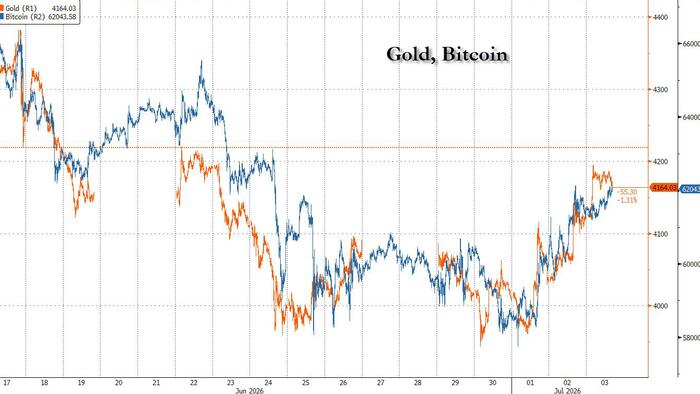

While US cash markets are closed for the July 4th holiday, stocks around the world rebounded from yesterday's momentum rout as the latest round of jitters about the AI trade subsided, with Europe’s benchmark rising to an all-time high. S&P futures rose 0.3% and Nasdaq 100 futures rebounded 1.2% in thin holiday trading after South Korean memory giants SK Hynix and Samsung Electronics recovered, helping to drive a 2% rally in Asian shares after earlier tumbling with SK Hynix plunging as much as 30% from its all time high. Europe’s utility and technology sectors outperformed to set the Stoxx 600 up for a second straight record close. The dollar touched a two-week low amid another mjni flash crash in the USDJPY overnight while gold extended gains.Friday’s gains marked the latest turn in a stretch of choppy trading as markets grapple with whether the second quarter’s AI-driven rally has gone too far. With stocks recovering after a two-day rout in chipmakers, investors are waiting for the upcoming earnings season as the next signal of whether massive spending on AI infrastructure can translate into profits.“The fundamentals are still very, very strong and the market is still underpricing them,” Tim Moe, Goldman equity strategist told Bloomberg TV. “There still is a lot longer to go in the overall positive profit environment for memory stocks and the AI hardware supply chain space overall.” With momentum crashing, its funding counterparties in the momentum pair trades, bitcoin and gold, jumped. Gold rose 1.2% to around $4,170 an ounce, the highest level in nearly two weeks, after money markets dialed back expectations for Federal Reserve interest rate hikes this year. Bitcoin also moved sharply higher, reversing from its recent rout and rising above $62. Having previously dislocated dramatically, gold and bitcoin are back to trading as the same asset class. The outlook for easier monetary policy also weighed on the dollar, which headed for its worst weekly performance since May. Meanwhile, the yen swung between gains and losses as speculation grew that Japanese authorities may be less predictable in how they intervene to support the currency.Worries that persistent inflation pressures would leave the Fed little choice but to tighten policy have subsided in recent days, with oil prices easing and an unexpectedly sharp slowdown in US labor market growth. The first fully priced-in quarter-point Fed hike has moved back to December, from October.“Unless and until we see clearer signs that the energy spike has filtered its way through to underlying inflation, we think that the Fed will opt for a cautious approach to policy tightening,” noted Matthew Ryan, head of market strategy at Ebury.European stocks were little changed in early Friday trading, but still set to wrap up their fourth straight week of gains, as investors remained optimistic that the Federal Reserve will hold off on rate hikes for now.The Stoxx 600 traded little changed at to 648.41, with utilities outperforming while consumer and personal good firms underperform. Here are the biggest movers Friday:Genfit shares jump as much as 15%, with the French biopharmaceutical company saying it’s set to benefit from US Medicare coverage for a diagnostic blood test for liver disease, known as NASHnext, which is powered by Genfit’s technologyPluxee gains as much as 8.6%, to the highest in almost two months, after the employee benefits provider delivered a slight beat in the third quarter and maintained its full-year guidanceMIPS gains as much as 19%, the most in nearly two years, after the Swedish helmet technology firm announced it settled a patent infringement lawsuit initiated by BrainGuard. Pareto Securities says the news removes a key overhangAFRY gains as much as 6.4%, the most since April, after the Swedish engineering consultancy’s recommendation was raised to buy from hold at Pareto Securities, expecting its upcoming second-quarter report to “mark a turn in AFRY’s earnings trajectory”Maersk gains as much as 4.6% after being raised to neutral from sell at Goldman Sachs, with the bank