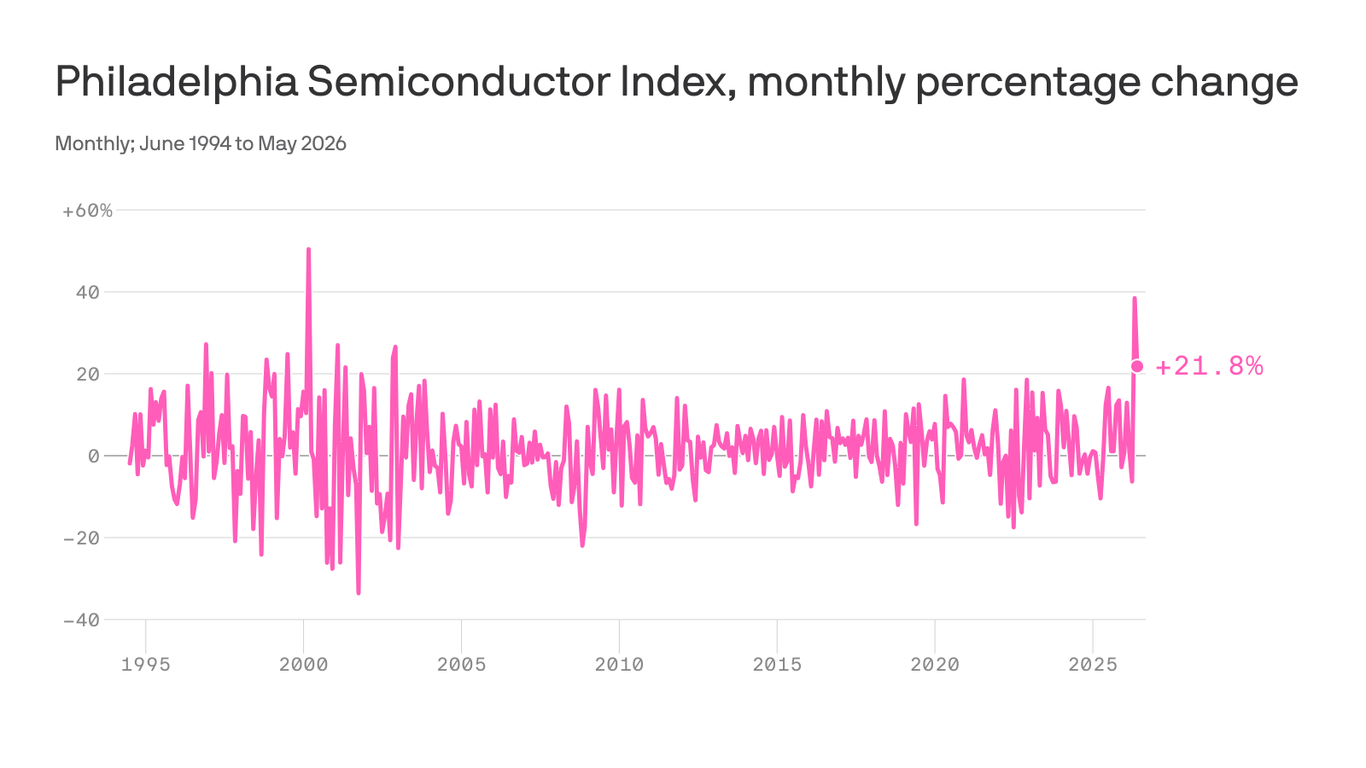

Despite the turbulence, stocks notched their best quarter in six years, overcoming recurring AI stock valuation fears, high oil prices alongside a geopolitical flare-up, inflation concerns, and the prospect of higher-for-longer interest rates. Most of the quarterly gains stemmed from the AI-adjacent rally, despite the brutal volatility: the iShares Semiconductor ETF (SOXX) soared nearly 90% in Q2, its best quarter on record.

A tight group of ten tech stocks representing the “picks and shovels” of the AI supply chain, plus Alphabet (GOOGL) and Apple (AAPL), drove almost 80% of the SPX’s gain in the first half of 2026. However, tech jitters, sparked by another rotation attempt, carried into the second half of the year, with the S&P 500 and Nasdaq-100 getting hit – and SOXX giving up more than 8% over the first two days of July – while the DJIA notched an all-time high.

Continued valuation worries and heavy profit taking – especially in memory, including Micron (MU), SanDisk (SNDK), and other hardware and infrastructure names that have rallied hard in recent months – outweighed the impact of macro news for the tech sector investors. While the NDX dropped hard on Thursday and the SPX finished flat, the Dow closed out its fourth-straight week of gains with a rally, encouraged by lowered expectations for a Fed interest-rate hike after a weaker-than-expected jobs report.