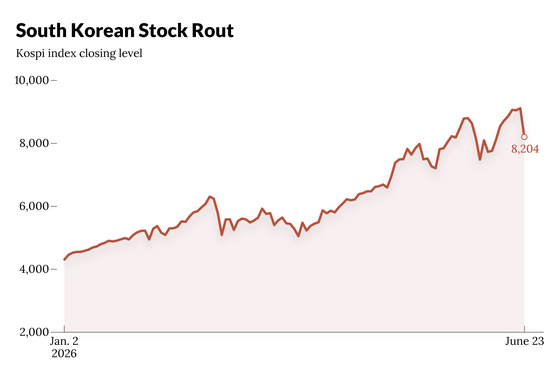

US equity futures are sharply lower as a Semis/South Korea-induced selloff has spread globally slamming tech stocks and pushing SpaceX 3% lower and below its first day of trading price of $150. Nasdaq stocks lead sentiment and early trading lower with AI cost concerns back in focus, as Bloomberg notes that traders are pointing to a South Korean media report we first highlighted at 8pm last night, saying SK Hynix is slowing expansion of AI memory chip production and shifting emphasis to commodity DRAM. As of 8:00am S&P futures were -1.3%, and Nasdaq futures tumbled 2.7%, both near session lows. In premarket trading, Intel and Micron led a broader decline among chipmakers while SpaceX fell 4.3%, below its $150 initial trade price. Chinese equities in Hong Kong entered a bear market. Mag7s are dragging the indices lower with MSFT / telecom the safety valve. In Seoul, chip giants SK Hynix Inc. and Samsung Electronics Co. slumped more than 10%. According to JPM, today's sell-off "may reflect anxiety into MU’s print on Weds as well as the levered ETF mkt structure." Bonds are operating as a safety haven as the yield curve bull steepens, and USD is bid. Commodities are seeing further declines in Energy as US / Iran discussions continue and precious metals are getting hit due to USD (gold) and AI / Tech (silver). Ags are mixed. Today’s macro data focus is on Flash PMIs, ADP’s weekly employment print, and regional Fed activity indicators. In premarket trading, chipmakers, memory stocks and other AI-related firms slide during the broader selloff. Decliners include Micron (MU -7%), Intel (INTC -6%), AMD (AMD -6%) and CoreWeave (CRWV -5%).Nvidia leads most of the Magnificent Seven group lower (Nvidia -2%, Tesla -2%, Meta -0.6%, Microsoft +1%, Apple -0.3%, Amazon -0.6%, Alphabet -2%,)Avis Budget (CAR) climbs 4% as the rental car company entered into a settlement agreement with Pentwater Capital Management and affiliated persons to resolve a lawsuit seeking recovery of short-swing profits, the company said in a filing.Best Buy (BBY) falls 3% after the company said Matt Bilunas will step down as CFO and depart the retailer at the end of July after 20 years, including seven years as CFO.Edgewell Personal Care (EPC) rises 9% after people familiar with the matter said the maker of Schick razors has rejected an unsolicited takeover offer from private equity firm Yellow Wood Partners.IBM (IBM) gains 4% as JPMorgan upgrades to overweight and as the company announced it has joined the OpenAI Daybreak Cyber Partner Program.Primoris Services (PRIM) sinks 35% after the infrastructure construction company cut its adjusted earnings guidance for the full year.In other corporate news, Oracle reduced its workforce by 21,000 employees in the past 12 months, a wider scale than previously known, including those whose jobs were eliminated by the use of AI. SoftBank’s founder said there’s little merit to building data centers in space, while acknowledging that AI competition is intensifying. In an ugly session that started with a rout in South Korea, the Kospi finished down 10% while Nasdaq 100 contracts lose 2.5% and are struggling to find a floor. European stocks are not immune with the Stoxx 600 down 1%. Other assets have been caught up in the equity selloff with spot silver down over 4% and Bitcoin dropping 3%. Memory stocks, many of which are riding triple-digit gains this year, recorded some of the steepest losses. SpaceX was poised to fall below its first-day opening price of $150. In Seoul, chip giants SK Hynix Inc. and Samsung Electronics Co. slumped more than 10%. Intel Corp. and Micron Technology Inc. led a broader decline among chipmakers in US premarket trading, while SpaceX fell 4.3%. Chinese equities in Hong Kong entered a bear market. BofA equity derivative strategists said the Nasdaq 100’s heavy concentration in technology stocks has fueled its outperformance versus the S&P 500 in both returns and volatility. That’s pushed the Nasdaq’s Bubble Risk Indicator (BRI) closer to a key level which often signals elevated near-term tail risks. Meanwhile, already jittery tech sentiment and volatility could turn on a dime after Micron’s earnings tomorrow. The chipmaker has been the largest contributor to S&P 500 gains this year, while technology stocks make up each of the index’s 10 biggest drivers of returns.