Below is a summarized version of The Block Research's Strategy: The Capital Stack Meets a Falling Bitcoin Price report. The full PDF version of this report is accessible here.

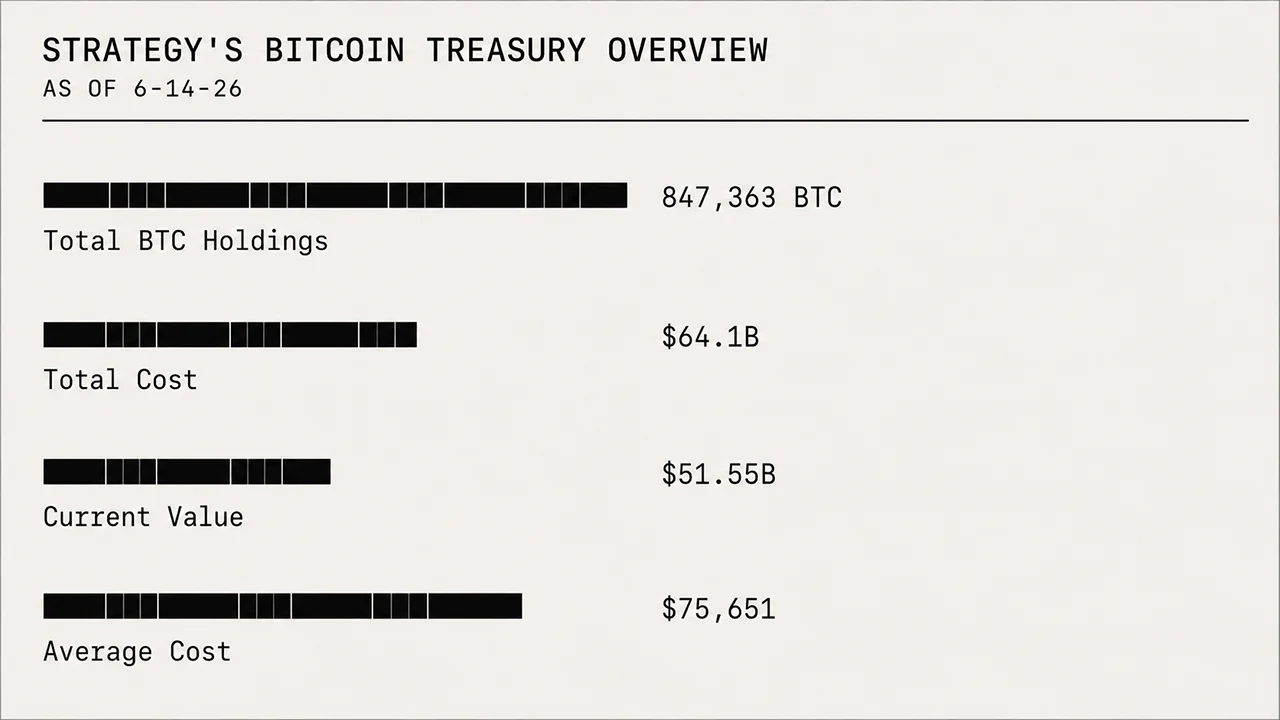

Strategy Inc., formerly MicroStrategy, faces the first real test of its Bitcoin-treasury model. It holds 847,363 BTC acquired for $64.10 billion, or an average of $75,651. At a treasury value of about $54.7 billion, it is about $9.4 billion underwater, about 14.6% below cost.

This is also the first time the full preferred-funded capital stack has been in place during a deep drawdown. There is no mechanical liquidation price. Strategy's core debt is senior unsecured and the Bitcoin is reported as unencumbered. The question to watch is whether future secured financing or senior preferred issuance changes the waterfall. The real exposure is liquidity, carry, and capital-markets access: roughly $1.7 billion of annual preferred dividends, noteholder put dates beginning in 2027, and a $1.4 billion USD Reserve that covers only months of those dividends on its own and is management-designated; it is not escrowed.

MSTR common is not "Bitcoin at a discount." It looks cheap on the headline ratio (market cap over gross Bitcoin), but once debt and preferred claims are subtracted it trades at a premium to what the common actually owns, its residual common NAV. Because that claim is levered, it falls faster than Bitcoin. Whether the premium then widens or compresses as Bitcoin moves is a behavioral question the NAV section takes up, and the caution here does not depend on resolving it.