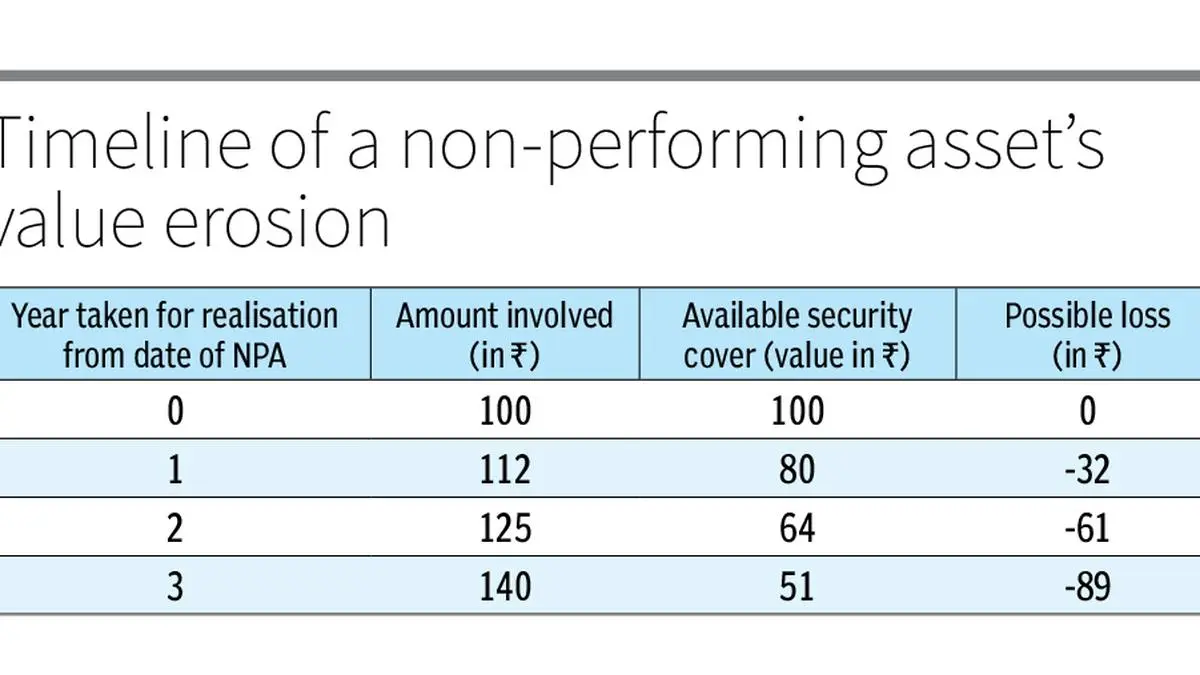

There has been a spate of news recently on the sale of loans to asset reconstruction companies (ARCs) and the settlement of loans at low prices. Here it is important to understand the market dynamics and other commercial aspects that influence the pricing of a distressed debt. Once an account turns into a non-performing asset (NPA), the value of the underlying security starts deteriorating, while the dues of the bank keep increasing on expected lines, as there is the ‘time value of money’. An apple once rotten cannot fetch the same optimal value it attracted in its prime state.The value erosion and nosediving price can be explained using Table 1. Let us take 12 per cent as interest rate (time value of money) and a 20 per cent deterioration of security value each year. These are approximate numbers used for the limited purpose of explaining value erosion. Even in the case of a loan with 100 per cent security, the position turns as shown.True, this is an oversimplified table, used only to provide a perspective on how the loss on an NPA sale increases with each passing year, all other things remaining constant. One important thing to note is that the major component of this is the notional loss of accrued interest.The entire NPA sale process — from banks to ARCs or, for that matter, to other eligible entities like banks and thousands of non-banking financial companies (NBFCs) — is through an auction process, with an additional Swiss challenge method for larger loans. One must trust that the market is right and the equilibrium price is attained through the price discovery mechanism. There could be aberrations, which need to be dealt with as per regulations and laws.ARCs — the entities known as ‘bad banks’ — acquire bad loans from the books of banks and resolve them through various permissible asset reconstruction measures, which include restructuring, asset sales, settlement, and so on. ARCs are regulated by the RBI, which covers their entire lifecycle and areas of functioning, including the settlement process, where the amount and logic is vetted by an independent advisory committee consisting of professionals.Bad banks help banks exit bad loans and focus on lending (good banking), which in turn aids economic growth. There is a direct correlation between credit growth and GDP. The Indian landscape is dominated by consortium lending and/or multiple lending due to the concentration and exposure norms in banks and risk management. When a loan turns bad, recourse to recovery processes like SARFAESI (Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest) or Insolvency and Bankruptcy Code (IBC) requires a certain threshold of consent from creditors (60 per cent and 66 per cent, respectively) to drive the process. ARCs fit in here by aggregating debt and driving resolution. Besides, the specialised skills developed at ARCs over two decades of experience aid in value maximisation.An analysis of other mechanisms versus ARC sales shows some interesting results.Agreed, IBC is not strictly a recovery mechanism, and its performance need not be evaluated only on the basis of recovery, as many cases are closed even before admission and there is an appreciation in value post resolution and so on. The aggregated recovery is low, as many cases are of pre-IBC vintage and with no tangible security, from the days of the Board for Industrial and Financial Reconstruction (BIFR).In ARC sales, since there could be part payment in security receipts (amount paid only if realised from underlying assets), the effective return for banks holding security receipts could be less. However, in a sale to ARCs there is always a minimum upfront cash payment, unlike in a legal mechanism, where payment is received only after the recovery case is disposed of.So, ARCs have been an integral part of the financial system, helping banks focus on their core activities and quarantining NPAs. Banks had a gross non-performing asset ratio of over 11 per cent in FY2018, which dropped to 2 per cent by FY2025. The absolute level of NPAs has fallen from ₹10 lakh crore to ₹4 lakh crore during the period, with banks transferring ₹9 lakh crore total dues (NPAs inclusive of interest) to ARCs. After discounting the effect of this added unrealised accumulated interest, it can be assumed that, but for the sale to ARCs, banks today would possibly have been struggling with a staggering additional NPA volume, equivalent to the level they hold today, imposing a drag on their capital and credit creation.

‘Bad banks’ are like vitamins for good banks

Explore how asset reconstruction companies (ARCs) help banks manage non-performing assets and enhance their focus on core lending activities.

791 words~4 min read