“Some of the recent performance in stocks has been highly speculative, fueled by a passion from retail investors for short-term gains,” Mark Dowding, chief investment officer for fixed income at RBC BlueBay Asset Management, told Bloomberg TV. “We may not like it this morning, but actually it’s healthy behavior.The market selloff “is largely a blip, but it is tapping a real and more fundamental anxiety,” said Amanda Lyons, head of research at Energy Group Capital. “The blip part: it is a single piece of local trade press, landing into a jumpy tape and a day before a nervous Micron print, on a trade that is about as crowded and as priced-for-perfection as anything in the market.One regular buyer of stocks, the corporates themselves, are exiting for the time being. Goldman’s Vani Ranganath estimates approximately 65% of companies have entered their blackout window ahead of 2Q results.For the AI trade, attention is now shifting to Micron’s quarterly results on Wednesday after the stock rallied more than 300% since January.“The real test is Micron,” said Amanda Lyons, head of research at Energy Group Capital. “I would watch the rate of change in pricing and any change to capex or bit-supply guidance far more closely than the headline beat or miss.”Fed’s Goolsbee said he remains concerned about inflation and questioned whether all the factors driving prices up are temporary. US Trade Representative Jamieson Greer kicked off talks with Indian officials this week as both sides stepped up efforts to resolve the remaining differences holding up an interim trade agreement.In other assets, currency traders are on high alert for intervention after further weakness in the yen. Gold slides, with Deutsche Bank following Goldman in cutting price forecasts for the metal.European equities fell sharply at the open on Tuesday: the Stoxx 600 falls 1.1% to 632.10, with mining and technology shares leading declines while health care and food beverage stocks are the biggest outperformers. Here are the biggest movers Tuesday:Porsche shares rise as much as 1.8%, erasing early declines after the German luxury carmaker confirmed its forecast for the 2026 financial yearBasic resources stocks are falling the most in the Stoxx Europe 600, with the sector index down as much as 4.6%, as metals fell across the board on inflationary concerns and progress of peace talksHermes shares fall as much as 2.9%, extending its drop to 11% over the past three sessions, after HSBC downgraded its rating on the Birkin bag maker to hold from buyEpiroc drops as much as 5.6%, the most in three months, as UBS downgrades the Swedish mining-equipment maker to sell from neutral and says its valuation “has gone too far”Signify plunges as much as 18% after the Dutch lighting manufacturer announced new medium-term targets and an updated dividend policy that analysts say would mean big cuts to shareholder payoutsTelecom Plus shares plunge as much as 33%, sending shares to their lowest level since 2012. The company’s new five-year plan will see it invest with the ambition of improving growth and the quality of earningDometic declines as much as 11%, the most since March, with Danske Bank cautioning its upcoming 2Q report will be held back by tough US markets for its RV and marine divisionsEarlier in the session, Asian stocks fell reversing the previous session’s gains as a selloff in technology shares weighed on regional markets. The MSCI Asia Pacific Index dropped as much as 3.6%, with SK Hynix and Samsung Electronics among the biggest drags. Most of the region’s major markets were in the red, led by declines in South Korea, Japan and China. A sub-gauge of information technology shares slid as much as 6.1%, after rallying 2.3% on Monday. South Korean stocks tumbled 10% from a record high as investors dumped chip heavyweights on concerns that the rally has become overstretched, prompting the local exchange to briefly halt program selling. Japanese equities slipped as some AI-related stocks fell following a selloff in US tech megacaps.“I think our Asian markets are tracking a rotation already underway in the US rather than a fresh risk-off move,” said Billy Leung, an investment strategist at Global X Management. “Hyperscalers have been leading the pullback on AI capex concerns and negative cash flow concerns.”In FX, the Bloomberg Dollar Spot Index gains 0.2% although the yen takes top place among the G-10 currencies, climbing a few pips against the greenback. The Aussie dollar is the weakest, falling 0.7%.In rates, treasuries are richer across the curve with gains led by front-end and belly, as oil steadies and stock futures slump after a selloff in Korean chipmakers stoked concerns about the artificial intelligence trade. US yields richer by as much as 4bp across front-end and belly with 2s10s and 5s30s spreads steeper by 1bp and 3bp on the day; 10-year is around 4.48%, 3bp richer on the day with bunds and gilts in the sector outperforming by around 1bp: German and UK 10-year yields falling 3 basis points each. SpaceX shares fell to the lowest level since their first day of trading ahead of a potential jumbo investment-grade bond sale that could be announced Tuesday. Focal