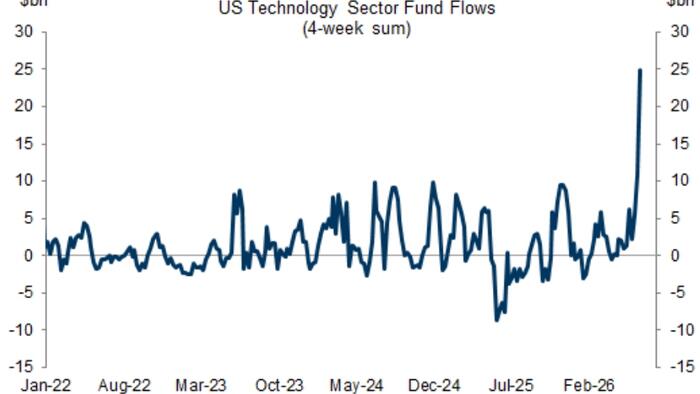

The inflow of money into U.S. equities is running well above the average this year, according to Christian Mueller-Glissmann and his team at Goldman Sachs. One aspect of that is that “Investors are increasingly deploying leverage to participate in the equity rally,” they said in a recent note. “Net margin borrowing”—where traders magnify the effect of their bets by borrowing a multiple of their own money—is now at about $1.4 trillion. That’s the equivalent of 1.8% of all U.S. stocks.

While leveraged investors can make more money on their trades by borrowing against their own stakes, they also stand to lose by a similar multiple if their bets go wrong. That adds an extra level of risk into the market—traders forced to cover their losing bets may end up selling other stocks to raise cash, thus magnifying selling pressure in the markets.

“Outside the U.S., margin purchases of Japanese equities have also climbed above $30 billion, the highest level since the GFC [Great Financial Crisis],” Mueller-Glissmann said in a note seen by Fortune. “Investor leverage remains very concentrated in the AI ecosystem.”

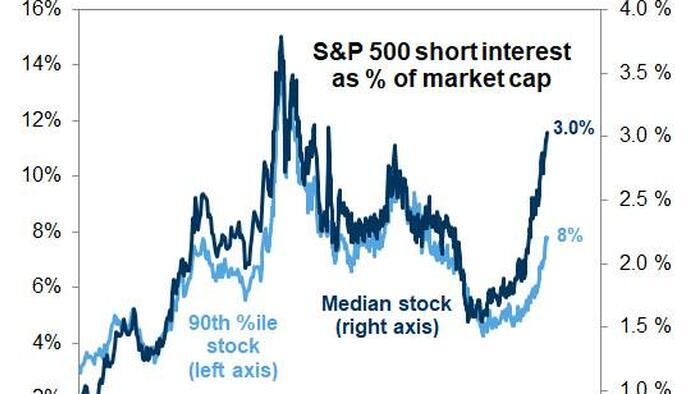

The Magnificent Seven have become a bit of a drag

As this chart from Jim Reid and his folks at Deutsche Bank shows, the big tech stocks have underperformed the S&P 500 so far this year. Reid names four reasons why: 1. Extreme positioning (they were overheld). 2. People are still worried that AI hyperscaler capex won’t be able to generate profits. 3. The Fed got more hawkish about interest rates. And 4. The cost of shipping has gone up since the Iran war.