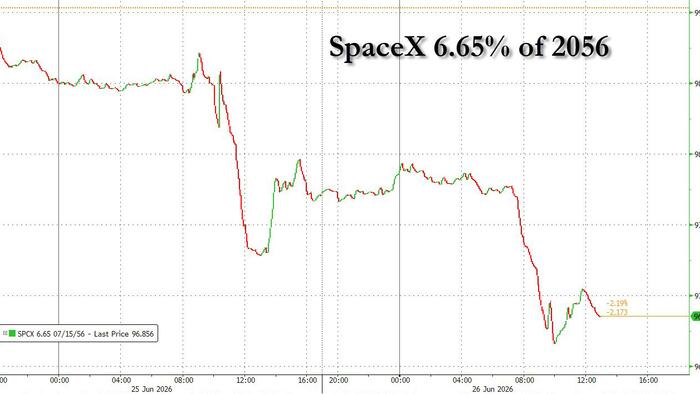

Submitted by QTR's Fringe FinanceSpaceX’s debt honeymoon lasted about as long as a meme stock gamma squeeze.Traders are already taking meaningful paper losses on SpaceX’s $25 billion bond offering, with losses totaling roughly $305 million relative to Treasuries just days after issuance, according to Bloomberg.Even veteran credit traders appear surprised by how quickly the deal has deteriorated in the secondary market. One dealer reportedly quoted the longest-dated bonds 0.28 percentage point wider than their original issue spread, while Bloomberg noted that several traders “can’t recall another recent deal that widened this sharply.”Portfolio manager Tony Trzcinka summed up the mood: “We expected SpaceX to widen from issuance level, but not this much.” He pointed to a combination of weak technicals, the enormous supply, and investors “still scratching their heads over how to price its unique risk profile.”Imagine that. Bond traders are scratching their heads but this tattooed ex-bartender from Philadelphia has a pretty damn good idea why the bonds have sold off.This is exactly what happens when you can’t lock down 95% of the float, squeeze every short seller into oblivion, and force passive indexes to stuff the security like a dildo up a Thanksgiving turkey’s ass into everybody’s retirement account.There is no equivalent financial engineering machine operating in the secondary corporate bond market like there is in equities, as I wrote last week: How Wall Street Launders Dogshit Into Retirement FundsBond investors actually have to care whether they’re being compensated for risk.They don’t get to manufacture demand through index inclusion. They don’t get a perpetual bid from retail call-option gamblers chasing momentum. They don’t get gamma squeezes forcing dealers to buy ever-higher prices. They don’t get every ETF on Earth mindlessly vacuuming up more shares simply because the market capitalization keeps inflating itself.They just have buyers...and sellers. That’s why I believe the bond market is giving investors a much cleaner signal than the equity market as to how much risk is really in SpaceX…and it’s why I went apeshit last week about its bloated equity valuation being totally unnatural and potentially systemic: SpaceX Could Get Dangerously SystemicI’ve been arguing since the IPO that SpaceX’s valuation made little economic sense. A company that still expects years of negative free cash flow was briefly being assigned a valuation north of $2.6 trillion…larger than almost every publicly traded company on Earth. Bulls waved away every concern because “it’s SpaceX,” because “it’s Elon,” because AI, because Mars, because narratives have replaced analysis.The bond market doesn’t give a f*ck about narratives. It cares about getting paid back.Bloomberg points out that SpaceX’s longer-dated bonds are now trading much closer to Oracle’s credit curve than where they were originally priced. That’s the market slowly repricing risk after the...(READ THIS FULL ARTICLE HERE). Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.Loading...

SpaceX Slams Head First Into The Bond Market

The bond market doesn’t give a f*ck about narratives. It cares about getting paid back.

TL;DRAI

SpaceX's $25B bonds lost $305M within days, spreads widening 0.28 points—signaling market skepticism on fundamental valuation. Unlike equities, bond markets price risk accurately; SpaceX's negative free cash flow contradicts its $2.6T valuation, revealing narrative engineering.

483 words~2 min read