points of US session also include June preliminary PMIs and a 2-year note auction. This week’s Treasury auctions begin at 1pm New York time with $69 billion 2-year note sale, to be followed by 5- and 7-year notes Wednesday and Thursday; WI 2-year yield near 4.20% is ~13bp cheaper than the May auction, which stopped on the screws.In commodities, Brent crude futures fall 1% to around $77 a barrel. Other assets have been caught up in the equity selloff with spot silver down over 4% and Bitcoin dropping 3%.Today's US economic data calendar includes weekly ADP employment change (8:15am), June Philadelphia Fed non-manufacturing activity (8:30am), June preliminary S&P Global US manufacturing and services PMIs (9:45am) and Richmond Fed manufacturing and business conditions indexes (10am). Fed speaker slate empty for the session.Market SnapshotTop Overnight NewsKorea's KOSPI plummeted 9.99%, its steepest drop in more than three months, on Tuesday as overseas investors sold chipmakers following regulatory signals that the sector's rally had gotten overheated. RTRSSouth Korea’s retail investors are ploughing profits from a world-beating stock market into an overheated property sector, confounding government efforts to cool real estate demand. FTIran said $12 billion of its frozen funds were set to be released as part of ongoing talks with the US, with the two sides broadly signaling progress in negotiations to formally end their war. BBGThe Trump administration and Qatar have warned the EU that it faces a gas supply crunch that would force up prices unless Brussels rewrites planned rules on methane emissions. BBGThe yen erased losses after Japanese Finance Minister Satsuki Katayama said she spoke with Scott Bessent and that they agreed that “bold action” may be needed. Traders are on high alert for intervention. BBGEuro-area business activity shrank less than anticipated in June. S&P Global’s Composite PMI rose to 49.5 from 48.5, topping estimates but remaining below the 50 mark that indicates growth. BBGThe UK’s economy contracted for a second consecutive month, with its PMI slipping to a 14-month low. BBGThe Fed’s Austan Goolsbee told American Public Media’s Marketplace he remains concerned about inflation and questioned whether price pressures will persist after temporary shocks have dissipated. BBGTSLA logged a more than twofold jump in European monthly sales in May as Elon Musk’s electric-vehicle maker continues to rebuild strength in a region where Chinese rivals are gaining ground. WSJUS Senate passes bipartisan affordable housing bill.Iran War Latest Iran's Foreign Ministry Spokesperson Baghaei said "if the other party does not fulfill its obligations, we should not be expected to unilaterally fulfill our obligations", Iran International reported.Iran's Foreign Ministry Spokesperson said defensive capabilities and missiles will never be a topic of discussion. US commitment regarding Lebanon is completely clear.Iran's Foreign Ministry Spokesperson said quadrilateral talks were stopped early in Switzerland due to the witnessing of US threats. Thereafter, exchanges were via a mediator, Mehr reported.Iran's Foreign Ministry Spokesperson said Iran has no plans to let IAEA inspectors visit nuclear sites targeted in the conflict.Iranian President, ahead of trip to Pakistan, said Iran is seeking the full implementation of the clauses that have been signed within the framework of international law, Nour News reported.Iranian Parliament Speaker Ghalibaf said the Strait of Hormuz will be administered by Iran according to international law.Iranian President Pezeshkian said in phone call to Turkish President Erdogan on Monday that Iran is ready to pursue diplomacy as per international law.Iran Central Bank Governor said Tehran is not obliged to purchase US agricultural goods under current agreements, and states that remaining frozen assets can be used to buy non-sanctioned goods beyond essential items, according to Tasnim."Iranian Foreign Minister Abbas Araghchi will visit Baghdad next Sunday", Al Mayadeen reported citing sources; The meeting will include a briefing on the progress of the talks in Switzerland and the preparations.Iranian Foreign Ministry said "America has issued the necessary license for the sale of Iranian oil and petrochemical products", Al Jazeera reported.Iranian Ambassador to the UN said any further attacks on Lebanon would be a red line.Iranian Ambassador to the UN said Hormuz talks will be held with Oman.Iranian Ambassador to the UN said there has been good progress in negotiations with the US."Sources indicate that the Iranian Foreign Minister [Araghchi] will hold separate talks with Pakistani officials", Al Hadath reported.Oman's Foreign Minister said Iranian negotiators reaffirmed their commitment