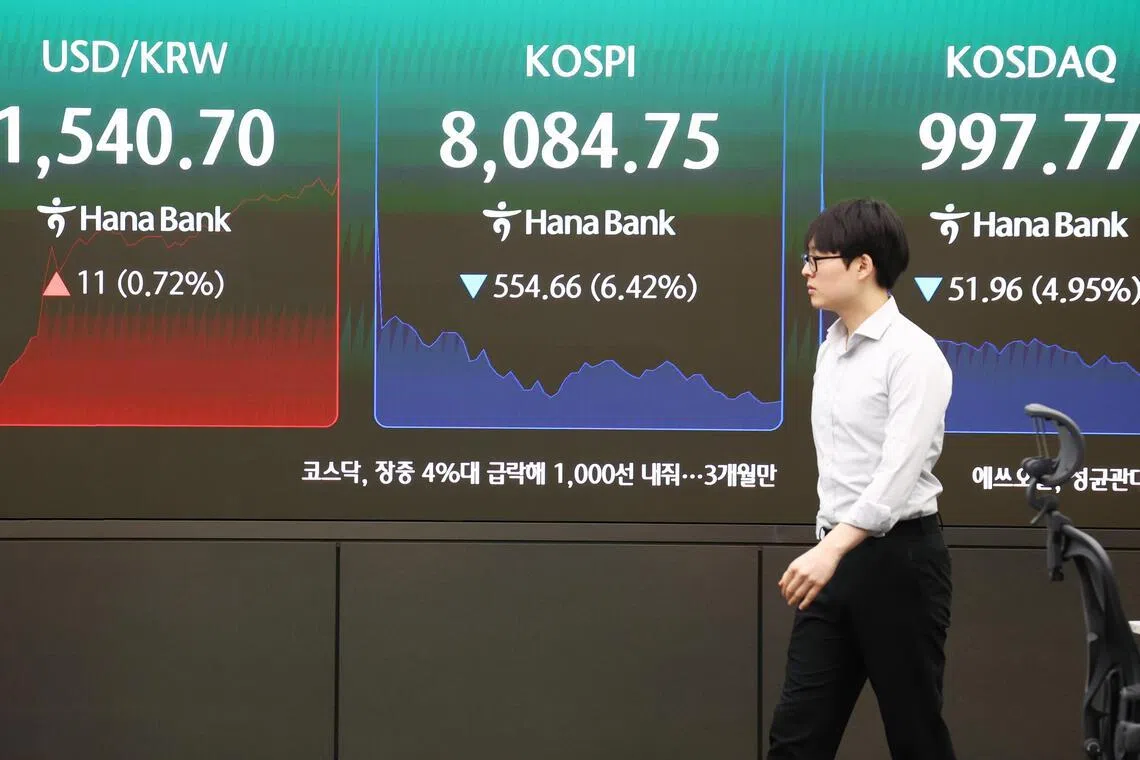

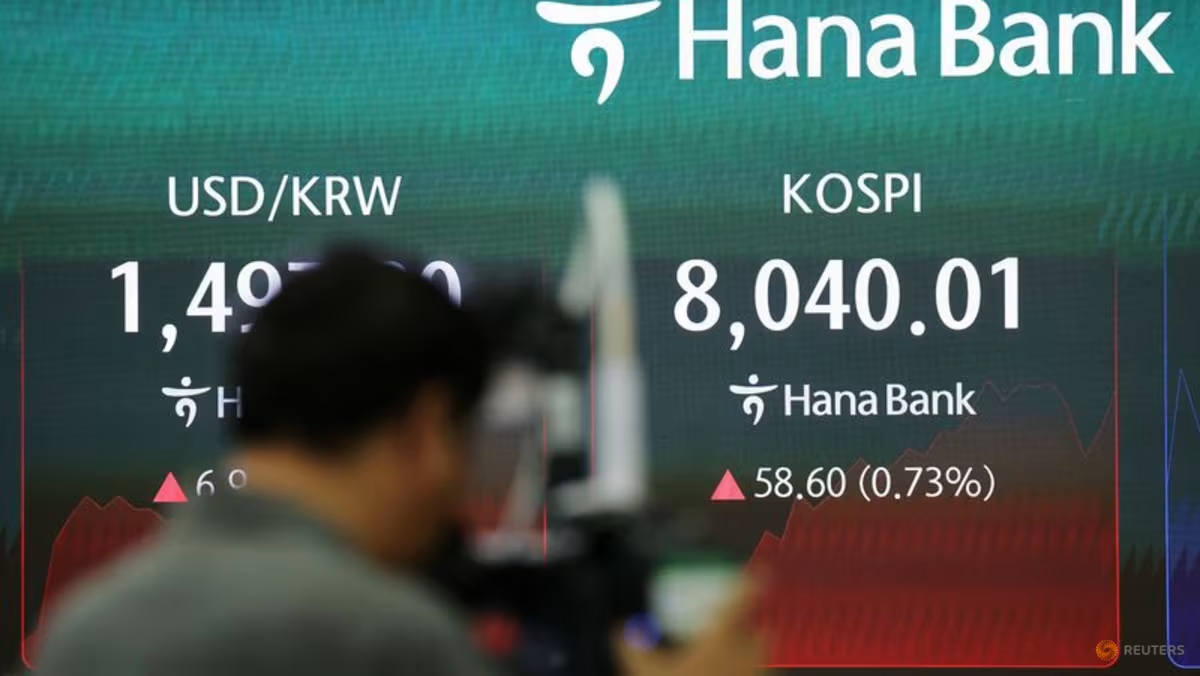

Futures are lower amid fresh underperformance of tech. If the premarket weakness persists, the S&P 500 is set to break a historic weekly run of gains as the AI trade takes another leg lower this time driven by the cartoonish Kospi index, with investors also expecting payrolls data to affirm that interest rates will stay higher for longer (full payrolls preview here). As of 8:00am ET, S&P futures are down 0.5% while Nasdaq futures slide 1% as chipmakers fall and big tech stocks are lower too, following on from a slump in South Korea’s Kospi. All Mag 7 names are all lower in premarket trading except for MSFT (+0.4%); NVDA fell -1.3%, a continuation of yesterday’s underperformance post AVGO earnings. On news flow, headlines were mostly muted this morning; after yesterday’s non-tech led rebound, we saw more negative sentiment this morning with all three indices lower during the pre-market session. Bond yields are flat to lower, the 10Y yield trading unchanged at 4.47% lower; the USD is also lower. WTI crude fell -0.2% to $92.86; both base and precious metals are lower while the bitcoin mauling shows no signs of ending. Today, the key focus is NFP; see our full preview here. In premarket trading, Mag 7 stocks are mostly lower (Nvidia -1.3%, Microsoft +0.4%, Tesla +0.1%, Apple -0.1%, Alphabet -0.4%, Amazon -0.2%, Meta -0.2%, Nvidia -1.3%)Argan (AGX) rises 11% after the power-plant construction company reported first-quarter revenue above what analysts expected.Chipotle (CMG) is up about 2% after JPMorgan upgraded to overweight, citing a “rare valuation opportunity” for the stock.Cooper Cos (COO) gains 6% after the lens maker posted second quarter sales and profit that topped estimates.Docusign Inc. (DOCU) is down 4% after the company provided an in-line forecast for second quarter revenue. Analysts notes that its still a wait-and-see story as the company ramps Intelligent Agreement Management, its AI-powered platform for contracts.G-III Apparel Group (GIII) rises 8% after the clothing company boosted its adjusted earnings per share guidance for the full year.Guidewire (GWRE) is down 12% after the midpoint of the software company’s subscription and support revenue forecast for the fourth quarter fell short of the average analyst estimate.Lululemon Athletica Inc. (LULU) slides 10% after the company lowered its annual forecast due to deteriorating performance in North America.Merlin Inc. (MRLN) soars 29% after the defense technology company announced the successful completion of the critical design review for its C-130J autonomy program with the US Special Operations Command.Samsara (IOT) slips 2% after the GPS fleet tracking company posted first-quarter results.ServiceTitan (TTAN) jumps 15% after the software solutions firm reported revenue for the first quarter that beat the average analyst estimate.Stocks are pulling back for a second day after Broadcom’s outlook for chip sales fell short of high expectations, raising questions over whether the rally in the AI trade had run too hard. The lack of progress toward a deal in the Middle East has also stoked worries that oil prices will remain elevated for some time. "Following a period of upward revisions to earnings expectations across the sector, investors are taking a more selective approach to new information and guidance updates,” said Tomás García-Purriños, senior asset allocation strategist at Santander Asset Management. “We would view the recent weakness primarily as profit-taking and consolidation after a strong run.”The chase for tech stocks took a further knock after S&P Dow Jones Indices said it would keep its eligibility criteria for benchmarks such as the S&P 500, rejecting proposals that