turning “less negative” on the 2027 supply-demand outlook, seeing a “slightly later and shallower acceleration in new capacity growth in 2027”Craneware shares tumble as much as 31%, the most in seven years, after the software company warned that FY26 financial performance is likely to be below market expectationsStellantis shares fall as much as 1.7% after the carmaker was downgraded to reduce at HSBC, which says it’s concerned about cash outflows and the potential need for de-stockingAsian stocks rose at the end of a volatile week as shares of heavyweight South Korean semiconductor makers bounced back following a two-day slide. The MSCI Asia Pacific Index rallied as much as 2.2%, erasing early losses. Samsung, SK Hynix and Japan’s Kioxia each jumped more than 8%. Anthropic is in talks with Samsung to be a manufacturing partner for a custom AI chip, according to a report. However, TSMC’s shares slipped, tracking declines in US chip stocks. Friday’s rebound in Asia was also aided by improved risk sentiment after weaker than expected US June employment data and lower oil prices challenged expectations for Federal Reserve rate hikes this year. The MXAP index lost 1.4% in the previous session, when chipmakers plunged on concerns over excess AI capacity and intensifying competition. It is up 1.5% for the week. This week’s price action has served as another reminder that the fortunes of Asia’s benchmark remain closely tied to a handful of tech names. The two Korean chipmakers and Kioxia carry a combined more than 12% weighting in the regional gauge. TSMC alone holds close to 11% — the most for a single stock.“We’re looking much more forward now in terms of expectations, in terms of growth, what 2027 will look like,” said Billy Leung, investment strategist at Global X Management, in a Bloomberg TV interview. “The AI trade’s really got breadth now,” with infrastructure and energy supply names also offering opportunities beyond memory chips, he added.Looking ahead, Samsung is expected to announce its preliminary quarterly earnings on July 7 while SK Hynix will list ADRs on the Nasdaq next Friday. Traders will be watching for monetary policy decisions from New Zealand and Malaysia’s central banks next week. Several other companies in the region are due to report earnings, including Fast Retailing, Seven & i and Tata Consultancy Services.Brent steadied below $72 a barrel as traders weighed the outlook for increased supply through the Strait of Hormuz and continuing talks between the US and Iran.Meanwhile, nervousness about AI valuations has seen investors turning away from US stocks at the fastest pace since March, according to Bank of America Corp. strategists. The country’s stock funds had $17.2 billion in outflows in the week through July 1, the team led by Michael Hartnett wrote in a note, citing EPFR Global Data. Investors turned to some international stocks instead, with Japanese equities seeing their biggest inflows in seven weeks at $1.9 billion.Market WrapS&P 500 futures rose 0.3% as of 9:26 a.m. New York timeNasdaq 100 futures rose 1.2%Futures on the Dow Jones Industrial Average fell 0.2%The Stoxx Europe 600 rose 0.5%The MSCI World Index rose 0.2%The Bloomberg Dollar Spot Index was little changedThe euro rose 0.1% to $1.1444The British pound was little changed at $1.3354The Japanese yen was little changed at 161.22 per dollarBitcoin rose 0.7% to $61,973.66Ether rose 2.1% to $1,739.81Germany’s 10-year yield advanced three basis points to 2.93%Britain’s 10-year yield advanced two basis points to 4.80%West Texas Intermediate crude was little changedSpot gold rose 1.2% to $4,170.41 an ounceDB's Jim Reid concludes the overnight wrapHappy Independence Day to our US readers as they celebrate 250 years of AMEXIT. A reminder of our piece on the US quarter millennium success story and the prospects of that continuing in the decades ahead can be found at the Deutsche Bank Research Institute here.

Futures Rebound With Cash Markets Closed; Gold, Bitcoin Jump

“We’re looking much more forward now in terms of expectations, in terms of growth, what 2027 will look like"

2,729 words~12 min read