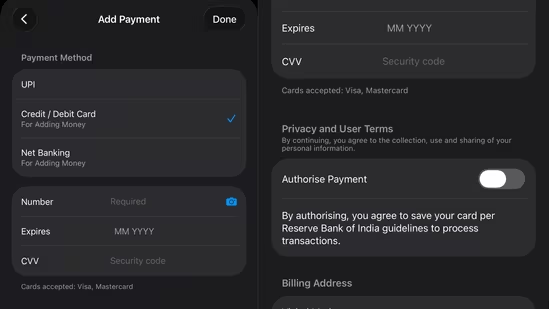

Apple is reportedly restoring direct credit and debit card payments for App Store purchases, iCloud+ and Apple subscriptions in India after roughly four years of workarounds, pre-paid balances and UPI prompts. Eligible Visa and Mastercard cards are said to be appearing for a small set of users first, with a broader rollout expected over the coming months. That is good news for anybody who has tried to renew iCloud storage at the wrong moment and found themselves loading money into an Apple Account like it was 2008.But this is not Apple Pay. It is not a Wallet launch. It does not mean iPhone users can suddenly tap a terminal at Starbucks, the Delhi Metro or a petrol station with Face ID. It is Apple rebuilding a piece of billing infrastructure that India’s payment rules broke, then using that work to prepare for a much harder job: convincing Indian banks, card networks and regulators that Apple Pay deserves a place in a country already wired around UPI.The immediate result is simple. Indian Apple users may once again be able to add an eligible debit or credit card directly to their Apple Account and use it for App Store purchases, iCloud+, Apple Music and similar services. The larger result is more complicated. Apple has spent years learning that India does not bend its payments rules because a company in Cupertino finds the checkout flow untidy.India made Apple adapt. And Apple, eventually, did.Key takeawaysApple is reportedly restoring direct Visa and Mastercard payments for App Store, iCloud+ and Apple subscription purchases in India through a phased rollout. Apple has not issued a formal public launch announcement.The return follows Apple’s reported compliance with RBI tokenisation and payment-data localisation requirements. RBI rules prevent merchants and token requestors from holding full card details in the old way.Apple stopped card billing after RBI’s recurring-payment and tokenisation rules disrupted its previous stored-card system. The process began with a September 2021 warning and became a consumer problem in 2022.Apple Pay remains unavailable in India. Apple’s official list of countries and regions supporting Apple Pay still does not include India.The reported Apple Pay delay is now less about technology than commercial negotiations with major banks, data handling and the need for a payment proposition that makes sense in a UPI-first market.What Apple has actually changed in IndiaApple is reportedly bringing back the option to use certain cards as a direct Apple Account payment method. This had been disabled since September 2022.Moneycontrol reported that Apple is testing direct card payments with selected users, beginning with Visa and Mastercard, while RuPay and American Express support is reportedly still being prepared. The report says the wider rollout could take several months. TechCrunch separately reported that the phased change lets eligible Indian users add Visa and Mastercard credit or debit cards to their Apple Account for subscriptions such as iCloud+ and Apple Music, as well as App Store purchases.That sounds faintly ridiculous because it is such a normal thing to be able to do. Everywhere else, “add card, pay for storage” is not news. In India, it became a small domestic ritual of payment friction.You wanted an app? Use UPI.You wanted more iCloud storage? Set up UPI Autopay, if your bank supported it.You wanted a subscription but did not want a recurring UPI mandate? Add money to an Apple Account balance through UPI, net banking or a card, then let Apple deduct from that stored balance.The workaround functioned. It was also clumsy. Particularly for users with corporate cards, international cards, family accounts, prepaid balances, recurring subscriptions or a perfectly good credit card that had become oddly unwelcome inside the most valuable consumer electronics platform on the planet.Apple’s own India billing page, published on 23 June, still says that new subscriptions can be paid through UPI Autopay or Apple Account balance, while other purchases can use UPI or account balance. The same page says users can use accepted cards to add funds to their Apple Account balance. Yet Apple’s broader India payment-method page now lists Visa and Mastercard alongside UPI, net banking and Apple Account balance. That mismatch is a clue: the public support material is in transition, and the consumer rollout is not yet uniform.Why Apple removed card payments in the first placeThe answer has been flattened too often into one phrase: “RBI rules”.That is technically true and editorially useless.There were several overlapping rules, deadlines and payment requirements. Apple’s old card-billing arrangement ran into a regulatory environment designed to make recurring payments safer, card details less portable and payment data more visible to Indian authorities.The first warning arrived in September 2021. Apple told developers that RBI requirements affecting recurring card payments would begin in October that year. The rules required banks, financial institutions and payment gateways to obtain user approval through transaction notifications, e-mandates and an Additional Factor of Authentication before certain recurring payments could be completed. Apple warned developers that card-based auto-renewals that did not meet those