would’ve allowed mega-caps to gain entry more quickly after going public. The decision means companies such as SpaceX, Anthropic PBC and OpenAI would have to wait at least a year for inclusion in the US benchmark after their debut. Fast inclusion in the S&P 500 would’ve led to about $14 billion in forced passive buying for SpaceX.Friday’s jobs data will likely show a solid increase in payroll numbers, up 88K (if down from 115K in April), suggesting the strong March and April reports reflected underlying momentum rather than just a rebound from earlier weakness, according to Bloomberg Economics. Our preview can be found here. The report may not offer strong direction for stock markets, as a focus on signs of price pressures is keeping investors to expect a rate hike as soon as December. Goldman noted that the implied move of 47 basis points is much lower than the average realized move over the past year, and the lowest since Dec 24. “Employment figures should not move the needle unless there is a major surprise,” said Roberto Scholtes, head of strategy at Singular Bank. “Instead, the key variables to watch are 10- and 30-year Treasury yields, which are hovering around the 4.5% and 5% ‘pain threshold’ levels.”Europe’s Stoxx 600 is brushing broader losses off and edging higher, as losses for tech stocks and miners are offset by gains for consumer names.Here are the biggest movers Friday:Raspberry Pi shares rise as much as 14%, extending their run and hitting a new all-time high after the British maker of small, low-cost computers said earnings this year will be well ahead of expectations, pointing to robust demandEvoke shares rise as much as 17% yet trade about 10% below the value of a recommended all-stock offer from Bally’s Intralot. Berenberg analysts expect the deal to get done on the current termsCMC Markets shares rise as much as 7.3%, extending strong gains since the online trading platform guided to a stronger-than-expected FY27 performance on Thursday, as Jefferies upgrades to buy from holdInfineon shares slide 5.7% after being downgraded by analysts at MP Capital Markets because the recent strength in the semiconductor stock leaves “limited upside” on the tableBodycote shares fall as much as 11%, most since March 2025, after Apollo Management Holdings said it does not intend to make a firm offer, ending discussions that began with a conditional proposal announced on May 22Wacker Chemie falls as much as 6%, the most since April 29, after Citi cut its recommendation to sell, saying momentum in upstream chemicals may be moderating, leading to a less compelling risk/reward for Wacker Chemie and ClariantAsian equities slid for a second day, dragged down by losses in technology hardware shares as enthusiasm for the artificial intelligence trade cools. The MSCI Asia Pacific Index fell as much as 2.3% before paring some of its declines. Heavyweight chipmakers Samsung and SK Hynix were the biggest drags. South Korea’s Kospi led losses around the region, tumbling over 5%. For the week, the regional measure was down about 1.3%. Stocks in Indonesia extended this week’s slump, heading for the lowest close since November 2020. Global tech stocks fell after a weaker-than-expected outlook from US chipmaker Broadcom, indicating investors are nervous about sustainability of the AI rally. Meanwhile a lack of progress in talks between the US and Iran threatened to keep oil prices elevated, raising inflation concerns.In FX, The Bloomberg Dollar Spot Index is down 0.2%, while the euro is holding its gain despite a downward revision to first-quarter GDP growth, entirely due to a contraction in Ireland. EUR/USD rose 0.2% to 1.1637. USD/JPY inched 0.1% lower to 159.86: Japan Finance Minister Satsuki Katayama reiterated that the government