Benzinga examined the prospects for many investors’ favorite stocks over the last week — here’s a look at some of our top stories.

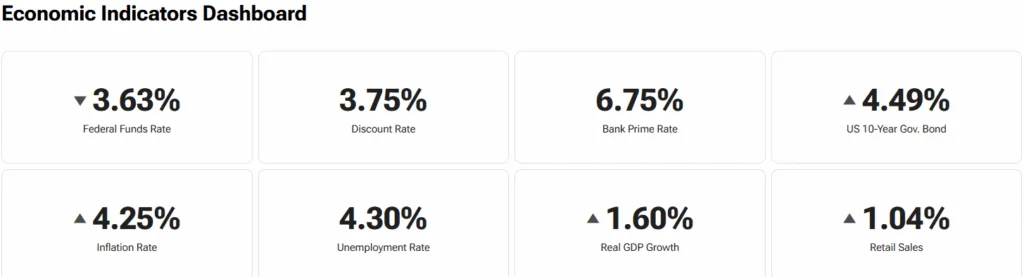

U.S. stocks ended the week with heightened volatility as investors grappled with shifting Federal Reserve expectations, persistent inflation concerns, and uneven economic signals. Major indexes including the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite moved lower over the week after an initially steady start, as stronger-than-expected inflation readings and hawkish Fed commentary under new leadership reinforced fears that interest rates may remain elevated longer than previously expected.

Technology stocks, which had been the primary driver of gains earlier in the year, came under renewed pressure as rising Treasury yields weighed on valuations and prompted a rotation out of high-growth sectors. Semiconductor and software names saw the most pronounced swings, contributing to broader market softness as investors questioned whether AI-driven earnings momentum could continue to offset tighter financial conditions.

Bond markets played a key role in shaping sentiment, with yields trending higher as expectations for near-term rate cuts faded and the possibility of additional Fed tightening came back into focus. Despite pockets of resilience in select industrial and consumer names, the overall tone remained cautious, with investors increasingly focused on incoming inflation data and central bank guidance. The week underscored a fragile balance between still-solid economic growth and tightening financial conditions, leaving markets sensitive to any new macro or policy surprises.