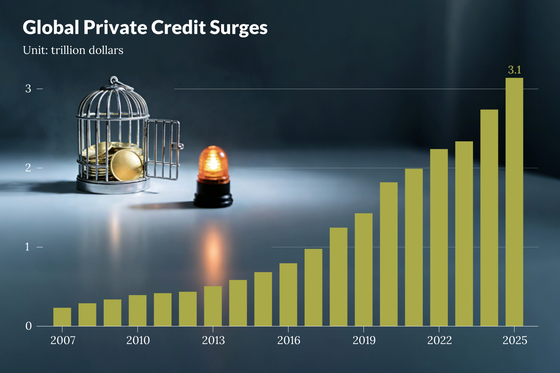

1. The $3.1 trillion private credit market, originally promoted as a high-yield alternative to bank lending, is now facing liquidity squeezes and high-profile collapses, revealing deeper systemic risks due to the lack of bank-like oversight [para. 1]. The market's vulnerabilities—illiquidity, hidden leverage, and opaque valuations—closely resemble China’s shadow banking era, which Beijing dismantled beginning in 2018. Western markets are now confronting similar systemic dangers [para. 2]. A chart illustrates the rapid growth of global private credit, reaching $3.1 trillion by 2025 [para. 3].2. A primary threat is a glaring valuation mismatch between publicly traded business development companies (BDCs) and private credit funds [para. 4]. While both hold similar loan portfolios, BDC shares on the New York Stock Exchange traded at discounts of 20% to 35% to net asset value (NAV) earlier this year, whereas private funds continued to process redemptions at NAV [para. 5]. This divergence triggered an arbitrage loop, with investors rushing to cash out of private funds at par value to buy discounted BDC assets, straining liquidity in some funds [para. 6].3. In response to mounting redemption pressure, U.S. giant Blue Owl Capital limited redemptions on one private credit fund and executed an urgent $1.4 billion fire sale of debt assets, a sequence that evoked parallels to the early liquidity crunches of the 2007 financial crisis [para. 7].4. Compounding the structural flaw is severe concentration risk [para. 8]. Private credit leans heavily on software companies, with some managers allocating up to 40% of portfolios to the sector. The rapid advancement of artificial intelligence (AI) threatens to disrupt these borrowers' asset-light, recurring-revenue models. If AI deployment impairs cash flows, default rates could spike, turning a perceived safe haven into a distress epicenter [para. 9].5. Recent collapses point to underlying governance risks [para. 10]. The downfalls of U.S. subprime auto lender Tricolor Holdings LLC and U.K. mortgage lender Market Financial Solutions Ltd. centered on fraud or collateral double-pledging allegations. Hedge fund Rubric Capital accused some private credit managers of using accounting maneuvers to mask leverage. In a market lacking standardized public auditing, such incidents rapidly erode trust [para. 11].6. Industry proponents argue that shifting risk from regulated banks to private capital reduces broader systemic threats [para. 12]. However, regulators are increasingly wary. The U.S. Securities and Exchange Commission and the Bank of England have flagged risks. After the European Union required member states to implement strict new rules for private credit by April, the era of fragmented regulation in the bloc has effectively ended [para. 13].AI generated, for reference only

Analysis: Cracks in the $3 Trillion Private Credit Market Expose Shadow Banking Risks

Mounting redemption pressures, valuation lags and governance deficits are testing the resilience of a famously opaque asset class

420 words~2 min read