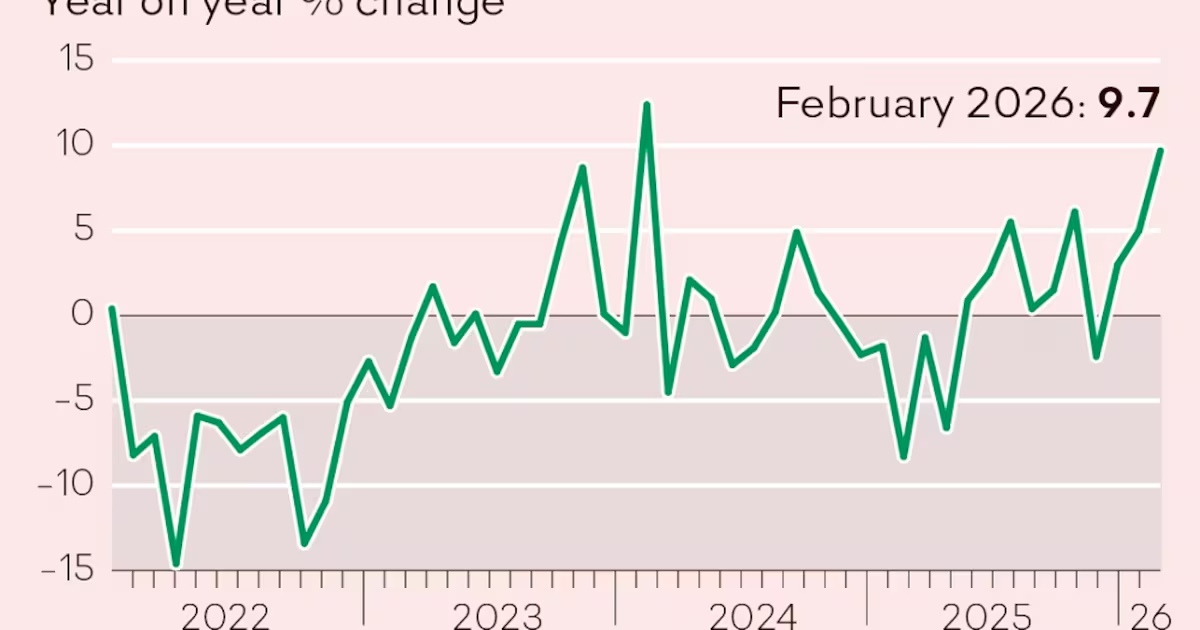

The Minerals Council’s assessment of the mining sector in the first quarter of 2026 presents a complex and in many respects paradoxical narrative. On the one hand the sector exhibited measurable signs of recovery, underpinned by robust commodity prices, export demand and selective production gains. On the other, entrenched structural constraints underpinned by uneven domestic demand and commodity-specific declines continued to delimit the pace and sustainability of that recovery. This duality underscores the fragility of South Africa’s mining economy, even in periods of favourable global market conditions. At the aggregate level, South Africa’s mining production recorded a modest expansion in early 2026. Output rose by 2.5% year on year in March, though this was a marked deceleration from January (4.6%) and February (9.7%). The moderation suggests that while cyclical recovery forces remained operative, they were increasingly offset by emerging headwinds. This subdued growth trajectory reflects both base effects and sector-specific divergences. Importantly, it highlights that South Africa’s mining sector remains highly sensitive to both domestic constraints and exogenous shocks, including geopolitical uncertainty and global commodity cycles. The limited expansion in output contrasts sharply with the more pronounced increase in mineral sales, illustrating a growing decoupling between physical production and revenue generation. A close analysis reveals stark heterogeneity across commodity classes, with platinum group metals (PGMs), gold and manganese driving growth. PGMs emerged as the most significant contributor to production growth, expanding by 10.5% year on year and contributing 2.6 percentage points to overall output. This performance was facilitated by operational stabilisation and recovering demand for internal combustion engine vehicles, which rely on catalytic converters. Gold production exhibited even stronger growth, rising by 17.1% year on year, buoyed by heightened geopolitical uncertainty that reinforced gold’s traditional role as a safe-haven asset. This reflects broader global macroeconomic dynamics, including financial market volatility and persistent geopolitical tensions, which have elevated investor demand for bullion. Manganese production also expanded robustly, increasing by 14.4% year on year, largely driven by surging Chinese demand. Notably, China’s manganese ore imports increased significantly, with South Africa’s exports rising from 1.4-million tonnes to 2.2-million tonnes year on year. This underscores the centrality of China as a demand anchor for South Africa’s bulk commodities, reinforcing structural export dependencies. Collectively, these three commodities accounted for 43.2% of total mining production, indicating a relatively concentrated base of growth drivers. In contrast, several key commodities experienced contraction. Coal production declined by 9.6% year on year, marking the sixth consecutive monthly decrease. This downturn is attributed primarily to weakened domestic demand, which constitutes more than two thirds of total coal consumption. Though exports increased by 9.8%, this was insufficient to offset the domestic shortfall. Iron ore output also contracted, decreasing by 2.7% year on year. The persistence of such production declines, despite strong export growth, reveals structural vulnerabilities in domestic industrial linkages. Equally, diamond production decreased by 8.5% year on year, reflecting sectoral pressures. The diamond industry faces deeper structural challenges, potentially including subdued global demand, the competitiveness of lab-grown diamonds, and overall price volatility. Together these declining industries represent 44.8% of the production basket, effectively offsetting gains elsewhere and contributing to the overall subdued growth profile. In contrast to modest production growth, the mining sector experienced an increase in revenue. Year-to-date mineral sales reached R242bn, a 39% increase (R67.4bn) compared to the same period in 2025. This surge was overwhelmingly price-driven. PGMs and gold were the principal contributors, with sales increasing by 113.5% and 51.7% respectively. These gains were underpinned by substantial increases in global commodity prices: platinum: +109.6%; rhodium: +105.7%; palladium: +62.4%, and gold: +62.8%. Such price escalations reflect a