to international law and to ensuring safe, toll-free passage through the Strait of Hormuz.Oman's Foreign Minister meets with Iranian Parliamentary Speaker Ghalibaf, with the officials discussing regional stability and Strait of Hormuz.Shipping data cited by Al-Arabia showed at least 20 ships have crossed the Strait of Hormuz in the past 24 hours.One person reportedly killed by Israeli gunfire in a southern Lebanese town, according to Lebanese Civil Defense and a security source - timing unclear.Senior US official tells Al Jazeera that talks between Lebanon and Israel will continue to advance comprehensive peace and a security agreement between the two countries.Israeli National Security Minister Ben-Gvir said Israel must act alone against Iran's nuclear program and must maintain military freedom in Lebanon, hopes withdrawal from southern Lebanon will not happen and will do everything to convince PM Netanyahu.Israel military shells and fires at Khan Yunis in Gaza, according to Fars News Agency.Israel's PM, Defence Minister and Military Chief said Israeli military will continue to act to neutralise threats to soldiers and citizens, demolish terrorist infrastructure, and maintain security zone in southern Lebanon, according to a joint statement. Israel's leadership reaffirms that the security of Israeli citizens and IDF troops will remain its overriding priority, with no room for compromise.Israeli forces reportedly violate Syrian territory, conducting house searches in southern outskirts of Quneitra governorate.US-Iran technical talks in Burgenstock had a "breakthrough", talks proceed seemingly in a positive direction, Journalist Mallick reported.US President Trump, on Israel and Lebanon, said "we'll take a look at it"; said he gets problems solved fast, including with Israeli PM Netanyahu.US President Trump said if Iran doesn't stick to agreement, he will do what he has to do. As long as Iran respects us, we are not going to have any trouble. Could restart the blockade quickly if needed.A more detailed look at global markets courtesy of NewsquawkAPAC stocks were subdued with initial choppy price action following the mixed performance stateside, where participants reflected on the progress in US-Iran talks, but communication stocks and the Nasdaq Comp underperformed. KOSPI, -6.9%, led the sell off, moving to a test of 8.5k to the downside. ASX 200 traded little changed for most of the session amid a lack of major fresh catalysts overnight and as the strength in financials and defensives offset the losses in the tech and commodity-related sectors. Nikkei 225 swung between gains and losses with the index briefly climbing to a fresh record high before reversing course, and is on track to snap its 8-day win streak. Hang Seng and Shanghai Comp conformed to the lacklustre mood in the region and the absence of any major fresh catalysts, with the Hong Kong benchmark pressured by losses in miners, and digital platforms stocks amid a rotation out of hyperscalers into semiconductors.Top Asian NewsChina's MOFCOM announces measures to stimulate the auto after-sales market; to support the integration and upgrading of the car rental industry.Japanese Chief Cabinet Secretary Kihara said will take appropriate action against FX moves if needed.Canada awarded Australia a USD 1.75bln contract for its over-the-horizon radar system, boosting Arctic early warning capabilities, and which marks Australia's largest ever defence export.Japanese S&P Global Composite PMI Flash (Jun) 52.50.Japanese S&P Global Manufacturing PMI Flash (Jun) 54.9 vs. Exp. 54.5 (Prev. 54.5).Australian S&P Global Manufacturing PMI Flash (Jun) 51.2 (Prev. 50.7).Blackstone (BX) President and COO Gray told Nikkei that the firm plans to invest USD 30bln in Japanese data center development over the next three to five years.Large losses in Kospi (-9.9%) crept through to Europe (STOXX 600 -1%) with EU tech leading the losses. No specific headline driver for overnight losses in a typical non-conflict risk-off move (stocks/oil down, fixed/havens bid). As you would expect, South Korean heavyweights Samsung and SK Hynix (which account for over 50% of the index) led the declines, both falling 12%. Some analysts point out the mechanical rebalancing from leveraged ETFs exacerbated losses with a large share of the vehicle used to gain Kospi exposure coming as leveraged ETFs. Others point out positioning into Micron earnings due after the close on Wednesday. Given the above, Tech is the worst sectoral performer (bar Basic Resources), the sector posting losses in excess of 3%. The highest weighted chip constituents ASML -5% (Highest weighted in Europe+Tech Sector), Prosus -2.1% and STMicroelectronics -7.3%. For Basic resources, the sector has been dragged lower by declines in metals (Gold -2.5%, Silver -5.5%).Top European NewsGerman Chancellor Merz outlines his support for a capital-based pension system, saying it "strengthens the system".German Chancellor Merz confirms plan to push forward with all pension reform proposals.Britain’s biggest business lobby group, CBI, said UK firms are not seeking another Brexit referendum and have little interest in rejoining a customs union with the EU, according to FT.UK's Burnham will seek to soothe markets as he marches on number 10 and will use a speech next week to pledge to grow the economy and commit to Labour's fiscal rules, according to The Times. Burnham is considering Miliband, Streeting and Mahmood for Chancellor.FXG10s are entirely lower against the Buck (bar JPY), as USD attracts haven demand in a textbook risk-off market move (stocks/oil down, fixed/havens bid), signalling the market is gradually moving away from geopolitical trade. As you would expect, Antipodeans underperforms, Aussie fares the worst as metals suffer from the strong Buck, while JPY is the only currency stronger vs the USD after a sharp 30pip move lower as it sits towards 2024 highs.DXY firmer by 0.2% as it attracts haven demand amid tech weakness in Kospi/NQ (see equities at 09:25 BST for analysis). In terms of domestic newsflow, Fed's Goolsbee said services inflation was “a little disturbing”. The data docket is light but begins to pick up today (ADP weekly + PMIs due) heading into Thursday's GDP revisions and PCE data. DXY surpassed Friday’s high of 101.12, now looks to the May peak just below 102.JPY continues to whipsaw around multi-year lows against the Buck, with USD/JPY towards 161.50-162. Japanese officials continue attempts to bolster the Yen, but continue unsuccessful with the Greenback bid. Overnight, Japanese Finance Minister Katayama confirmed she spoke with US Treasury Secretary Bessent on Monday. Elsewhere, APAC trade saw stronger flash PMI data and mixed results of the latest 5yr JGB auction.GBP is weaker and tracks the firmer Buck with participants awaiting further updates from a likely incoming Burnham premiership. Despite Gilts continuing to outperform peers on optimistic Burnham reporting (Streeting added to Chancellor candidates/Burnham said to announce commitment to Fiscal rules), Miliband still in the picture for Chancellor is viewed by Sterling traders as an unwelcome option. As such, GBP awaits further press reporting and tracks the Buck with Cable remaining at 1.32, EUR/GBP unchanged. ING this morning writes “Regardless of politics, we keep favouring higher EUR/GBP on the back of a dovish view (no hikes) on the Bank of England”. EZ/UK PMIs were mixed (see fixed income for analysis), EUR saw fleeting strength on the French figure, which indicated a cooling of cost pressures; a move which proved fleeting as the German services and composite metric cooled (Some respondents' answers did not eclipse the signing of the US-Iran MoU).Fixed IncomeA firmer start for fixed income as the complex benefits from the softer energy environment, though the influence of this has diminished amid recent updates from Iran, and the weak risk tone as the KOSPI closed lower by 9.9% and has weighed on European price action, with the European Tech sector lower by over 3%.USTs firmer by seven ticks in 109-06+ to 109-14+ confines, towards but just off highs as the mentioned energy move off lows has seemingly formed a ceiling in fixed or now at least. Ahead, we have the region’s Flash PMIs before 2yr supply. A tap that should benefit from a number of factors.Bunds firmer by just over 10 ticks and are just under that from the 126.74 high. Initially moving on the above, in-line with peers and with no real reaction to the latest pension reform commentary.The main updates, aside from the APAC moves, today have been Flash PMIs for June. Firstly, France’s figures sparked some modest EGB pressure as the components all came in firmer than expected. Internal commentary pointed to a possible peak in price pressures. Thereafter, Germany was below consensus but caveated by the majority of responses coming in before the MoU signing. Nonetheless, encouragingly, the series showed that inflationary pressures had started to ease off.Finally, the EZ figure was mixed and again most responses came before the MoU. But, it already showed that lower energy prices were filtering through to businesses with inputs cost rates and selling price inflation moving lower in June. Again, pointing to a potential price spike peak.Overall, the data chimes with those who believe that expectations for further ECB tightening are overdone. A point arguably added to by the pertinent commentary from President Lagarde on Monday. As such, upcoming hard and survey data will be scoured for confirmation that prices may have