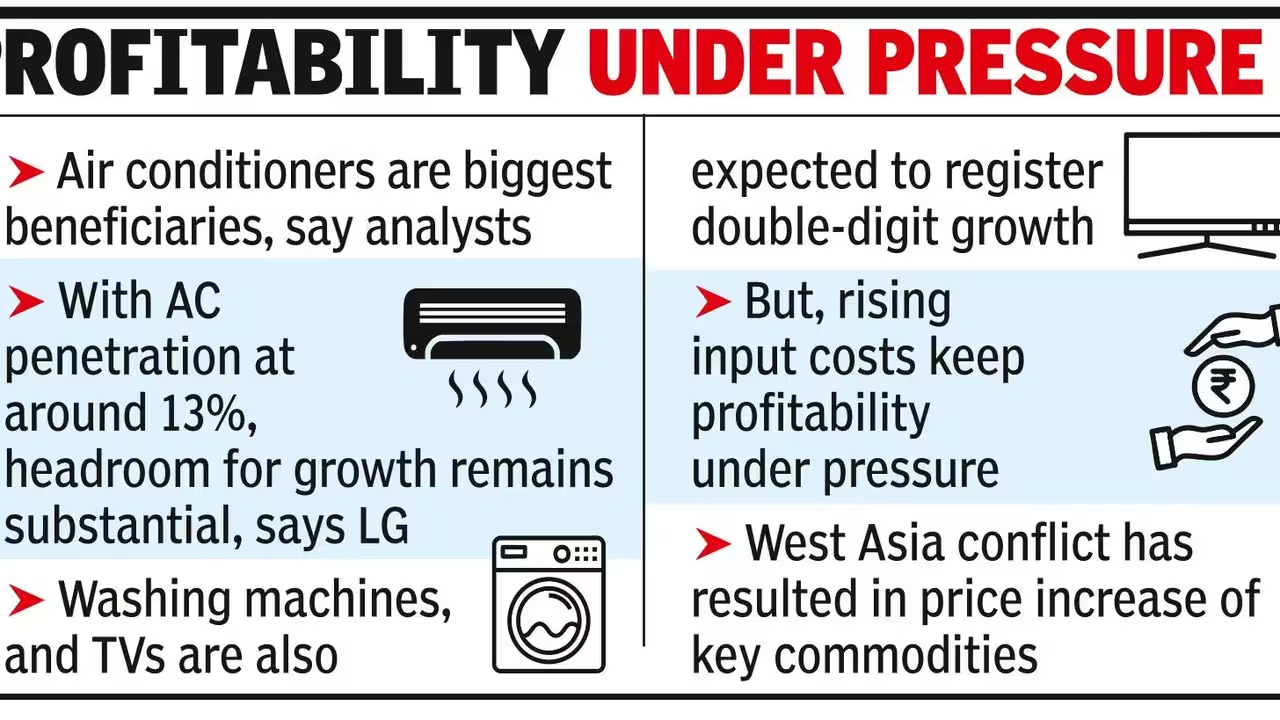

Corporate India is expected to clock its fastest revenue expansion in two years in the opening quarter of this fiscal, navigating a barrage of exogenous disruptions that tested businesses across sectors.Supply-chain disarrays triggered by the West Asia conflict amplified uncertainty around crude oil prices, raw material and packaging costs, energy expenses, freight rates and global trade flows.Adding to the pressure, the rupee weakened, pushing up the cost of imported inputs, while demand remained uneven across consumption-led, export-oriented and investment-driven industries.Yet India Inc seems to have pressed ahead.Our analysis of more than 400 companies—together accounting for nearly half of India's listed market capitalisation—suggests revenue likely grew 11-11.5% in the first quarter, significantly faster than the average growth in the past eight quarters.Also read | India flags inconsistencies in US forced labour probe, seeks resolution via trade talksThe nature of that growth, however, is beginning to shift.In the past two fiscals, revenue expansion was driven largely by volume growth. That momentum is increasingly becoming price-driven, particularly in commodity-linked industries.Domestic economic activity continued to be a key source of support. Sectors such as automobiles, white goods and fast-moving consumer goods (FMCG) continued to benefit from the demand stimulus generated by the rationalisation of goods and services tax, helping sustain healthy volume growth despite rising prices.Automobile demand remained especially buoyant, with two-wheeler and passenger vehicle volumes likely expanding 14% and 25%, respectively, marking a third consecutive quarter of robust traction.The momentum was visible elsewhere as well. Backed by sustained construction activity, cement and steel volumes are estimated to have grown 4-5% during the quarter. Power demand remained robust, likely rising ~7%, supported by above-average temperatures and strong industrial and commercial consumption.India's export engine also fired on multiple cylinders. Merchandise and services exports during April and May are estimated at about $163 billion, up nearly 15%, powered by electronics, higher-value petroleum products and information technology services.Also read | India's richer middle class is living a more dollar-linked life while earning in rupeesTo be sure, not every indicator flashed green. Output growth across India's eight core infrastructure industries remained subdued at 1-2%, reflecting supply challenges in crude oil, gas and fertiliser production.Yet the broader economic picture remained encouraging. Central government capital expenditure, led by railways, increased 14% during April and May, underscoring the continued strength of infrastructure development and construction activity.One of the defining features of the first quarter is the growing role of pricing in shaping revenue performance.Take airlines, for instance. Despite a ~5% decline in passenger traffic, airline service companies are likely to report revenue growth of 13-14%, driven by a sharp increase in fares and realisations.Similar dynamics were visible in