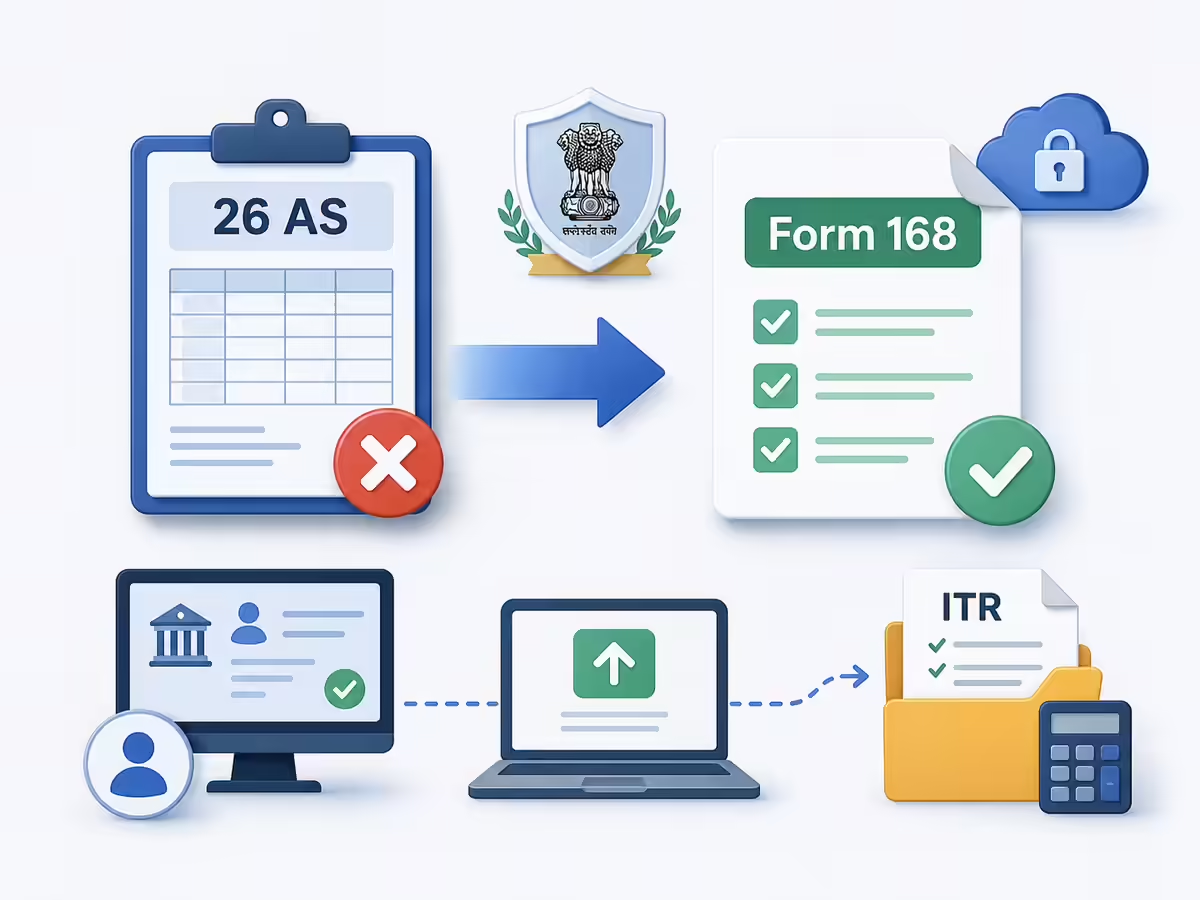

The Income Tax (I-T) Department has introduced Form 168, a new version of the Annual Information Statement (AIS) form, under the Income-tax Rules, 2026. This has left many taxpayers wondering whether Form 168 has replaced the traditional Form 26AS.Form 168 is designed to be a much more comprehensive statement compared to Form 26AS. It brings together information on taxes paid, income reported by various entities, specified financial transactions, refunds, demands and even details of tax proceedings.What is Form 168?Form 168 is a comprehensive annual tax information statement reflecting all tax-related and specified financial transactions linked to a taxpayer’s PAN. It enables taxpayers and the I-T Department to verify taxes paid, income sources and compliance history. Form 168 contains details relating to:Tax Deducted at Source (TDS)Tax Collected at Source (TCS)Advance tax, self-assessment tax and regular tax paymentsSpecified Financial Transactions (SFTs)Refunds and outstanding tax demandsPending and completed proceedingsOther information prescribed under Rule 245 of the Income-tax Rules, 2026Who should file Form 168?Form 168 is auto generated by the Income Tax Department.It is uploaded in the registered e-filing account of the taxpayer by:Principal Director General of Income-tax (Systems)Director General of Income-tax (Systems)Or any authorised person designated by them Taxpayers do not file Form 168 manuallySo, what happened to Form 26AS?Form 168 now formalises this expanded framework under the new Income-tax Rules, 2026. In effect, it serves as the new comprehensive annual information statement and incorporates much more information than the traditional Form 26AS.Structure of Form 168Part A –Particulars of the personName (full, no abbreviations) 2. Date of birth / incorporation 3. Address (flat/door/block, premises, road/street/lane, area/locality, town/city/district, state, PIN) 4. PAN 5. Email ID 6. Contact number (country code + number; multiple numbers allowed)Part B--Nature of Information Information relating to tax deducted or collected at source (TDS/TCS) Information relating to specified financial transactions (SFT)Information relating to payment of taxes (advance, self-assessment, regular)Information relating to demand and refundInformation relating to pending proceedingsInformation relating to completed proceedingsAny other information under sub-rule (2) of Rule 245, 2026.Does Form 168 need to be filed by taxpayers and how often is it updated?Form 168 is not filed by a taxpayer. Instead, it is an automatically created annual tax statement provided by the Income Tax Department based on data submitted by various deductors, collectors and reporting businesses. Form 168’s availability is contingent on the periodic submission of TDS/TCS returns, SFT statements, and other statutory reports by these organisations.Therefore, Form 168 does not have a filing frequency of its own; it is updated dynamically throughout the year as and when the underlying statements are filed and processed by the Department.What are the sources of information used to prepare Form 168?Form 168 is compiled using information received from multiple sources. These include:1. TDS/TCS data: Submitted by deductors/collectors through quarterly returns (Forms 24Q, 26Q, 27Q, etc.)2. Tax payment details: From challans (OLTAS/online payments)3. SFT information: From banks, mutual funds, registrars and other reporting entities4. Refund/demand data: From CPC-ITR module5. Proceedings information: From assessment units / faceless assessment centres

Has Form 168 replaced Form 26AS for FY 25-26? Here's what taxpayers need to know for ITR filing - The Economic Times

Form 168: The Income Tax Department has unveiled Form 168, a comprehensive upgrade to the Annual Information Statement, effectively superseding the traditional Form 26AS. This new form consolidates all tax-related and financial transaction data linked to your PAN, offering a holistic view of your tax compliance. It's automatically generated, so taxpayers don't need to file it.

TL;DRAI

Form 168 automatically consolidates Indian tax data (TDS/TCS, payments, transactions, refunds), replacing Form 26AS. Automated compliance reduces overhead for multinationals in India, exemplifying trend toward digital governance and platform-driven reporting.

496 words~2 min read