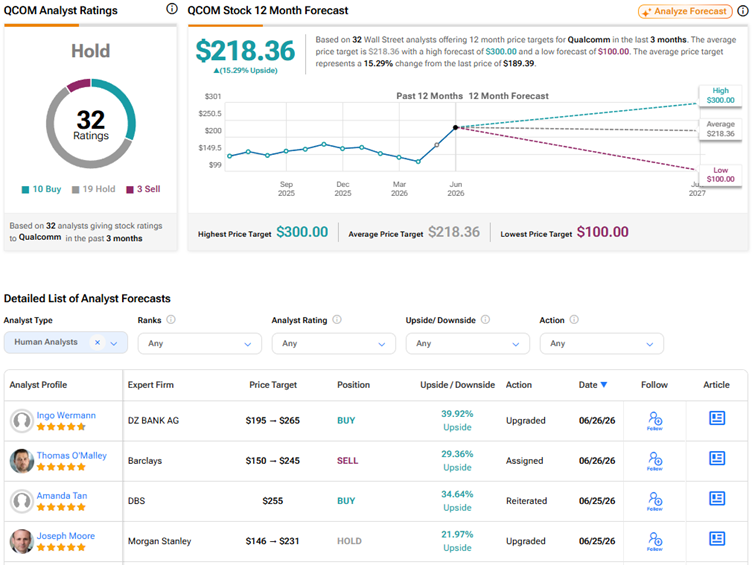

Barclays Analyst Says ‘Sell’ Qualcomm Despite Solid FY29 Targets

Ahead of the Investor Day event, O’Malley expected Qualcomm to unveil a major U.S. hyperscaler customer for its custom silicon/AI accelerator business. Instead, the company announced two global hyperscaler customers for customer silicon and disclosed a deal with Meta Platforms to supply its C1000 CPU.

The 5-star analyst highlighted that Qualcomm raised its non-handset revenue target for Fiscal 2029 to $40 billion from $22 billion. The new target includes an estimated $10 billion in automotive revenue, more than $14 billion in IoT (Internet of Things) revenue, and over $15 billion in data center revenue.

Given diversification efforts, O’Malley noted that the company expects handsets to contribute just below 50% of estimated sales in Fiscal 2027 and one-third of Fiscal 2029 sales. Overall, Qualcomm is upbeat about its growth prospects and projects a total addressable market (TAM) of $1.7 trillion by 2030 across licensing, Android handsets, auto, IoT, and data center.

While O’Malley raised his multiple for QCOM stock to align with peers’ valuations and to reflect its broadening business model, he remains bearish as he sees “this is a show-me story in a highly competitive market.” He noted that Qualcomm is facing challenges in the handset market amid memory shortages and the risk of losing business from Apple (AAPL) as the iPhone maker moves to in-house modems.