peaked which, alongside the stagnation in activity, may well see a dovish repricing in the period ahead.Gilts echoed the above, higher by 35 ticks at best and to a new WTD high of 89.19. Today’s strength also comes from reporting that Burnham will next week give a speech outlining his commitment to the fiscal rules; however, The Times briefing notes that Miliband remains in consideration to be Chancellor, a point that potentially caps any further upside.PMIs for the region were weak, though price commentary was also welcome and chimes with the view that the BoE is on hold for the foreseeable.The Netherlands sold EUR 1.98bln vs exp. EUR 1.5-2bln 3.50% 2056 DSL Bond: avg. yield 3.52% (prev. 3.51%).Japan sold JPY 1.9tln 5yr JGBs; b/c 3.11x (prev. 3.22x), average yield 1.905% (prev. 2.024%).Germany sells EUR 3.807bln vs exp. EUR 5bln 2.50% 2028 Schatz: b/c 1.90x (prev. 1.58x), average yield 2.57% (prev. 2.59%), retention 23.86% (prev. 22.80%)CommoditiesGeopolitical newsflow remains focused on the US-Iran talks, and the sometimes mixed commentary filtering out from the respective officials. As it stands, there does not appear to be any cause for concern, with President Trump and VP Vance both sounding positive about the initial talks; the Iranian side also said good progress has been made. However, looking between the lines reveals some contradictory remarks. On Monday, VP Vance said that Iran would allow the IAEA to inspect nuclear facilities. However, Iran’s Foreign Ministry Spokesperson stated that there are no plans to let inspectors visit nuclear sites targeted in the conflict; the nuance of “sites targeted in the conflict”, potentially offers some hints to the inner workings of the proceedings between the US and Iran. Do note that the Iranian President is visiting Pakistan today.The biggest risk to the talks is Israeli actions in Lebanon. Several high-ranking Israeli officials have suggested that Israel will continue its military operations in Lebanon. Comments which come ahead of the US-mediated Lebanon-Israel talks, which are set to begin today. A confab which spans over a couple of days, and focuses on finalising “pilot zones” within southern Lebanon and long-lasting peace.Crude benchmarks traded sideways for much of the APAC session, before then moving to lows heading into the European cash open. Since, WTI and Brent have bounced a touch off lows, to currently trade towards the mid-point of the days range. In more detail, WTI Aug’26 (-0.5%) sits within a USD 72.48-74.45/bbl range and Brent Aug’26 (-0.6%) holds within a 76.43-78.23/bbl range.Spot gold (-2%) extends lower amidst the continued hawkish mood in markets, which have kept the USD elevated. For gold specifically, a number of sell-side banks have cut their price forecasts for spot gold. On Monday, Goldman Sachs cut their year-end target to USD 4,900/oz (prev. USD 5,200/oz). Its model focused on the Fed, whereby every 50bps worth of easing adds c. USD 120/oz of support to spot gold. Most recently, Deutsche Bank cut its gold forecast by 22%. Today, the yellow metal holds at the bottom end of a USD 4,091 to 4,198/oz range; it may find support at a recent low of USD 4,023/oz, if the pressure continues.Base metals follow the downbeat risk tone seen across broader markets. 3M LME copper is lower by c. 1.8% and holds within a USD 13,396.35-13,671/t range.Rabobank lowers its Q3 Brent price forecast to USD 79/bbl (from USD 103/bbl), and Q4 to USD 78/bbl (from USD 93/bbl); sees Brent averaging USD 74.50/bbl in 2027, and USD 71/bbl in 2028.US Department of Agriculture reported a new case of screwworm in a Texas goat, taking total number of domestic detections to 16 cases.Central BanksFed's Goolsbee (2027 voter) said inflation is well above target and going the wrong way, adds need evidence this inflation is temporary and services inflation is a little disturbing. said:. We haven't had stagflation shock, and the job market has been stable. Fed Chair Warsh's approach is let's have less speculation about rates, less forward guidance, while Goolsbee said he is pretty sympathetic to that approach.ECB's Kazimir said they are data-dependent, but the direction for policy is clear.ECB's Lane said that inflation risks being above 2% for some time; increase in energy prices is expected to keep inflation well above target into H1'27. Remains attentive to both sides of the outlook. Energy shock is feeding through to broader inflation. labour market resilience, solid household balance sheets and public investment should support activity.ECB's Escriva said service-sector inflation is showing very strong persistence.GeopoliticsRussia and Ukraine may swap Prisoners of War soon, TASS reported.Ukraine's capital Kyiv issues an air raid alerts and authorities ask people to seek shelter.North