Six months of running a Rust trading bot live, then replaying historical tick data through the same code. The results were not what I expected.

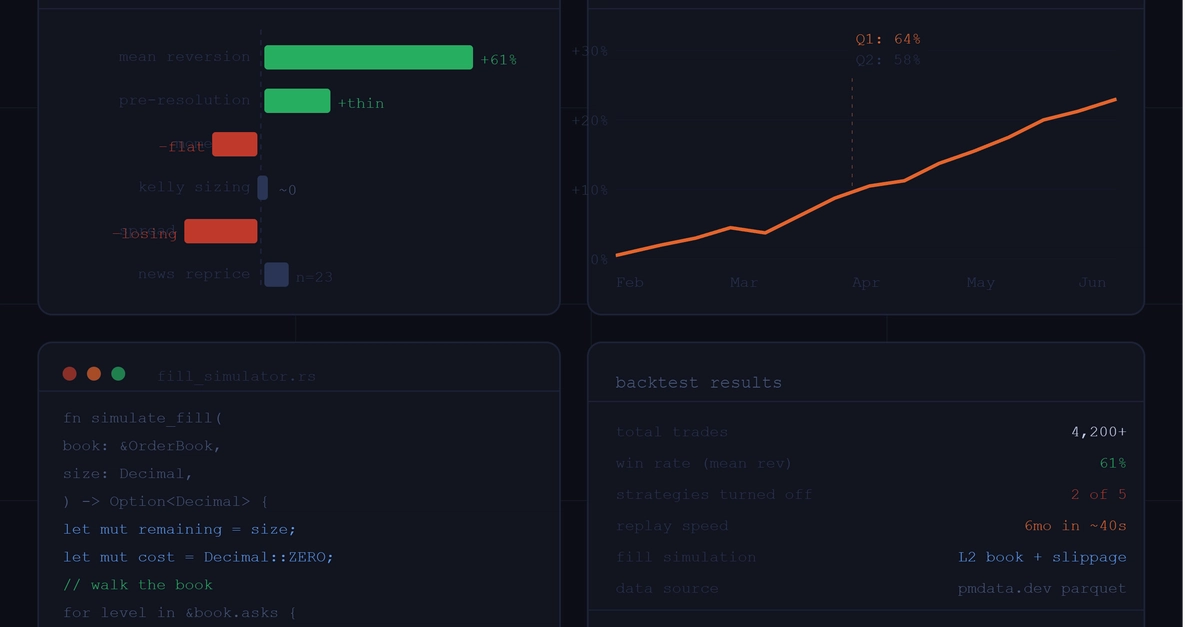

The bot had been running for six months. It felt like it was working. P&L was positive. Win rate looked decent. And then I actually backtested it.

Turns out I had been lucky on a few large positions that masked two strategies that were quietly bleeding. I wouldn't have known without replaying real historical data through the same code that runs in production.

This is how I built the backtester, what data I used, and what I found.

The data problem