stands ready to respond appropriately to currency moves at any time. USD/CAD fell 0.2% to 1.3880:Friday’s data will include change in nonfarm payrolls, unemployment rate for the US and unemployment rate, net change in employment for Canada as wellIn rates, treasuries are mixed ahead of the May jobs report at 8:30am New York time, with oil prices little changed as traders await signs of progress in US-Iran peace talks.US yields remain within a basis point of Thursday’s closing levels with the 10-year near 4.47%. Gilts in the sector outperform slightly while bunds lag by around 1bp. US curve spreads are marginally steeper on the day. WTI crude oil futures down 0.2% underpin Treasuries, while Nasdaq 100 futures are off nearly 1% as tech stocks falter.Ahead of May jobs report, Fed-dated OIS contracts price in around 17bp of tightening by year-end and fully price in a 25bp hike by the March FOMC meeting. Into the data, Thursday’s activity in Treasury options was active and mixed in direction, while SOFR options flows largely consisted of position liquidation and adjustment, as traders looked reduce risk.In commodities, Brent edged lower to around $94.80 a barrel. Cryptocurrencies are under sustained selling pressure, heading for a sixth straight day of losses. Sentiment is hurt by Middle East tensions, expectations of higher U.S. rates, ETF outflows, and Strategy’s reported bitcoin sales for the first time since 2022. Bitcoin falls 2% to $62,292, Ether drops 5.8% to $1,669, and Solana declines 4.1% to $66.20, all near multi-month or multi-year lows.Today's US economic data calendar includes May jobs report (8:30am) and April consumer credit (3pm). Fed speaker slate empty for the session. External communications blackout commences Saturday ahead of the June 17 policy announcementMarket SnapshotTop Overnight NewsUS and Iran Show Little Progress in Talks After Week of Clashes: BBGIran has informed Pakistan of its acceptance of transferring part of its uranium to a third country that agrees to it. However, Al Arabiya followed up by stating that the US still refuses Iran's request to release its frozen funds.Senate passes $70 billion ICE funding; fails to ban Trump's 'anti-weaponization' fund: RTRSSenate blocks debate on FISA surveillance law days before program 'goes dark: RTRSAnthropic Calls for AI Pause Button to Let Humans Take Stock: BBGApple’s Plan for AI Dominance Rests on Fixing Its Much‑Maligned Chatbot: WSJPoint72 Weighs Paying Other Hedge Funds to See Their Trade Ideas: BBGMorgan Stanley Sees SpaceX’s Revenue Reaching $3.4 Trillion in 2040: WSJTrump's trade adviser Navarro said the Fed shouldn't raise rates into supply shock inflation.US officials held preliminary discussions with major AI companies about the potential for the government to acquire some shares in their firms, according to people familiar with the matter cited by NOTUS.Banks Curb China Trips, Delay Events After Cross-Border Scrutiny: BBGThe Anything-Goes Era in Private‑Credit Lending Is Coming to an End: WSJAmericans on GLP-1s Are Overwhelming Retailers With Their Nonstop Returns: WSJA weekly flow data shows USD 39bln into bonds (a record inflow), USD 122bln into cash, USD 23.1bln into stocks, USD 2bln out of crypto (biggest since November 2025), USD 3.1bln out of gold (biggest in 10 weeks).A more detailed look at global markets courtesy of NewsquawkAPAC stocks were mostly lower with the region subdued by recent tech-related pressure, and despite the predominantly positive handover from Wall St, where healthcare helped boost the Dow to a record high. ASX 200 declined as the losses in the mining, materials and resources sectors overshadowed the outperformance in health care. Nikkei 225 retreated amid tech selling but with the index off today's worst levels