceleration and solid execution across Amazon’s businesses.The firm also said the stock’s current valuation remains an attractive entry point, with shares trading broadly in line with their six-month average forward enterprise value-to-EBITDA multiple.Earnings And Analyst OutlookAmazon is expected to report second-quarter earnings on or around July 30.Wall Street expects earnings of $1.82 per share, up from $1.68 a year earlier. Revenue is projected to increase to $196.02 billion from $167.70 billion.The stock carries a consensus Buy rating with an average analyst price forecast of $320.55. Recent analyst actions include:

What's Going on With Amazon Stock Thursday? - Amazon.com (NASDAQ:AMZN)

Amazon heads into Q2 earnings with an Outperform rating and $345 target from BNP Paribas. Read the technical trends for AMZN.

384 words~2 min read