conditions could be declined by banks or card issuers.The practical impact was easy to see. Auto-renewing subscriptions, which depend on the merchant quietly charging the saved card each month, were no longer allowed to remain quite so quiet.RBI wanted customers to know a recurring debit was about to happen. It wanted them to have an opportunity to stop it. It wanted an authentication layer around mandate registration and certain later transactions. Apple, like Netflix, Spotify, Adobe and plenty of other subscription businesses, had built systems for a world where saved cards did most of the work in the background.India had decided that background billing required more light.Then came tokenisation.RBI’s tokenisation rules changed how card data could be stored and used. A token is a substitute code for the actual card number. It is tied to a particular card, token requestor and device or use case. The merchant does not receive the real card number during processing. RBI says tokenisation is safer because the actual card details are not shared with the merchant, and the customer must explicitly consent through Additional Factor of Authentication when registering a token.That is the important bit. Tokenisation is not just a fancy way of saying “encrypted card”. It changes who holds what.Under RBI’s model, the actual card data and token-related details are stored securely by the token service provider, which may be the card network or issuing bank. The merchant or token requestor cannot keep the Primary Account Number, the actual card number, or other card details in the old card-on-file manner.Apple’s billing system had to be rebuilt around that reality.The company’s own 2021 developer guidance recommended Apple Account balance as a fallback, noting that users could add money using cards, net banking, RuPay and UPI even when recurring card payments were being disrupted. That workaround tells the whole story. Apple could still take money in some forms. It could not make its old recurring card system operate in India without changing the plumbing underneath it.The consumer-facing restriction landed in 2022. Apple told Indian users that, from 1 June 2022, credit and debit cards would no longer be accepted for purchases or subscriptions across the App Store and related Apple services because of upcoming RBI requirements.That makes the current return a roughly four-year story, not a neat five-year blackout. The warning began in 2021. The real consumer disruption took hold in 2022. The distinction matters because it shows how long the repair work has taken.Four years to restore a card field.That is not because Apple lacks engineers.It is because payment systems are where software meets regulation, banks, fraud rules, liability, national data policy and every unpleasant edge case that occurs when a subscription tries to collect ₹75 at 2.14 am.Tokenisation solved a security problem. It also created a product problem.RBI’s intent was sensible.Saving millions of card numbers across merchants, gateways and payment intermediaries creates a large attack surface. A breach at one merchant can expose data that should never have been sitting there. Tokenisation reduces that risk by replacing the card number with a token that is useful only in a particular context.The RBI describes tokenisation as available across contactless payments, QR payments, apps and other channels. It lets customers set transaction limits and choose how a tokenised card is used. It also gives them the option to deregister a token later.For a consumer, the result should be safer payment credentials and more control.For Apple, the result was an awkward engineering and compliance challenge.The company could not simply keep its global billing design and call the Indian version “close enough”. It had to work with card networks, issuing banks and payment infrastructure that could satisfy RBI’s rules on tokenisation, consent and data handling.The other complication is data localisation.RBI’s payment-data rule requires the entire payment data relating to payment systems operated in India to be stored only in India. The regulator says this includes end-to-end transaction details, customer information, payment-sensitive data, payment credentials and transaction data. Processing can happen abroad in some cases, but the data has to be brought back to India and deleted from foreign systems within the required period.Moneycontrol reported that Apple has now agreed to a model where tokenised payment data is held on-device and with card networks, without mirroring Indian payment data to Apple’s own overseas servers. The report also said Apple does not have an Indian data centre and is unlikely to build one in the near term. The company has not publicly described its India payment architecture.That distinction matters because there is an easy, wrong conclusion floating around: that Apple is storing Indian payment data in India on some mysterious new Apple server farm.The public evidence does not show that.The more likely arrangement is that Apple has adjusted its role so the card network, issuer and compliant local payment participants hold the sensitive payment information required by RBI rules, while Apple operates within the boundaries of tokenised credentials and device-level security.That is not Apple surrendering privacy. It