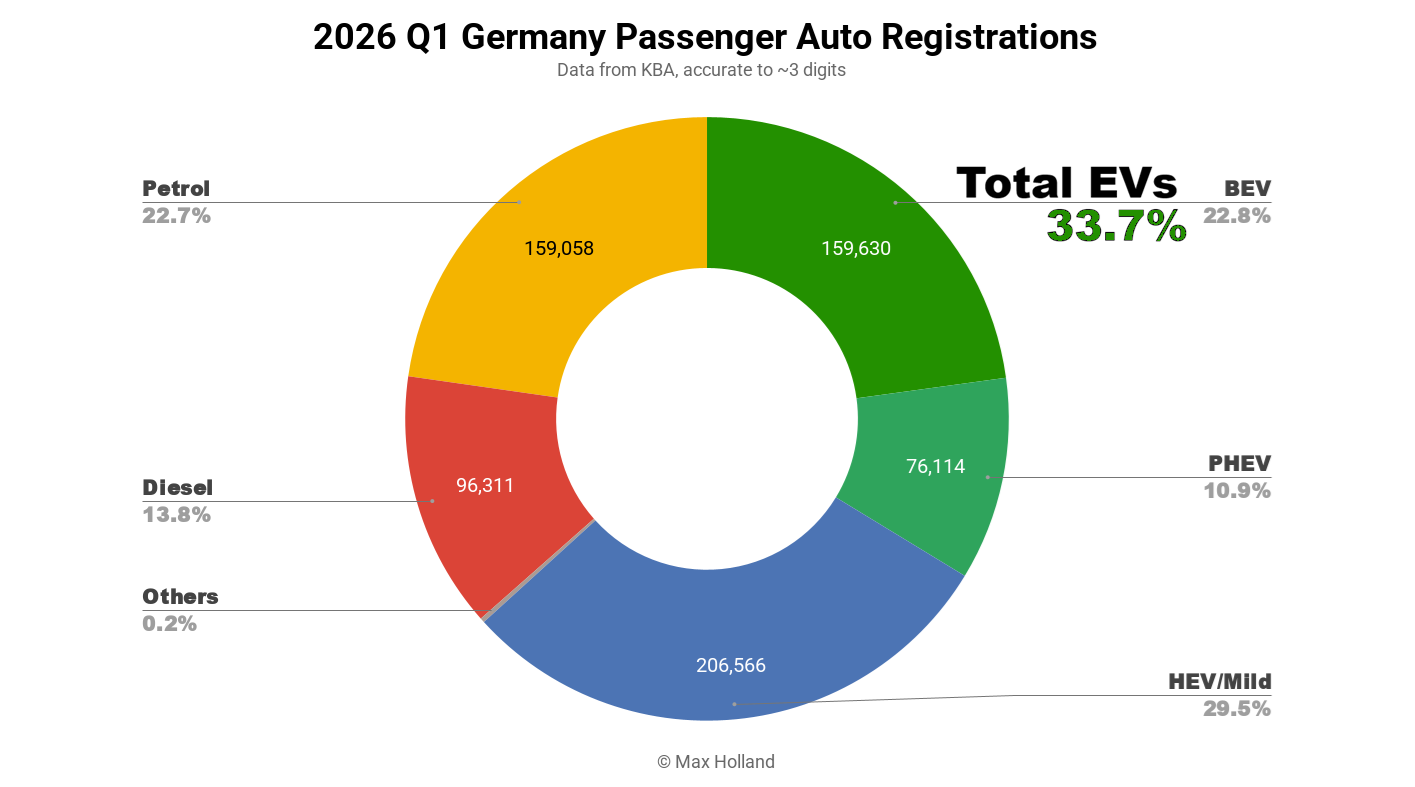

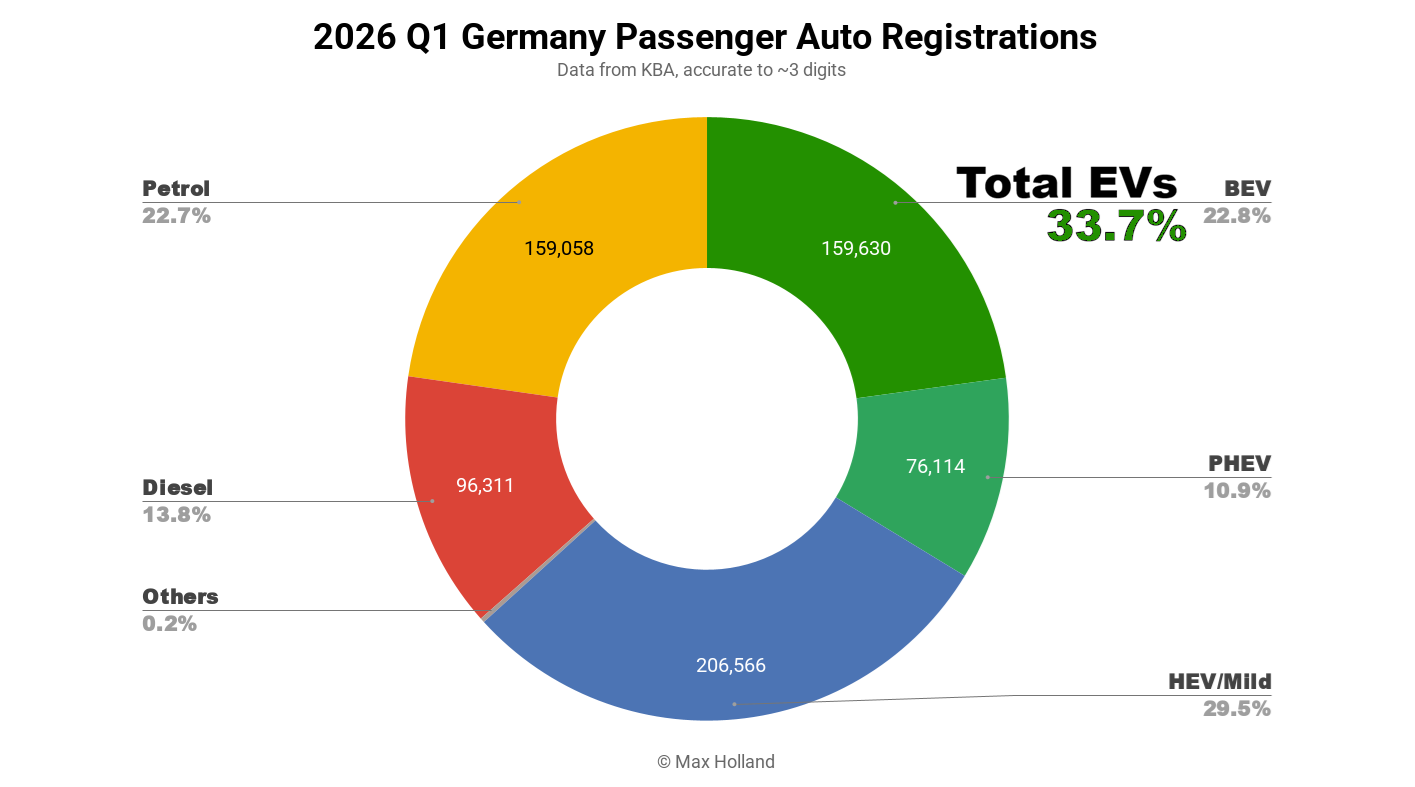

The first quarter of 2026 saw plugin EVs at 33.7% share in Germany, up from 26.6% in Q1 2025. BEV share grew strongly year on year, and PHEV share grew modestly. Overall, Q1 auto volume was 699,377 units, up some 5% YoY. The Skoda Elroq was the best-selling BEV in Q1.

2026 Q1 auto sales saw combined plugin EVs at 33.7% share in Germany, with full electrics (BEVs) at 22.8% and plugin hybrids (PHEVs) at 10.9%. These figures compare YoY against 26.6% combined, 17.0% BEVs and 9.6% PHEVs.

This is the best ever start to a year in terms of BEV share in Germany, with the previous best being Q1 2025 with 17% share. This has been helped by the reintroduction of purchase incentives, with 3.000 € for BEVs and 1.500 € for PHEVs (with additional incentives for lower income families).