after bouncing off a floor beneath the 66,000 level, while data was mostly encouraging as Household Spending and Labour Cash Earnings topped forecasts, which effectively supports the argument for a BoJ rate hike this month. Hang Seng and Shanghai Comp were mixed with Hong Kong pressured after the recent efforts to tighten cross-border capital outflows, including banks suspending opening Hong Kong bank accounts for mainland clients that could be used for overseas investments, while the mainland is marginally positive after the PBoC resumed open market operations.Top Asian NewsJapanese PM Takaichi said there are pros and cons to a weak yen, while she added that investment strategy will help maintain trust in the yen and that her economic policy is aimed at boosting Japan's economic capability, not at FX manipulation.Japanese Finance Minister Katayama said the direction on sales tax cut hasn't been decided, adds government will not rely on debt to finance the food sales tax cut.European bourses (STOXX 600 +0.2) start the last trading session of the week mixed, with the breadth of performance narrow. Global tech continues to sell off, after Broadcom's AI chip revenue fell short of expectations, weighing on indices that are heavily weighted with tech names (AEX -0.1%, EuroStoxx 50 -0.1%). Sectors point to a neutral bias. Retail (+1.5%) and Media (+1.5%) outperform, while Technology (-1.6%) and Basic Resources (-1.8%) are the clear laggards.Top European NewsUK MP/PM candidate Burnham has spoken on options for increasing infrastructure spending without breaching the fiscal rules, FT reported citing sources.Andy Burnham says he would run in a Labour leadership contest and, if prime minister, urgently tackle social care, taxation and devolution while avoiding a snap election or immediate Brexit rerun, according to the Guardian.UK PM spokesperson said Starmer will not walk away from PM job, in response to Andy Burnham's bid for the leadership, while Burnham confirmed he'll stand to replace PM Starmer as Labour leader, as he stated that Wes Streeting seems to have launched a leadership contest, which he would seek to join.Norway's Stryke labour union said companies have agreed wage deal for oil workers and that they will not go and strike.FXG10s are all firmer against the Buck, where DXY -0.2% as it respects recent ranges into the US Jobs report. Franc leads, EUR +0.2% and GBP +0.2% also performing well.In a quiet morning session, the Buck has trundled lower from a 99.40 peak to a trough just above 99.20. Today sees the release of May US Jobs data, expected to tick lower to 85k from 115k in April. Recent labour market proxies align with expectations of a cooling in the labour market, as initial jobless claims rose to 225k from 212k, above the top end of the forecast range, while Challenger layoffs rose to 97.006k from 83.387k. Aside from macro data, focus remains on geopolitics, where headlines overnight suggested Washington demanded Tehran deliver its response before the end of the week or be hit with strikes. MUFG notes EUR/USD is vulnerable to a stronger employment print citing the OIS curve in Europe, which they believe is now well priced or even overpriced for what the ECB will deliver. Markets currently assign 14bps of tightening by year-end for the Fed.EUR performs well on the back of the weaker Buck. The likely catalysts today for the single currency will be the US Jobs report, which is expected to cool on a monthly basis. ING, which has an above consensus expectation (100k vs consensus 85k), contends the US print will support the Buck, and potentially enough to price a 25bp hike from the Fed by year-end, widening rate differentials. EUR/USD +0.2% firmed throughout the morning after rising from the 1.16 mark.CHF continues to