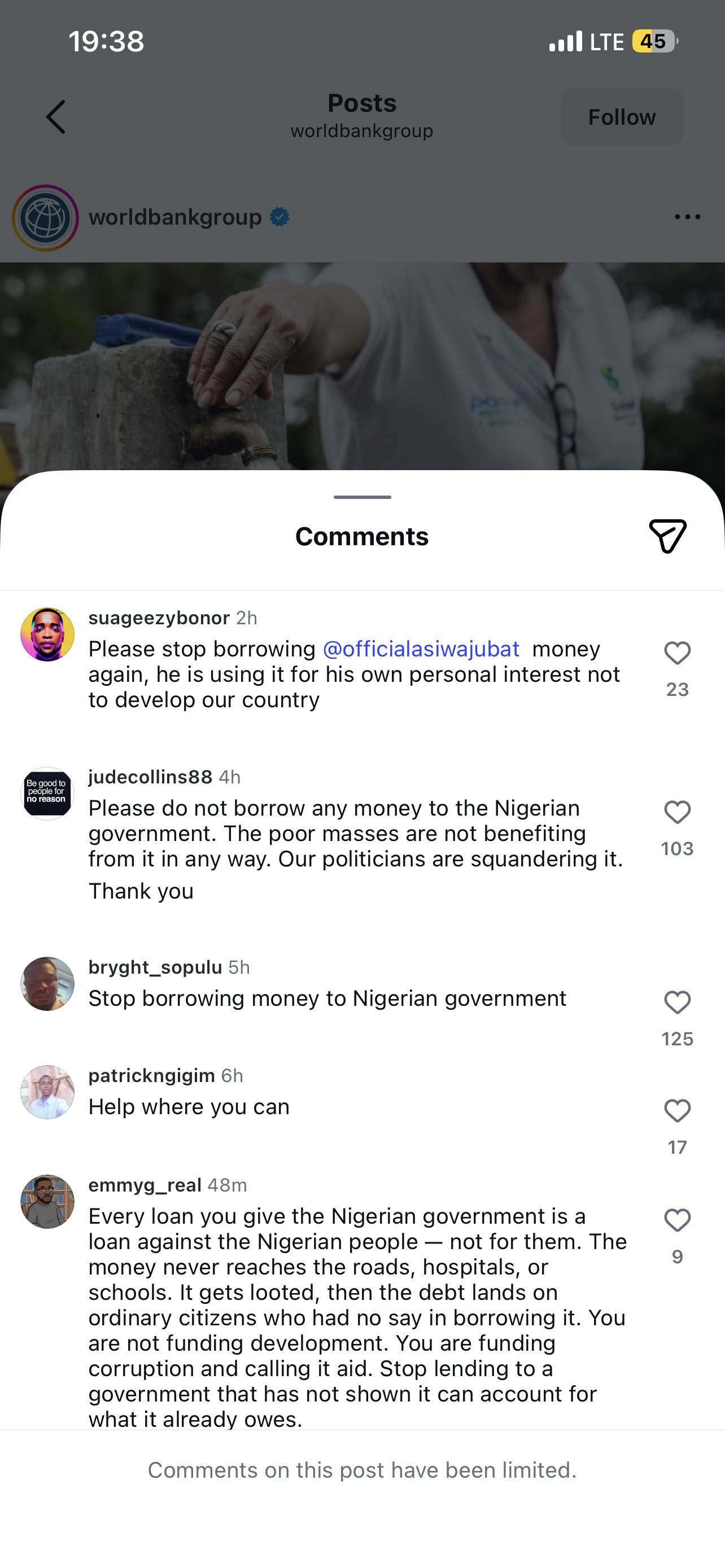

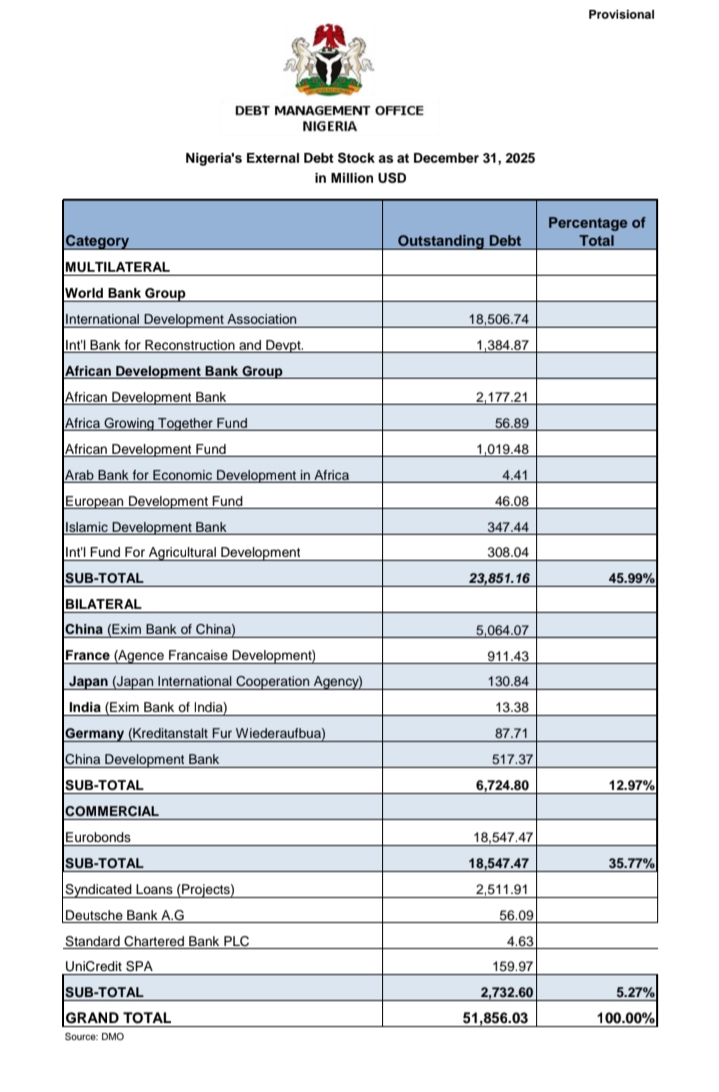

The World Bank has approved a $1.25bn loan for Nigeria under its Nigeria Actions for Investment and Jobs Acceleration programme, despite recent public backlash over the country’s rising debt burden and calls by many Nigerians for the lender to halt further borrowing.

The approval was announced in a statement issued by the World Bank on Wednesday, alongside the launch of a new Country Partnership Framework for Nigeria covering 2026 to 2032.

The bank said the new framework would guide its support for Nigeria over the next six years, with a focus on creating jobs by unlocking private sector-led growth.

“The World Bank Group has endorsed a new Country Partnership Framework for Nigeria spanning 2026-2032, setting out a strategy to create more and better jobs at scale by unlocking private sector-led growth,” the statement read.

It added that the bank had “also approved the Nigeria Actions for Investment and Jobs Acceleration Development Policy Financing operation, which supports Nigeria’s transition toward a more inclusive growth model that spurs growth and creates jobs.”