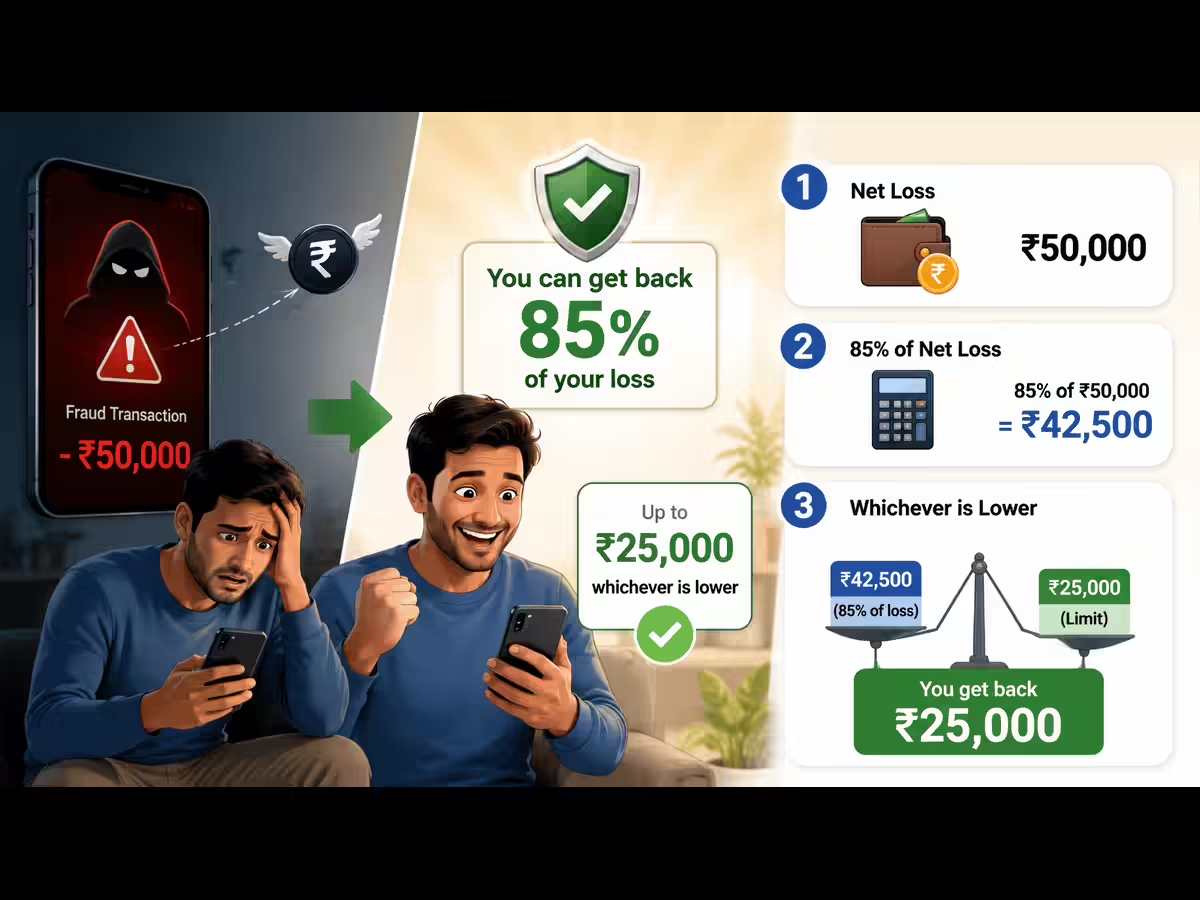

Reserve Bank of India (RBI) on Wednesday broadened its framework for limiting customer liability in digital transactions to cover a wider range of payment scams, including cases where customers are tricked into transferring money to fraudsters posing as legitimate recipients, and introduced a compensation mechanism for victims of small-value digital frauds.Under the revised framework, bona fide victims suffering losses of up to ₹50,000 due to fraudulent electronic banking transactions will be eligible for compensation of 85% of their net loss, subject to a maximum of ₹25,000, once during their lifetime.Also read: RBI to raise large exposure limit for upper layer NBFC-IFCs to 45% from 35% of eligible capital baseThe central bank said the amended directions will come into effect from January 1, 2027.The revised rules also cover cases where a third party uses credentials obtained fraudulently to carry out transactions and situations where customers approve transactions under coercion or duress.As part of the new framework, banks will be required to examine complaints and establish liability within 45 calendar days in cases involving domestic fraudulent electronic banking transactions and within 60 calendar days for cross-border cases. Banks will have to communicate the reasons to customers if these timelines are exceeded.For fraudulent transactions involving credit cards, banks will be required to provide a shadow reversal equivalent to the disputed amount within five calendar days of receiving notification from the customer.Further, RBI has also retained the requirement for banks to send instant SMS alerts for electronic transactions above ₹500, saying SMS remains the only electronic mode of communication available to customers without smartphones or internet access.

RBI expands digital fraud protection, introduces compensation for small-value scam victims

The RBI has expanded customer protection rules for digital payment frauds to cover cases where people are tricked into sending money to scammers and introduced a compensation mechanism for small-value frauds. Eligible victims can receive up to 85% of their losses, subject to a cap of ₹25,000. The rules take effect from January 1, 2027.

263 words~1 min read