mark gains against the Euro and Buck in wake of May inflation data. EUR/CHF U/C, USD/CHF -0.2%. Antipodeans firmer, but to a lesser extent than cyclicals as metals are lower across the board and amid the general equity risk tone.Central BanksRBI keeps Repurchase Rate unchanged at 5.25%, as expected, via unanimous decision, while policy stance kept at neutral. RBI Governor Malhotra said the central bank would take steps, if needed, to rein in speculative activity in the FX market.Fixed IncomeGlobal fixed benchmarks are slightly firmer this morning alongside some mild pressure in the energy complex. Markets remain on tenterhooks, awaiting the key NFP report and mixed geopolitical updates: 1) Trump said talks with Iran are going well, 2) reports suggest Washington has demanded Iran deliver a response before the end of the week, 3) Hezbollah rejected the US-backed ceasefire between Lebanon and Israel. (Please see the commodities section for details.)USTs (+9 ticks) are firmer and trade within a narrow 19-18 to 109-23 range. Tentative action as markets await the US NFP report later today; in brief, the US economy is expected to add 85k nonfarm payrolls in May, vs 115k added in April. The unemployment rate is seen unchanged at 4.3%. Traders will be watching closely for signs of labour market deterioration, given that FOMC officials view employment risks as tilted to the downside, though Fed officials are seemingly more concerned about the inflation side of its mandate, amid the labour market stability.US yields are lower across the curve, with some mild underperformance in the belly. The 10yr (4.46%) resides just shy of the key 4.50% mark; a dovish NFP report could see the yield test near-term support at 4.45%, and then a cluster of highs at around the 4.42%. Of course, a hawkish report would see a potential test of 4.50%, and a breach above that mark will bring in near-term highs at 4.53%.Bunds (U/C) and Gilts (+17 ticks) also trade incrementally firmer. There has been a lack of pertinent newsflow for either region; UK Halifax House Price Index showed that prices edged a little lower in May due to the Middle East war. Elsewhere, the BoE DMP report was released, which saw 1yr ahead inflation expectations rise, whilst the 3yr was left unchanged. Focus will shift to BoE speak via Dhingra and Bailey this afternoon. Bunds currently hold within a 125.54 to 125.69 range; Gilts hold within a 87.77 to 88.05 range.CommoditiesIn US-Iran news, the biggest setback this week regarding US and Iran talks (in spite of the flare-ups) came in Lebanon, where Hezbollah publicly rejected the latest US-backed Israel-Lebanon ceasefire framework, saying it required Hezbollah concessions without an Israeli withdrawal, and vowed to continue resistance while Israeli forces remain in Lebanese territory. An Israel-Hezbollah ceasefire remains a key Iranian demand for broader peace talks. Washington reportedly demanded Tehran respond by the end of the week and warned of either an agreement or military action. More recently, Al Hadath reported that Iran has informed Pakistan of its acceptance of transferring part of its uranium to a third country that agrees to it, which resulted in fleeting downside in energy benchmarks.Crude futures are off their worst levels with little in terms of notable geopolitical headlines this morning. Following Hezbollah’s rejection yesterday, Israeli army issued evacuation warnings for 9 villages in southern Lebanon. Note, this morning, there were reports of a marine drone exploding in Romania, although the Romanian defence ministry later clarified that this was a Romanian army drone. WTI Jul resides in a USD 91.50-USD 93.54/bbl range while Brent Aug sits in a USD 93.64-95.90/bbl range. Dutch TTF trades higher by around 1%, just north of the EUR 49/MWh level.Spot gold has rebounded after finding support at its 200 DMA for a second day in a row (200 DMA at USD 4428/oz today). The yellow metal still trades with modest intraday losses and within a USD 4429-4482/oz range, within yesterday’s 4424-4515/oz parameter. Traders look ahead to the US NFP later today for impetus (full preview available on Newsquawk).Base metals are lower across the board but to varying degrees after trickling lower in APAC alongside the mostly downbeat overnight risk sentiment. 