is Apple accepting that India’s payments regime decides where the regulated record lives.What users will notice, and what they will notFor users included in the initial rollout, the change should be refreshingly dull.They may see an option to add an eligible Visa or Mastercard credit or debit card under Apple Account payment settings. That card could then be used for App Store purchases, iCloud+ storage, Apple Music, Apple TV subscriptions and other Apple digital transactions. The user should still expect bank verification, card eligibility checks and potentially different treatment for a one-time app purchase versus a recurring subscription.Not every card will work.Not every bank will be ready on day one.Not every Apple user will receive the option at the same time.And no, repeatedly deleting and re-adding UPI, changing the Apple Account country, signing out of iCloud or installing a beta will not magically produce Apple Pay in Wallet. It may produce a headache. Apple’s own payment pages say payment methods vary by region and can change.The practical advice is straightforward:Open Settings on iPhone.Tap your name.Open Payment & Shipping.Check whether Add Payment Method offers a card option.Use a card issued in India and expect authentication through the issuing bank.Keep UPI Autopay or Apple Account balance active until a direct card payment has actually worked.Do not cancel an existing iCloud+ payment route just because you saw a report about cards returning.The phrase “rolling out” has ruined more subscriptions than any technical bug.Apple Pay is related to this. It is not the same thing.This is where the story becomes both more interesting and more irritating.Apple Account card billing is a merchant-payment function. You use a card to pay Apple for an app, subscription, storage plan or media purchase.Apple Pay is a digital wallet and payment service. You add an eligible card to Apple Wallet, authenticate with Face ID, Touch ID or a passcode, then use the phone or Apple Watch to pay in shops, inside apps or on websites.One pays Apple.The other lets the iPhone pay everybody else.Apple Pay uses device-specific tokenised card credentials. Apple says a bank or card issuer creates a Device Account Number, encrypts it and sends it to the device’s Secure Element. The real card number is not stored on Apple Pay servers or backed up to iCloud. Each payment uses a unique security code, and merchants do not receive the full card number.That is exactly the sort of architecture that sounds compatible with RBI tokenisation. And in principle, it is.RBI permits tokenisation on mobile phones, watches, tablets, laptops and other devices for contactless payments, QR-based payments and apps. The rulebook is not inherently hostile to a phone wallet.But compatibility in principle is not market entry.Apple Pay needs participating banks. It needs card-network support. It needs commercial agreements. It needs issuer-level card provisioning. It needs the correct treatment of authentication. It needs regulators satisfied with data and audit arrangements. It needs merchants with contactless terminals for physical payments. It needs an answer to the question every Indian payments executive will ask within fourteen seconds: why should this be better than UPI?Re-enabling cards for App Store billing addresses one piece of that stack.It does not complete the stack.Apple Pay in India: what has changed, and what has notApple has not announced Apple Pay for India.India does not appear on Apple’s official country-and-region list for Apple Pay. Apple’s support material says Apple Pay is available only in supported markets with participating banks and card issuers. The India section of Apple’s payment-method page lists Apple Account balance, Mastercard, Visa, net banking and UPI. It does not list Apple Pay.That is the official position.The reported position is more advanced.Reuters reported in February that Apple was in talks with ICICI Bank, HDFC Bank and Axis Bank, as well as global card networks, about launching Apple Pay in India around the middle of 2026. Reuters said it could not independently verify the Bloomberg report on which the story was based.Moneycontrol reported in May that Apple Pay’s technology and infrastructure were ready, but negotiations with banks had stalled over commercial terms. Apple was reportedly seeking 20 basis points per transaction while larger banks were willing to offer 15 basis points. Apple and the banks did not comment.That is not a small gap.A basis point is one-hundredth of one percentage point. Five basis points can sound trivial to people who do not spend their working lives arguing about payments. It is not trivial when multiplied across large volumes of high-spending card transactions, especially in a market where banks already compete on rewards, interchange, partner offers and card acquisition costs.Apple’s pitch to a bank is familiar: Apple Pay can improve card security, make transactions quicker, keep customers in the issuer’s card product and present the bank’s card as the default payment method on a premium consumer device.The bank’s reply is equally familiar: UPI already handles an enormous volume of payments at low cost, customers are not asking loudly for another wallet, and Apple would like to be paid for the privilege of becoming part of the card