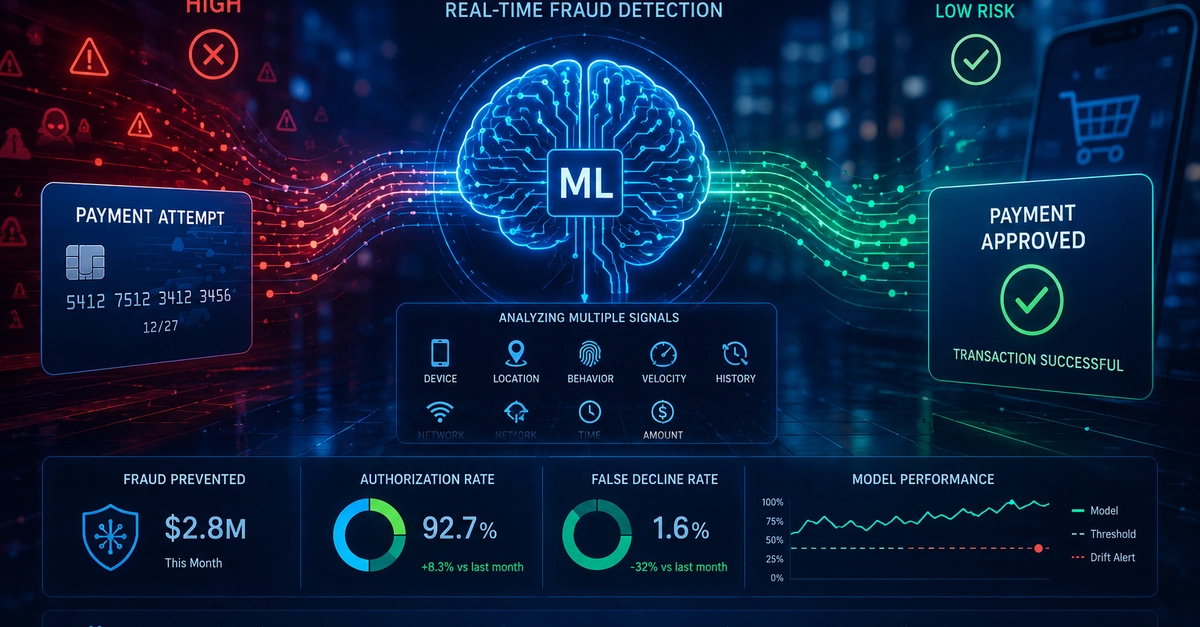

Machine learning has quietly become the default tool for payment fraud detection, and the reason is a trade-off every fraud team knows too well. Tighten the rules and you block more fraud, but you also block real customers who just wanted to buy something. Loosen the rules and conversion improves, right up until losses start eating the margin. Push too far in either direction and someone in a leadership meeting is going to ask hard questions.

For a long time, the lever for managing this was static rules. Block transactions over a certain amount from a certain region. Flag anything that looks unusual. Rules are easy to understand, which is their charm, and rigid, which is their curse. A rule cannot tell the difference between a genuine customer behaving slightly differently and an actual fraudster. It just sees a threshold and reacts. The result is a pile of false positives, which is a polite way of saying you annoyed your best customers.

And that is not a soft cost. Industry analyses have repeatedly found that the revenue lost to false declines runs at well over ten times the value of the fraud actually stopped, and roughly a third of wrongly declined shoppers never come back to that merchant. A blunt rule does not just leak money on the fraud side. It quietly bleeds it on the conversion side too.