The Quest Begins (The "Why")

Picture this: I’m sitting at my desk, coffee gone cold, staring at a spreadsheet that looks like something out of Indiana Jones and the Last Crusade – a maze of dates, prices, and a gut feeling that I’ve cracked the code to beat the market. I had a shiny new idea: buy when the 50‑day moving average crosses above the 200‑day (the classic “golden cross”) and sell when it crosses below. Sounds simple, right?

I threw the logic into a quick Python script, ran it on a year of AAPL data, and—boom—my P&L chart looked like a rocket ship. I felt like Neo in The Matrix when he finally sees the code. “I know kung fu,” I whispered to my monitor.

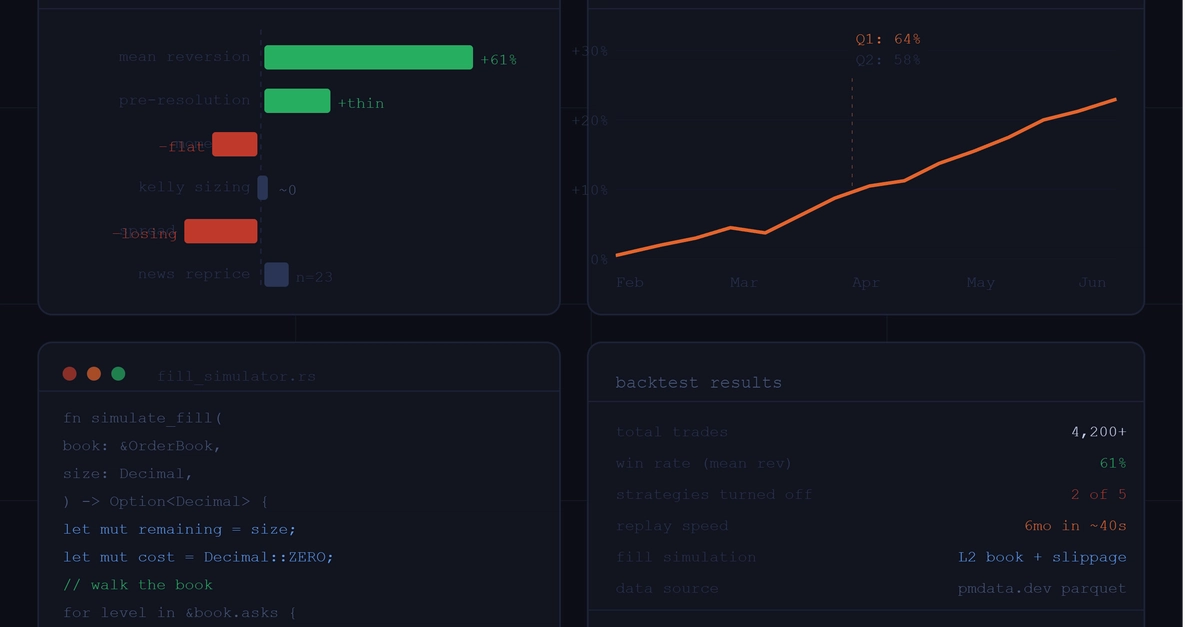

Then reality slapped me like a boss fight in Dark Souls. The results were too good to be true. I’d somehow managed to look into the future, ignore transaction costs, and pretend my strategy could trade fractions of a share without slippage. My excitement turned into a cold sweat. If I couldn’t trust the backtest, how could I ever trust the strategy live?

That’s when I realized I needed a proper quest: build a backtesting framework that’s honest, reproducible, and close to what you’d see in a live account.