Home

Money & Banking

Competition to intensify for NRI deposits

The Reserve Bank of India (RBI) logo is pictured outside its head office in Mumbai

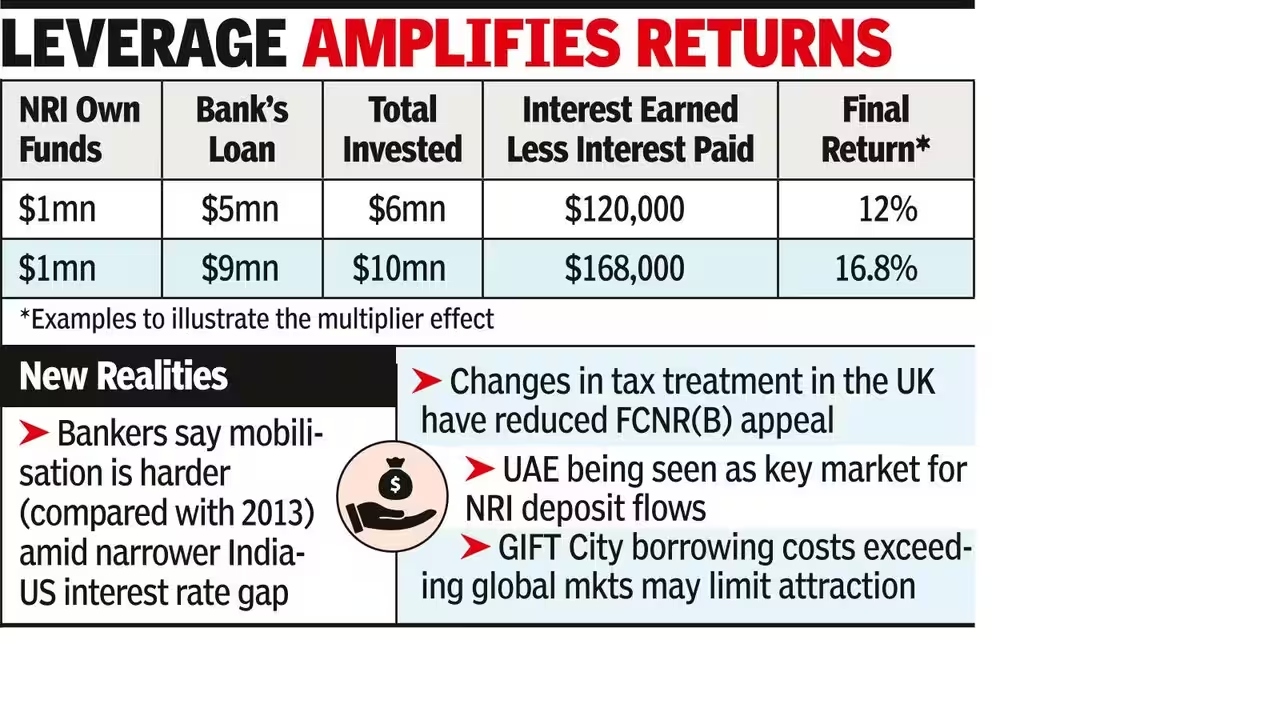

About $55-65 billion is expected to flow into the country due to the RBI move to bear the full hedging cost of banks for raising fresh 3- 5-year FCNR (B) deposits and providing a concessional forex swap facility to incentivise ECBs by PSUs, according to estimates by State Bank of India’s economic research department (ERD).The effect of the aforementioned measures could be that the rupee could strengthen to about 92/dollar; the overall balance of payment would be in the range of $5 to $10 billion surplus for FY27 (way above ERD’s previous estimate of $65-70 billion deficit); and bank deposit growth could jump to 14.5 per cent, with the credit-deposit gap in FY27 shrinking to less than 2 per cent from the peak of 6.7 per cent in FY24, per ERD economists in a report.The economists noted that the current FCNR (B) rate is 3.35 per cent (three years). At present, the cost of hedging, forward premium is 3.5 per cent. Current Card rate for a 3-year deposit is 6.3 per cent.“Thus, banks can offer attractive FCNR (B) pricing in the range of 5.5-6 per cent. This will be quite attractive even if we compare with current US yields at 4.20 per cent for three years. Additionally, the deployment of FCNR(B) funds can also be done at a rate lower than the prevailing 3 year MCLR (marginal cost of funds-based lending rate),” said Soumya Kanti Ghosh, Group Chief Economic Adviser, SBI.Ghosh said the interest rate gap (between the Indian government bond yields for 3-year tenure and the US three-year treasury yield) has narrowed down significantly, reducing the possibility of leverage this time. He assessed that in case of three years, the rate gap has now reduced to 2.1 per cent and for five year it has narrowed down to 2.2 per cent.SBI economists expect around $40-45 billion to come in through the FCNR (B) deposits route.They estimated that the ECB (external commercial borrowing)/OFCB (overseas foreign currency borrowing) swap window will support the rupee by encouraging fresh foreign currency borrowings and improving dollar supply. About $15-20 billion is expected to flow in through this route.The economists opined that the estimated $55-65 billion inflows will ensure that the deposit growth for FY27 for banking system could jump to around 14.5-15 per cent against a potential credit growth of 16 per cent.“This will mean that the credit deposit gap after adjusting for regulatory dispensation will shrink by around ₹1 lakh crore. This will ensure that the term structure of interest rates will decline further. It may be noted that in FY14 after the FCNR(B) fund mobilisation deposit and credit growth were almost identical,” they said.The economists observed that at this juncture, the RBI may continue to ensure that the rupee is not subject to excessive depreciation. In fact, the risks of allowing continued rupee weakness far outweigh the benefits of further currency flexibility.Therefore, the central bank should continue to adopt a more forceful and unambiguous intervention strategy to arrest any dramatic fall in rupee value as it happened on June 8. They cautioned that in the current environment, a passive approach could prove costly. A decisive RBI intervention would help anchor expectations, contain imported inflation, reduce pressure on the external account, and preserve macro-financial stability.NRI depositsV Rama Chandra Reddy, Head – Treasury, Karur Vysya Bank, observed that RBI’s latest FCNR(B) swap facility is a significant incentive for banks to mobilise long term NRI deposits. “By offering an at-par USD/INR swap for fresh FCNR(B) deposits of 3-5 years, the central bank is effectively absorbing nearly 280-300 basis points (bps) of annual swap cost, substantially improving the economics for banks,” he said.Adding to the attractiveness, the RBI has exempted eligible FCNR(B) deposits mobilised between June 8 and September 30 from CRR and SLR requirements. Reddy assessed that the CRR exemption alone provides a cost benefit of around 20 bps, while the SLR relaxation further enhances balance sheet efficiency.“Taken together, the swap concession and regulatory exemptions significantly lower the effective rupee cost of funds, enabling banks to offer more competitive FCNR(B) rates while remaining cost-effective. This is likely to intensify competition for NRI deposits, particularly in the 3-5 year maturity segment,” he said.Published on June 9, 2026