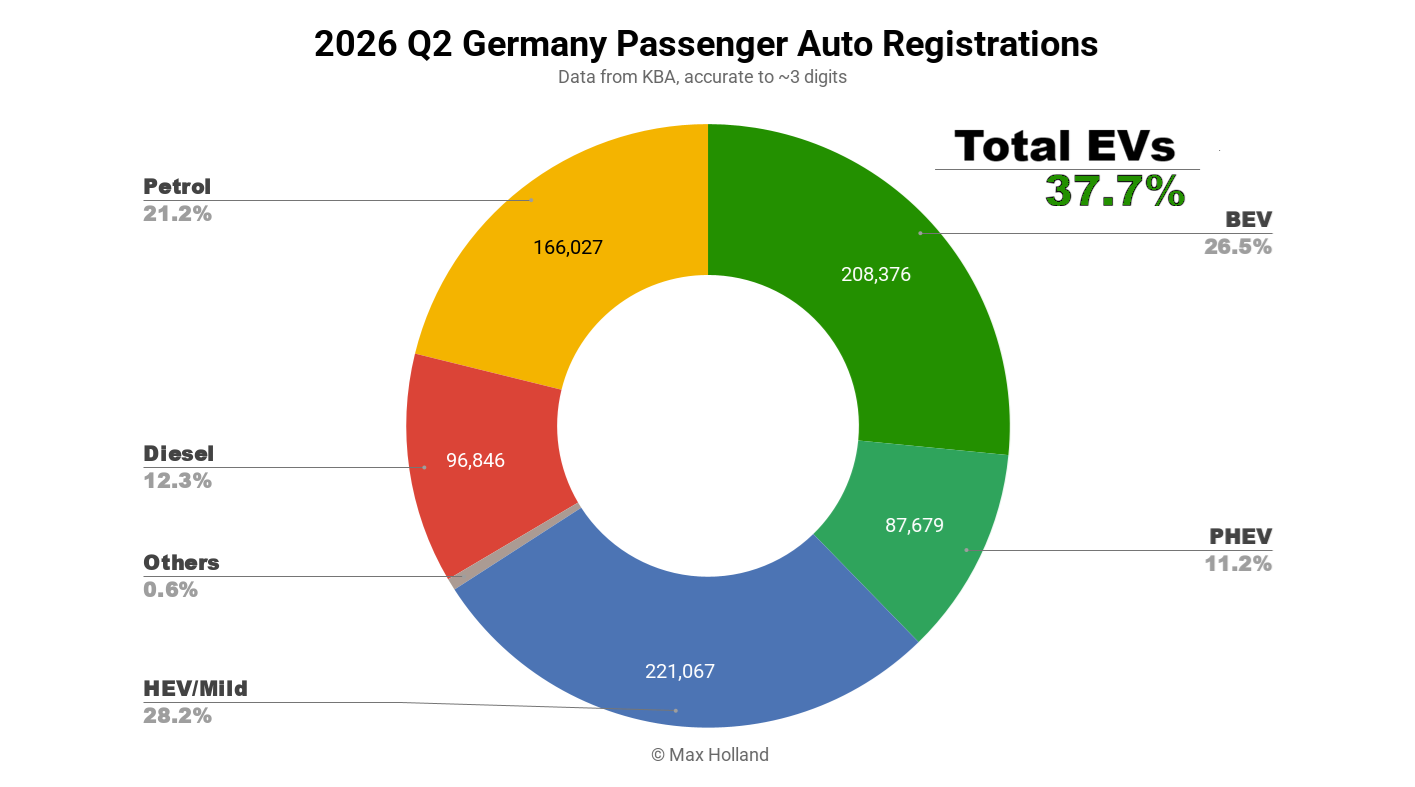

Prior to 2025, the start of each year was always a drop from the previous year’s Q4 peak, but since the 2024-2025 period, the peaks and troughs have smoothed out (see graph below). Growth in BEV share has been more steady (and less “roller-coaster”) ever since. This steady climb should remain the trend throughout 2026, now that incentives are back on the table.

As well as the growth in plugins, combustion-only powertrains are also being squeezed by growth in HEV and Mild-HEV powertrains. Remember that the latter are – at this stage of the transition – a cheap-and-easy way for legacy manufacturers to improve their fleet emissions. But they are also a “quick fix” – only a temporary interim technology, which will give way to plugins, and ultimately to BEVs, as we have seen in Norway, China, and other advanced markets.