transaction.That is not a technical disagreement. It is a negotiation about who gets the economics of the iPhone user.The UPI problem is not that Apple cannot understand UPIIt is that UPI changes the commercial equation.India has trained users to pay by scanning a QR code and approving a transaction through a bank-linked account. The payment feels immediate. It is usually free to the consumer. It does not require a premium phone. It does not require a contactless card terminal. It works on Android devices that outnumber iPhones by a wide margin.Apple Pay, by contrast, is built around tokenised cards, Wallet provisioning, NFC contactless payments and online checkout. It can make card payments more secure and convenient. It cannot turn a physical card into a superior version of UPI merely by adding Face ID.Moneycontrol reported that Apple was not keen to launch with UPI because UPI operates under a zero Merchant Discount Rate framework. That is a reported commercial position, not an Apple statement. But it makes sense. Apple Pay has historically been built around card rails, where the company can negotiate economics with issuers. UPI’s zero-MDR structure leaves much less room for Apple to extract a payment fee.This is why a future Apple Pay launch in India may arrive as a card-first service.That would mean:Tap iPhone or Apple Watch at a contactless card terminal.Authenticate with Face ID, Touch ID or device passcode.Use an eligible Indian Visa, Mastercard, RuPay or Amex card, depending on which banks and networks join.Pay online or inside an app through Apple Pay where merchants have integrated it.It would not automatically mean Apple Pay can scan every UPI QR code in the country.It would not automatically replace PhonePe, Google Pay or Paytm.It would not automatically make Apple Wallet a UPI app.Could Apple add UPI support later? Possibly. There is no official confirmation that it will. The card-payment restoration does not establish it.Why RBI’s newer authentication rules may matterApple’s long-standing hesitation around India was not only tokenisation and data localisation.It was also authentication.Apple Pay is designed around biometric approval. Look at the phone, confirm the transaction, let the Secure Element and card network do their work. It is supposed to feel immediate. The Indian preference for OTP-based additional authentication made that experience harder to reproduce.RBI’s newer digital-authentication directions, which took effect in 2026, permit a broader range of authentication methods while maintaining the requirement for multiple factors. Reporting on Apple Pay preparations says this has created room for biometric authorisation in card payments, which is closer to the Face ID-led flow Apple wants.The newer e-mandate framework also helps make recurring payments less punishing for normal subscription amounts. The framework requires authentication for registering or changing a mandate, pre-transaction notifications at least 24 hours before a debit, the ability to opt out, and additional authentication for recurring charges above ₹15,000. Charges below that threshold can proceed without another authentication step, subject to the mandate framework.For iCloud+, Apple Music, Apple TV and most App Store subscriptions, ₹15,000 is well above ordinary monthly pricing.That does not mean Apple is now free to charge cards however it likes. It means the regulatory path is clearer than it was during the 2021-22 disruption.The country has not relaxed security. It has modernised the ways security can be delivered.That is an important difference.What this means for Apple’s services business in IndiaApple’s Indian hardware business is easy to see. Stores, iPhones, MacBooks, AirPods, launch queues, EMI offers, bank discounts, film stars taking low-light portraits of brunch.The services business is less visible. It arrives as a ₹75 storage plan, a recurring music subscription, a game purchase, an app upgrade, an Apple TV renewal, an in-app payment or a family member wondering why the cloud backup failed again.Those small charges are the sort that should be effortless. They are also the charges most likely to fail when payment systems are badly fitted to local rules.Direct card payments can reduce failed renewals for users who prefer cards, especially those with credit-card rewards, corporate cards, bank-linked subscription management or no interest in setting up UPI Autopay. They can also reduce the need to maintain a prepaid Apple Account balance, which is workable but inefficient. Users have to estimate the amount, top up in advance and remember that money once added remains trapped inside Apple’s commercial orbit until it is spent.For developers, the return matters because billing failures damage subscription businesses in quiet ways.An app does not usually lose a customer because the product suddenly became terrible. It loses the customer because a renewal fails, access stops, the user gets distracted and the subscription is never restarted.Apple recognised this in 2021 when it advised developers to use Billing Grace Period and to communicate with customers whose card payments had been declined under the new Indian rules.Direct card billing will not solve every subscription churn problem. It should remove one particularly unnecessary one.The bigger lesson: India is not