Korea leader Kim Jong-un said North Korea will further assert its status and role as a nuclear power, adds will accelerate broader plans, enhance nuclear arms technology and develop water deterrence capabilities. accused US and South Korea carrying out the most dangerous provocations through nuclear war machinery. To accelerate building of 10,000-ton strategic guided missile cruiser.China's Beihai Maritime Safety Administration announced that parts of the Beibu Gulf will be closed to navigation due to military training from 11:00-12:00 Beijing time on June 23rd.US Event Calendar9:45 am: Jun P S&P Global US Manufacturing PMI, est. 54.6, prior 55.19:45 am: Jun P S&P Global US Services PMI, est. 51.1, prior 50.79:45 am: Jun P S&P Global US Composite PMI, est. 52.1, prior 51.510:00 am: Jun Richmond Fed Manufact. Index, est. 8, prior 13DB's Jim Reid concludes the overnight wrapWhen I started in financial markets in 1995, Alan Greenspan was a towering presence and arguably the first Fed Chair to become a global rockstar. At that point, he was eight years into what would become a 19-year tenure as Chair of the Federal Reserve. However, my own memories pale in comparison to those of my colleague Peter Hooper. Peter joined the Fed in 1973, later moving to DB in 1999, and worked closely with Greenspan for over 50 years.Peter has written a thoughtful remembrance following Greenspan’s passing yesterday at the age of 100. Drawing on first-hand experience as a colleague at the Federal Reserve and later recruiting him to be an adviser at Deutsche Bank, Peter highlights Greenspan’s intense curiosity, instinct for data and markets, and ability to identify structural shifts such as the 1990s productivity boom. In many ways, Greenspan was ahead of the data—something Kevin Warsh is attempting to emulate today—so there are clear parallels between the eras. It is a personal and insightful tribute from someone who had a ringside seat throughout Greenspan’s remarkable career, and it is well worth reading in full on the DB Research Institute site.Moving onto the remembering another landmark in history, 10 years ago today, those of us on this island marched to the polls to decide whether we wanted to stay in the EU or not. Ironically, I had a long weekend planned in the French Alps and left for the airport immediately after voting and arrived to a fierce thunderstorm in the mountains and news that the UK had voted to leave. It all felt fairly biblical and instead of enjoying a break I spent all night and the next 3 days glued to my work laptop.To mark the anniversary Sanjay and Shreyas have published a piece entitled "Brexit 10 years on: What's worked, what hasn't, what's next?" See it here ahead of our first in-person Deutsche Bank Research Institute event on Thursday reviewing the topic and all things UK related given the huge events of recent days. We may still be able to squeeze you in.The irony around the anniversary is that the shadow of Brexit partly claimed another UK Prime Minister yesterday with Keir Starmer resigning and heralding in what will be the 7th Prime Minister in that subsequent decade. The only viable candidate now seems to be Andy Burnham, who won last week’s by-election in Makerfield, after rival challenger Wes Streeting endorsed him yesterday to be leader. So, although nominations for the Labour leadership are set to open on July 9, currently it looks highly likely that Andy Burnham is the only candidate who would get more than 20% of MPs backing him to stand, meaning that a formal contest would be avoided. That’s reminiscent of when Labour last changed leaders in government back in 2007, when Chancellor Gordon Brown took over from Tony Blair without a contest. Under this timetable, Burnham could become the PM as soon as mid-July.Against this backdrop, UK assets responded relatively positively, as it looks like a period of extended uncertainty and a potential summer leadership contest have been removed. Speculation that Streeting may get the job of Chancellor was seen as a positive as well given his more moderate tendencies. The pound sterling was the strongest performing G10 currency on the day, up +0.14% against the US Dollar, whilst yields on 2yr (-4.5bps) and 10yr (-3.4bps) gilts moved in line with their European counterparts inspite of the political upheaval. Moreover, the FTSE 100 was up +0.72%, again similar to the STOXX 600’s +0.58% advance.Another G7 country in the news is Japan and this morning the currency is fairly flat after seeing a strong spike yesterday afternoon London time after it got within a whisker of hitting 40-year lows. It hit 161.93 versus a low of 161.96 in July 2024. Beyond that you have to go back to December 1986 to see weaker levels. There was speculation over imminent BoJ intervention