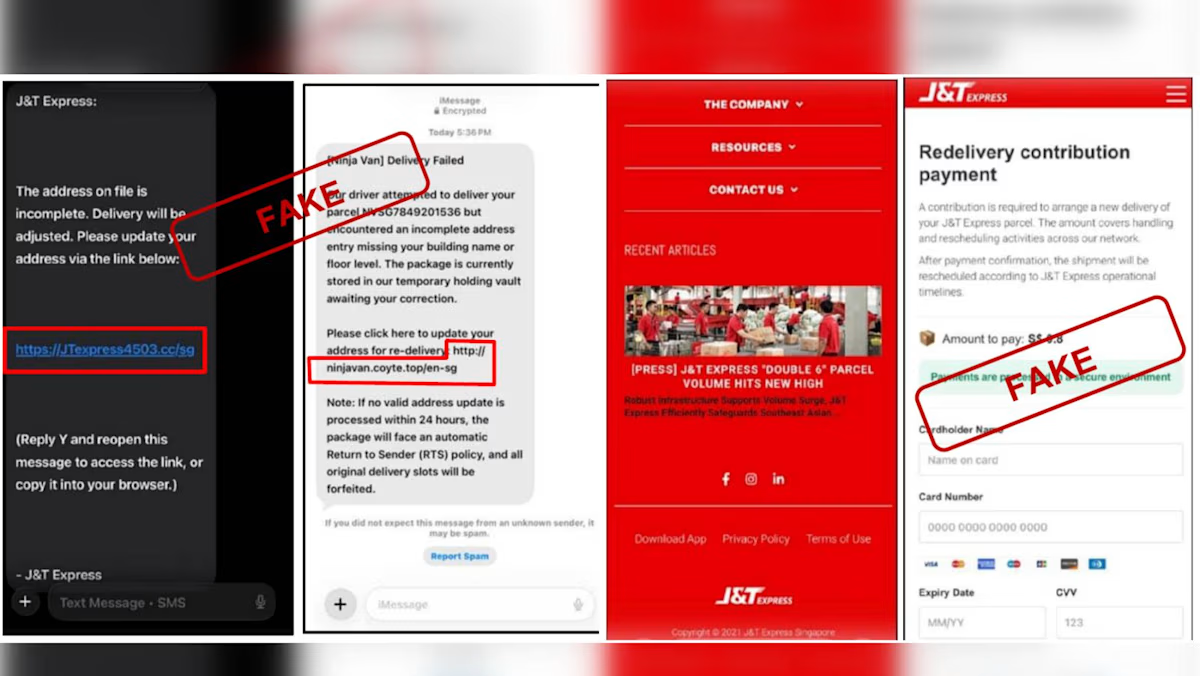

SINGAPORE – It was a Friday in February 2025. June (not her real name), a communications professional in her 30s, was working in the office when she received a call at around 11am from a man claiming to be a Citibank representative.June said the caller told her the bank had detected fraudulent activity on her Citibank credit card.As she had experienced credit card fraud before and was quite preoccupied with work, she did not think further and “trusted her caller completely”.She was then connected to a “police officer” as well as a “representative from the Monetary Authority of Singapore (MAS)”, who both told her she was a suspect in a money laundering case.“They said I had to appear in court. Then they told me that because of this court order, they needed to freeze my assets and that I couldn’t go to work. So I needed to tell my employer,” she said.“At that point, I was already very stressed.”She also felt a pressing need to act fast to protect her money. “That sense of urgency lowers your ability to take a step back to think whether this even makes sense,” she added.June was instructed to protect her assets by transferring at least 80 per cent of her money into a new account with digital bank GXS Bank for safe-holding.So she moved about half of that amount from her DBS Bank account, and was about to transfer the rest when DBS called to stop her. All that transpired over a space of three to four hours.In hindsight, June realised she had fallen for a government officials impersonation scam. The red flags were there – the scammers reached out to her on WhatsApp, she had a video call with an “MAS representative” and a “police officer” – but it did not occur to June at that point that she was being scammed.“It is super ridiculous when I look back now, but at that moment, I did not question anything at all,” she said.According to the annual scam and cybercrime brief from the Singapore Police Force (SPF), the number of government officials impersonation scams more than doubled to 3,363 cases in 2025 from 1,504 cases in 2024.The amounts lost due to this scam type increased by 60.5 per cent to about $243 million, the second-highest among all scam types in 2025.SPF noted that the majority, or 81.8 per cent, of all reported scams involved self-effected transfers, where victims were manipulated into moving the funds of their own accord.DBS is observing this trend among its customers. Yin Juon Qiang, its head of group investigations and fraud advisory, said scammers play psychological mind games to trick victims into transferring money.Tan Xue Ying, a behavioural scientist at the bank, noted that scammers do so by exploiting human emotions and behavioural biases, such as fear, urgency, trust and reciprocity.She added that victims may then be pressured into acting quickly to avoid supposed legal consequences or financial losses, or for fear of missing out on an opportunity.“Under these conditions, people tend to be in a ‘hot state’ and rely on instinctive or emotional decision-making rather than pause to evaluate the situation rationally,” she said.This also explains why scam awareness is not enough. Customers often do not believe they are being scammed, particularly when the scammer spins them an emotionally compelling tale, Tan added. Naveen Gondhi, associate professor of finance at French business school INSEAD, said scammers target “System 1 thinking”, a concept from psychology that refers to the intuitive mode of thinking that the human brain relies on to make fast decisions.He added that consumers may want to consciously slow down and ask themselves if the situation makes sense.Singapore banks have implemented a 24-hour cooling period since Oct 15, 2025. Under this rule, if account holders try to transfer out more than half of their funds, their bank will automatically hold the transaction for 24 hours or reject it. The safeguard applies to bank accounts with balances of $50,000 or more. Bank customers thus have 24 hours to decide whether to proceed with the transfer.Gondhi noted that the cooling period is “a nice way to put the brakes on our thinking”.