metals. Steel prices increased about 5% during the quarter, supported by resilient demand, higher input costs and safeguard duties that curbed imports from China. Aluminium producers also benefited as Middle East supply disruptions created market deficits and pushed prices up approximately 27%.Revenue growth may have remained broadly healthy, but profitability told a more nuanced story.The pain point was rising input costs. Wholesale inflation accelerated to ~10% in May, fuelled by higher energy, fuel and manufacturing costs. Across industries, companies grappled with rising transportation expenses, elevated feedstock costs and pricier imports resulting from both higher energy prices and rupee depreciation.As a result, we expect overall corporate profitability to contract 75-100 basis points on-year during the quarter, as companies were only able to pass through part of the cost increase to customers.While revenue growth appears broad-based, profitability has shades of subtext, with elevated energy and input costs weighing on earnings across several sectors.Margin pressure was strongest in sectors exposed to crude oil and gas, including airlines, chemicals, pharmaceuticals and cement. Consumer sectors proved relatively resilient, though higher packaging and food costs likely compressed margins 80–100 basis points despite selective price increases.Looking ahead, three variables will shape the trajectory of corporate performance.The first is the sustainability of lower crude oil prices and the speed at which global supply chains normalise. The second is the progress of the southwest monsoon, with rainfall shortfalls and potential El Niño-related risks carrying implications for rural demand and food inflation. The third is the durability of India's investment cycle, which is increasingly becoming the engine powering corporate growth.Ultimately, the first quarter's primary takeaway may not be the temporary squeeze on margins but in the resilience of the forces underpinning growth.A strong domestic demand base, sustained public investments, improving private investments, expanding manufacturing capacity, deeper integration with global supply chains, strengthening exports and a rapidly growing digital economy continue to reinforce India's growth story.Proactivity in reforms and continuous institutional facilitations to mainstream and scale the millions of small and micro enterprises would be vital for the next legs of growth.Priti Arora is President & Business Head - Crisil Intelligence(Disclaimer: The opinions expressed in this column are that of the writer. The facts and opinions expressed here do not reflect the views of www.economictimes.com.)

Rising with pricing: Corporate revenue growth likely held firm in the first quarter, riding out the tempest

Corporate India's revenue reached a two-year peak in Q1, propelled by significant price hikes. The domestic market drove growth in key sectors such as automobiles and FMCG, accompanied by robust volume increases. Strong export performance, especially in electronics and IT services, further boosted the economy. Yet, soaring input costs greatly impacted corporate profit margins this quarter.

811 words~4 min read