3M LME copper resides in a USD 13,711.70-13,893.30/t range at the time of writing.Petroleum Development Oman said operations at the Mina Al Fahal port are proceeding normally after oil loadings were suspended following an explosion due to an alleged drone attack.Trade/TariffsUS President Trump said automakers sought no tariff changes in their meeting and that talks focused mostly on car repair.China International Trade Council says it opposes proposed US tariffs and criticised the plan for 12.5% tariffs on Chinese goods.Geopolitics: Middle EastIran has informed Pakistan of its acceptance of transferring part of its uranium to a third country that agrees to it, Al-Hadath reported. However, Al Arabiya followed up by stating that the US still refuses Iran's request to release its frozen funds.US President Trump said they do not need help from European countries regarding Hormuz and noted that Iran talks are going well, while he reiterated that almost all of Iran's leadership has been wiped out and that Iran has no navy or air force. Trump said if Iran killed US troops, it would restart the war quickly, and the Israel-Lebanon conflict is interconnected with Iran. Trump also stated he thinks progress has been made on Lebanon, and he would be honoured to meet Iran's Supreme Leader if a deal is made.Iranian Foreign Minister Araghchi said they have many documents and evidence that show Kuwaiti skies have been used regularly against Iran. Araghchi also commented that Iran and Oman will regulate the management of the Strait of Hormuz based on international law standards, while they will exchange views and ideas about the management of the Strait with the Persian Gulf countries, but ultimately the decision will be made between Iran and Oman.Iran's Supreme Leader advisor Rezaei said US President Trump wants to pressure Iran to accept his conditions and keep Iran in a vague state, while he added that the current draft has ambiguities that have to be clarified. Rezaei also said that Iran will stand firmly with Hezbollah in Lebanon and that Iran will have no hesitation in defending its interests and security.Pakistan's interior minister was reported to return to Tehran to push negotiations.Israeli army issued evacuation warnings for 9 villages in southern Lebanon, Sky News Arabia reported.Hezbollah claimed drone and missile attacks on Israeli bases, while it also stated that six Merkav tanks were destroyed in Lebanon, according to Fars.US House rejected a war powers resolution on Lebanon in a 92 vs 324 vote.Geopolitics: UkraineUS House voted 226 to 195 to approve the Ukraine aid package and Russia sanctions bill after more than a dozen GOP lawmakers voted against party lines.Geopolitics: OtherUS sanctioned Cuba's President Miguel Diaz-Canel, while President Trump said sanctions are not meant to accelerate a collapse, and stated they will handle Cuba after they take care of Iran.Marine drone explosion has been reported in Romanian Black Sea Port of Constanta-Digi 24. Romania’s Defence Ministry later said that the Romanian Army maritime drone found at Constanța civilian port self-detonated, causing no casualties, and was not linked to recent Black Sea exercises.US Event Calendar8:30 am: May Change in Nonfarm Payrolls, est. 