confluence of factors, including supply constraints, geopolitical uncertainty and shifting industrial demand patterns. The divergence between production and revenue growth highlights the extent to which the mining sector’s current resilience is contingent on favourable price regimes rather than underlying output expansion. While favourable commodity prices and selective production gains have supported a modest recovery, underlying structural constraints continue to inhibit sustained growth. Notwithstanding the revenue windfall, the sector faces escalating cost pressures that threaten to erode profitability and investment potential. Chief among these is the sharp increase in fuel costs. According to the Minerals Council, average monthly fuel expenditure rose from R2.9bn in 2025 to about R4bn by April this year. This increase is attributed to geopolitical tensions in the Middle East, which have driven up global oil prices. Rising fuel costs have a pervasive impact on mining operations, affecting transportation, energy-intensive extraction processes and overall cost structures. As such, they constitute what the Minerals Council identifies as the most significant operational risk facing the sector. The persistence of such cost pressures could negate the benefits of elevated commodity prices, particularly if prices stabilise or decline in subsequent quarters. Moreover, it underscores the vulnerability of SA’s mining sector to external shocks, given its reliance on imported fuel. A recurring theme in the Minerals Council’s assessment is the weakness of domestic demand, particularly for coal and iron ore. The decline in coal production despite rising exports illustrates the critical importance of domestic consumption in sustaining output levels. This structural dependency reflects broader challenges within South Africa’s industrial economy, including sluggish growth in energy-intensive sectors and ongoing constraints in electricity generation and infrastructure. Addressing these structural issues is essential towards achieving sustained growth in mining output. Without a robust domestic industrial base, the mining sector remains overly reliant on volatile export markets. Despite these challenges, the Minerals Council emphasises the sector’s significant potential to drive inclusive economic growth. The substantial increase in mineral sales demonstrates the capacity of the mining industry to generate revenue, employment and foreign exchange earnings. However, realising this potential requires a supportive policy and regulatory environment focusing on at least four areas: Enhancing regulatory certainty to encourage investment; Addressing infrastructure bottlenecks, particularly in rail and ports;Mitigating energy and fuel cost pressures; andStrengthening domestic industrial linkages. The council’s assessment implicitly aligns with a developmental state perspective, wherein strategic policy interventions are necessary to leverage natural resource endowments for broader economic transformation. In sum, the Minerals Council’s evaluation of SA’s mining sector in the first quarter of 2026 reveals a sector at a critical juncture. While favourable commodity prices and selective production gains have supported a modest recovery, underlying structural constraints continue to inhibit sustained growth. The pronounced divergence between production and revenue underscores the precariousness of this recovery, as it remains heavily dependent on exogenous price dynamics. At the same time, rising operational costs, particularly fuel, pose a significant threat to profitability and competitiveness. Looking ahead, the trajectory of the sector will depend on its ability to navigate challenges while capitalising on its inherent strengths. With appropriate policy support and structural reforms, the mining industry retains the potential to serve as a cornerstone of South Africa’s economic development. Absent such interventions, however, the sector risks remaining trapped in a cycle of low growth and high vulnerability, despite intermittent periods of price-driven prosperity. Dr Tshitereke, an honorary professor at Unisa’s Thabo Mbeki School of Public & International Affairs, is Chief of Staff at the Minerals & Petroleum Resources Ministry.

CLARENCE TSHITEREKE | Nuanced SA mining recovery amid structural constraints

Platinum, gold and manganese buoy sector amid coal and iron ore slumps

1,177 words~5 min read