with JNN reporting an online emergency meeting between Finance Minster Katayama and US Treasury Secretary Bessent yesterday. This meeting has been confirmed by Katayama this morning, who stated that the US and Japan are aligned on FX policy. This morning it's hovering remarkably quietly at 161.60 given all the noise.Less quiet are Asian equities which are falling on tech weakness. The KOSPI (-6.41%) is leading the declines, followed by the Nikkei (-1.66%), Hang Seng (-1.16%), Shanghai Composite (-0.37%) and S&P/ASX 200 (-0.26%). S&P 500 (-0.66%) and NASDAQ 100 (-1.19%) futures are also weak with the tech sell-off dominating. Early morning data showed that Japan's private sector activity expanded at its fastest pace in three months in June, driven by strong manufacturing output and a return to growth in the services sector, although firms faced the sharpest rise in input costs in nearly four years. The S&P Global flash Japan manufacturing PMI rose to 54.9 in June while the services PMI climbed to 51.8 from 50.0, indicating a renewed expansion in business activity after stagnating in May. As a result, the flash composite PMI, advanced to 52.5 from 51.1, marking the strongest pace of overall private-sector growth since March.This all follows mixed markets yesterday, as tech worries overpowered investor optimism about progress in the US-Iran negotiations over the weekend. So that meant the S&P 500 slipped -0.37%, with the Nasdaq (-1.32%) and Magnificent 7 (-2.17%) posting even steeper losses, dragged down by declines by Alphabet (-4.99%) and Amazon (-4.75%).Those equity losses were compounded by the latest rise in Treasury yields yesterday, as investors continued to price in a more hawkish Fed. Indeed, yesterday saw markets price in a 98% chance of a rate hike by the September meeting (up from 93% on Friday), and the 2yr yield (+4.8bps) closed at a 16-month high of 4.23%. Meanwhile, the 10yr yield was up +5.5bps to 4.51%, and significantly, the 10yr real yield (+8.0bps) hit a one-year high of 2.26%. That rise in real yields was something Henry looked at in a note yesterday (link here), exploring why markets haven’t rallied as much as might have been expected given the US-Iran deal and the slump in oil prices in the last two weeks.Speaking of the Iran war, there were fresh signs of progress in the negotiations, with Vice President JD Vance saying that the weekend talks were “very, very good”. That follows comments from the Iranian side, who had previously said in the small hours of Monday that there’d been major progress to end the war in Lebanon. Moreover, the US issued a 60-day sanctions waiver to allow Iran to sell its oil on the international market, which was seen as one of Tehran’s demands for implementing last week’s interim deal. So that backdrop saw oil prices come down, with Brent crude (-3.31%) closing at a 3-month low of $77.90/bbl, whilst WTI (-2.32%) also fell to $74.82/bbl.Turning back to Europe, ahead of this morning's flash PMIs, ECB President Lagarde said yesterday that she saw no more need for the ECB to have a “forceful response” to the Iran War. In comments to lawmakers, Lagarde said she saw inflation returning to target over the medium term, saying that the ECB saw “no evidence yet of de-anchoring of inflation expectations or second-round effects” that warrants a “more forceful policy response at this stage.” This contrasted with some of the more hawkish messaging from the ECB last week, which saw markets dial up their conviction of further tightening this year.Those comments supported a rally in European government bonds, with yields on 10yr bunds (-3.4bps), OATs (-3.4bps) and BTPs (-4.3bps) all coming down. And there were larger declines at the front-end, with the 2yr German yield down -4.4bps as investors dialled back the likelihood of aggressive ECB rate cuts this year. Indeed, markets were pricing 32bps of ECB hikes by the December meeting at the close, down -4.5bps on the previous day. Otherwise, equities also rose, with the STOXX 600 (+0.58%) making a fresh gain, while the DAX (+0.62%) also rose. The CAC (-0.25%) struggled again and has been struggling this year largely due to its outsized luxury stocks weighting. To the day ahead now, we’ll get June flash PMIs for the US, UK, Eurozone, Germany, and France. We'll also see US June Philadelphia Fed non-manufacturing activity, Richmond Fed manufacturing index, business conditions, France June business confidence and May retail sales. Earnings include FedEx and Carnival.

Futures Slide As Tech Tumbles, Korea Crashes

“Some of the recent performance in stocks has been highly speculative, fueled by a passion from retail investors for short-term gains. We may not like it this morning, but actually it’s healthy behavior."

6,060 words~28 min read