“You can still proceed with the transaction (after 24 hours) if you feel it is legitimate.” Beyond the industry-wide safeguards, banks have their own scam detection and control measures.DBS monitors millions of transactions daily, using artificial intelligence to analyse customer behaviour and transaction patterns to detect potential scams. When the system flags suspicious activity, the bank intervenes on these transactions, instead of disrupting everyday banking activities. Such interventions include customised notifications and warning messages, as well as step-up authentication methods like digital token authentication and Singpass facial verification.The notifications are regularly updated to make them more effective at stopping scams.Tan noted that DBS’ behavioural science team collaborates with fraud, product and customer journey teams to understand how scammers exploit human biases and vulnerabilities.This allows them to design more effective “cognitive breaks” that prompt customers to pause and think. The efforts appear to be bearing fruit. Yin said DBS managed to avert 35 per cent more scam-related losses in 2025 compared with the year before. June was one of the bank’s relieved customers. While her first fund transfer to GXS went through, she managed to freeze the account in time so the scammers could not touch the money. “It was quite a big amount actually,” she said.The second transfer was blocked after a bank staff became suspicious and called her to verify the transaction.June said: “If the DBS representative did not call me and I did not tell anybody, I would probably still have transferred the money after the cooling period ended.“The call helped to shock me back to reality.”She feels that having a neutral third party intervene is useful because, in her case, the DBS staff pointed out the flaws in the scammer’s story that June had been too caught up in to see.Such a third party could also be a family member, friend or trusted adviser.Kim Dayoung, senior lecturer from the marketing department at NUS Business School, said people are more conscious of their decisions when they know that someone is watching their behaviour.She added that it therefore helps to involve a trusted contact in major transaction decisions.“It is not about taking away the individual’s autonomy to make decisions, but about ensuring that any decision is not made entirely alone,” she said.She noted that the mere option to add a trusted contact serves as a “psychological nudge” to prompt individuals to think twice about their actions, regardless of whether they ultimately involve that person in their decision-making.While regulators and financial institutions are pulling out all the stops to fight scams, scammers are adapting and evolving their tactics.Michael Meadon, head of the Asia-Pacific region at London Stock Exchange Group Risk Intelligence, said scams are an arms race between financial institutions, regulators and the bad guys.While public focus typically lands on the scam victims and the money they lost, he said that the emotional trauma, like embarrassment, fear and anger, is often neglected.Furthermore, the damage extends beyond individual victims. Meadon said scammers are “parasitic on pro-social behaviours”.“We want a society where we trust one another and where people follow instructions from, say, a law enforcement officer.”However, by impersonating officials, scammers erode this trust and tear away at the social fabric, he added.

How scammers exploit fear and urgency to target victims

Discover how scammers use emotional manipulation to exploit victims in financial scams, and learn about safeguards against these growing threats. Read more at straitstimes.com. Read more at straitstimes.com.

1,223 words~6 min read