88k, prior 115k8:30 am: May Change in Manufact. Payrolls, est. 2k, prior -2k8:30 am: May Unemployment Rate, est. 4.3%, prior 4.3%DB's Jim Reid concludes the overnight wrapAs we hit another payrolls Friday in the US, Asian markets are seeing some decent sized tech losses in what seems to be a hangover from Wednesday night's Broadcom results where forecasts weren't as elevated as some of the more optimistic predictions hoped. The KOSPI is down -5.02% with the Nikkei -1.27% lower. The latter is also influenced by the increasing view that the Bank of Japan will have to raise rates over the coming year. The meeting on the 16th of this month now sees a 96% probability of a hike according to futures. In our World Outlook our economist forecast a hike a quarter over the next year. This is more hawkish than the consensus.The Hang Seng (-0.84%) is also trading lower on tech losses with the ASX -0.63%. S&P 500 (-0.59%) and NASDAQ 100 (-1.07%) futures are also weak for this time of the day. Bucking the trend is the Shanghai Composite (+0.43%). European stock futures are only down just over a tenth of a percent given their low tech weighting. Early morning data revealed that Japan’s real wages rose by +1.9% in April (compared to +1.7% anticipated) y/y, contributing to a smaller-than-expected decline in household spending. Average nominal wages, or total cash earnings, increased by +3.5% year-on-year (against +3.1% expected). This figure represents the fastest wage growth since December 2024, following a revised increase of +3.1% in March. The April data marks the first instance in over 34 years where wage growth has surpassed 3% for three consecutive months. In a separate report, Japan’s household spending decreased by -0.5% year-on-year in April, a less severe decline than the expected drop of -1.5%, following a -2.9% decrease in the previous month. This decline has extended the trend of falling consumer spending to five consecutive months.Before these overnight moves, markets stabilised yesterday amidst growing hopes for some sort of US-Iran deal. So Brent crude oil prices (-2.84%) fell back to $95.03/bbl, reversing course after three consecutive gains, which in turn helped to ease fears about a stagflationary shock. As a result, markets followed the usual pattern of the last three months, where lower oil prices meant bond yields also fell back, with investors pricing in a more dovish path for central banks too. Meanwhile, equities recovered, including the S&P 500 (+0.41%), although it wasn’t all good news for risk assets yesterday, with Bitcoin (-2.06%) falling to its lowest level since early February, at $63,575. In terms of the latest from the Middle East, there wasn’t much in the way of fresh news. However, oil prices saw a clear move lower after Trump issued a post criticising the vote in the House of Representatives against the Iran conflict. That was because Trump’s post said the vote was “right in the middle of my final negotiations to end the War”. So that suggested talks were still happening and a deal might be near. Oil prices did rebound a bit during the US session as Lebanon’s Hezbollah militia rejected the US-brokered ceasefire, but overall this didn’t derail the more optimistic mood following the ceasefire announcement by Israel and the Lebanese government the previous evening.And investors also priced out the chance of a longer conflict, with the 6-month Brent future (-2.15%) also falling to $85.04/bbl. So that helped to ease concerns about inflation, with the 1yr US inflation swap (-9.2bps) falling to 3.09%, whilst the 1yr Euro inflation swap (-5.5bps) fell to 2.99%.With easing fears around inflation, markets dialled back the chance of a rate hike from the Federal Reserve this year. Indeed, the probability of a hike by