This is AI generated summarization, which may have errors. For context, always refer to the full article.

Alejandro Edoria/Rappler

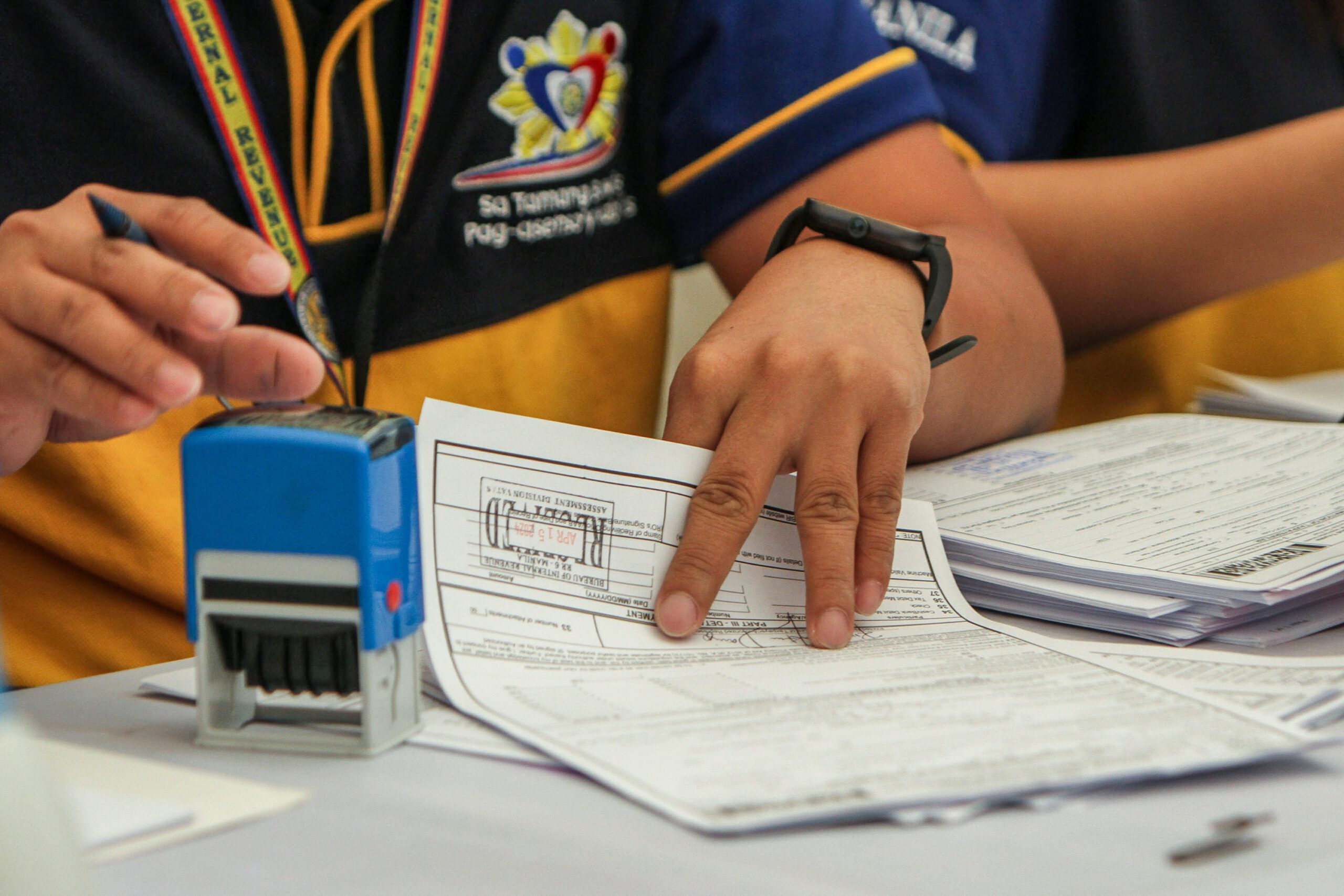

Ask the Tax Whiz clarifies the specific conditions and processes under which export-oriented enterprises may apply for a VAT zero-rating in light of recent BIR issuances

As Export-oriented Enterprises (EOE) navigate the evolving value-added tax (VAT) zero-rating process, understanding the implications of the updates or changes is critical for compliance and strategic planning.

To provide further clarification, Revenue Regulations (RR) No. 10-2025 and the related Bureau of Internal Revenue (BIR) issuance Revenue Memorandum Circular (RMC) No. 32-2025 provided key updates.