a feature checkboxApple has become very good at expanding into markets through hardware. Payment services are harder.A country can buy iPhones without Apple having to negotiate every part of the domestic financial system. A payment product has to fit the country’s banking rules, fraud controls, consent standards, data rules, card networks, merchant acceptance and commercial incentives.India is not a market where a global wallet can arrive with a polished launch video and assume the rest will take care of itself.The consumer already has three payment apps, six QR codes and a tolerance for payment friction that vanishes the moment the checkout takes more than ten seconds.Apple’s decision to restore cards for its own services shows that it has accepted this. The company is no longer treating Indian payment requirements as a temporary nuisance around the edges of the App Store. It is changing its own systems to operate inside them.That is why this story matters beyond iCloud storage.The return of direct cards is not Apple finally giving Indian users a convenience feature out of generosity. It is a sign that Apple’s India strategy is getting more serious, more local and less reliant on the idea that a global default will do.What users should watch nextThere are five signals worth following.1. Apple updates its India billing support page.The clearest sign of a broad rollout will be Apple explicitly stating that direct Visa and Mastercard payments can be used for subscriptions and App Store purchases in India, not only for adding account balance. At present, the support pages do not yet tell one clean story.2. RuPay and American Express support.Moneycontrol reports that Apple is working on these networks after Visa and Mastercard. RuPay support would matter symbolically and practically in an India-first payment market.3. Named Apple Pay banking partners.Apple Pay is not real for consumers until a bank says its cards can be added to Wallet.4. An Apple Pay India country listing.When India appears on Apple’s official Apple Pay country list, the speculation phase is over.5. A clear UPI answer.Apple may arrive with cards only. It may later integrate UPI. It may choose a different route. Until Apple states its plan, any confident claim that Apple Pay will “support UPI from day one” is a guess dressed as a launch detail.Bottom lineApple restoring card payments to the App Store in India is a modest change with a large backstory.For users, it could mean iCloud+ renewals, app purchases and Apple Music subscriptions once again work with the debit or credit card already sitting in their wallet.For Apple, it means the company has reportedly rebuilt its billing system around Indian tokenisation, authentication and data requirements after years of living with a workaround.For Apple Pay, it is a foundation stone, not the building.The company still needs banks. It still needs commercial agreements. It still needs to make a card wallet compelling in a country where UPI already owns daily payments. And it still has not announced a launch.Apple has reopened the card door.Apple Pay has not walked through it yet.FAQHas Apple restored credit and debit card payments for the App Store in India?Apple is reportedly restoring direct Visa and Mastercard payments in phases for App Store purchases, iCloud+ and Apple subscriptions. The rollout is limited at first, and Apple has not issued a formal public announcement confirming universal availability.Why did Apple stop accepting cards in India?Apple’s older card-billing system was affected by RBI rules around recurring transactions, customer authentication, e-mandates, tokenisation and the handling of card data. Apple warned developers in September 2021 that recurring card payments could be declined under the new requirements, then removed direct card payment support for Indian users in 2022.Can I use Apple Pay in India now?No. Apple Pay is still not officially available in India, and India does not appear on Apple’s current list of supported Apple Pay countries and regions. Direct card payments for Apple Account purchases are separate from Apple Pay.Will Apple Pay support UPI in India?Apple has not announced UPI support for Apple Pay in India. Reports suggest Apple has focused on card-network and bank partnerships, while UPI’s zero-MDR structure has complicated the commercial case. Any claim that Apple Pay will support UPI at launch remains unconfirmed.Which cards are expected to work first?Moneycontrol reports that Visa and Mastercard cards are active in the initial testing phase, with RuPay and American Express expected later. Availability will depend on Apple’s rollout, card network and issuing-bank support.What should I do if I cannot add my card yet?Keep using UPI Autopay or Apple Account balance for subscriptions and purchases. Check Settings, your Apple Account and Payment & Shipping periodically, but do not change country settings or cancel an existing payment route until a card has been added and charged successfully.end of article

Apple is bringing card payments back to the App Store in India But Apple Pay is still awaited

Apple is reportedly restoring Visa and Mastercard payments for App Store and iCloud purchases in India. Here is why cards stopped, how RBI rules changed billing, and why Apple Pay is still not live.

4,098 words~19 min read