December was down to 68% by the close, having been at 81% the previous day. Moreover, those dovish expectations got further support from some weaker US data, with the weekly initial jobless claims rising to their highest since early February. They hit 225k in the week ending May 30 (vs. 215k expected), and even though the Memorial Day holiday could have created volatility, the 4-week moving average also reached a 3-month high of 214.75k. So the release leant against the more positive US data in recent days, and it helped Treasury yields to decline across the curve. For instance, the 2yr yield (-3.8bps) fell back to 4.04%, whilst the 10yr yield (-2.1bps) fell back to 4.47%, roughly where we are this morning as I type. Looking forward, US data will stay in the spotlight today, as we’ll get the May jobs report at 13:30 London time. This will be an important one for the Fed, as the strong labour market data of recent weeks has fuelled the speculation about a potential rate hike. Indeed, we’ve just had back-to-back payrolls above +100k in March and April, which is the first time that’s happened since 2024. And so long as the labour market stays in decent shape, that will keep the focus on the inflation side of the Fed’s mandate, which has moved increasingly above target given the energy shock. In terms of today’s report, our US economists expect payrolls to come in at +50k (consensus +88k), with the unemployment rate remaining at 4.3%. So if realised, that would be a slowdown from the last couple of months, but would still mark 3 consecutive positive readings for the first time in a year. Our economists' lower than consensus forecast is not necessarily a structural story, more a slowdown in some sectors that have recently seen outsized gains. Our economists have been more optimistic on the labour market than their peers in recent months.Ahead of that, US equities also regained momentum before this morning's futures sell-off, with the S&P 500 (+0.41%) paring back the previous day’s losses and still looking to post a 10th consecutive weekly increase for the first time since 1985. We are at +0.06% so far this week but futures are lower so we'll see what happens. Most constituents in the index put in a solid performance yesterday, with 363 advancers – the most since April – and with the equal-weighted S&P 500 (+0.79%) rising to an all-time high. Chipmakers were the major exception to that, and Broadcom (-12.59%) was the second-biggest decliner in the index after their earnings the previous day. That included a forecast for AI chip revenue that was beneath expectations, which led to broader concerns around the sector. The Philly semiconductor index fell by -2.15% but it did recover from as much as -6.29% down early in the session. And the broader tech mood wasn’t as negative, with six of the Mag-7 (+1.06%) moving higher. Earlier in Europe, markets had put in a positive session across bonds and equities, benefiting from the fall in oil prices and being less exposed to semiconductor stocks. So the STOXX 600 (+0.52%) put in a decent performance, alongside gains for the DAX (+0.60%), the CAC 40 (+1.15%) and the FTSE MIB (+0.27%). Moreover, European rates rallied too, with yields on 10yr bunds (-1.0bps), OATs (-1.5bps) and BTPs (-1.8bps) all falling.Looking at the day ahead, data releases include the US jobs report for May, French industrial production for April, and the third release of Q1 GDP for the Euro Area. Central bank speakers include BoE Governor Bailey and the BoE’s Dhingra.

Futures Drop On Souring Chipmaker Sentiment, Kospi Plunge

“Following a period of upward revisions to earnings expectations across the sector, investors are taking a more selective approach to new information and guidance updates,”

4,824 words~22 min read